According to Lodging Econometrics’ (LE’s) Construction Pipeline Trend Report for the United States, the total U.S. construction pipeline stands at 5,216 projects/650,222 rooms. These are year-end 2020 results, and are down only incrementally, as the United States grappled with the ongoing coronavirus pandemic, an election, civil unrest, and the large and rapid partisan shift taking place. However, the announcement of various vaccine developments and distribution was undeniably good news for the general public, businesses, hotel development and the lodging industry as a whole, especially going forward. The industry has found optimism in the fact that as the vaccine rolls out travel demand will increase rather quickly, resulting in increased confidence in hotel development activity.

At the end of Q4 ‘20, projects currently under construction stand at 1,487 projects/199,700 rooms. Of the 1,487 projects under construction, 24% of these projects in the pipeline belong to extended-stay brands, a segment of the industry that developers have become increasingly interested in over the last few years. Projects under construction continue to move towards opening. Through year-end 2020, the U.S. opened 833 projects accounting for 97,203 rooms, bringing the U.S. supply of open & operating hotels to 58,569 hotels/5,557,119 rooms. Additionally, of the 833 projects opened in 2020, an impressive 29% of those projects belong to extended-stay brands.

LE is forecasting another 929 projects/107,407 rooms to open by the end of 2021. If all of these projects come to fruition it will represent a 1.9% increase in new hotel supply. For 2022, LE is forecasting 1,031 projects/116,749 rooms to open.

Projects scheduled to start construction in the next 12 months total 2,015 projects/234,703 rooms, down 12% by projects and 11% by rooms YOY. Projects in the early planning stage stand at 1,714 projects/215,819 rooms, a cyclical high in the number of rooms, and up slightly YOY.

It is also worth noting that renovations and brand conversions are becoming more prevalent. At the end of Q4 ‘20, there were a total 1,308 projects/210,124 rooms under renovation or conversion in the U.S. The number of projects and rooms has grown consistently over the last three quarters of 2020.

Related Stories

Industry Research | Aug 29, 2019

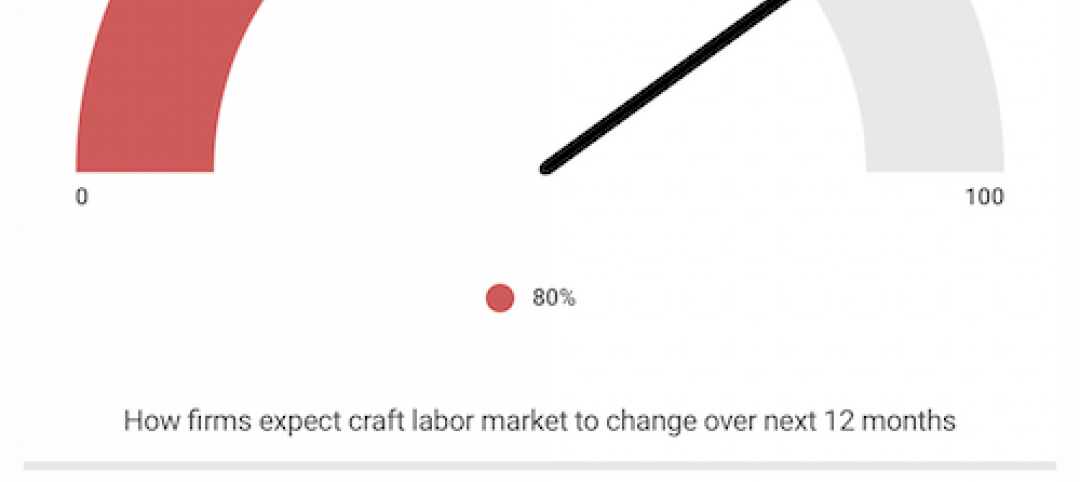

Construction firms expect labor shortages to worsen over the next year

A new AGC-Autodesk survey finds more companies turning to technology to support their jobsites.

Market Data | Aug 21, 2019

Architecture Billings Index continues its streak of soft readings

Decline in new design contracts suggests volatility in design activity to persist.

Market Data | Aug 19, 2019

Multifamily market sustains positive cycle

Year-over-year growth tops 3% for 13th month. Will the economy stifle momentum?

Market Data | Aug 16, 2019

Students say unclean restrooms impact their perception of the school

The findings are part of Bradley Corporation’s Healthy Hand Washing Survey.

Market Data | Aug 12, 2019

Mid-year economic outlook for nonresidential construction: Expansion continues, but vulnerabilities pile up

Emerging weakness in business investment has been hinting at softening outlays.

Market Data | Aug 7, 2019

National office vacancy holds steady at 9.7% in slowing but disciplined market

Average asking rental rate posts 4.2% annual growth.

Market Data | Aug 1, 2019

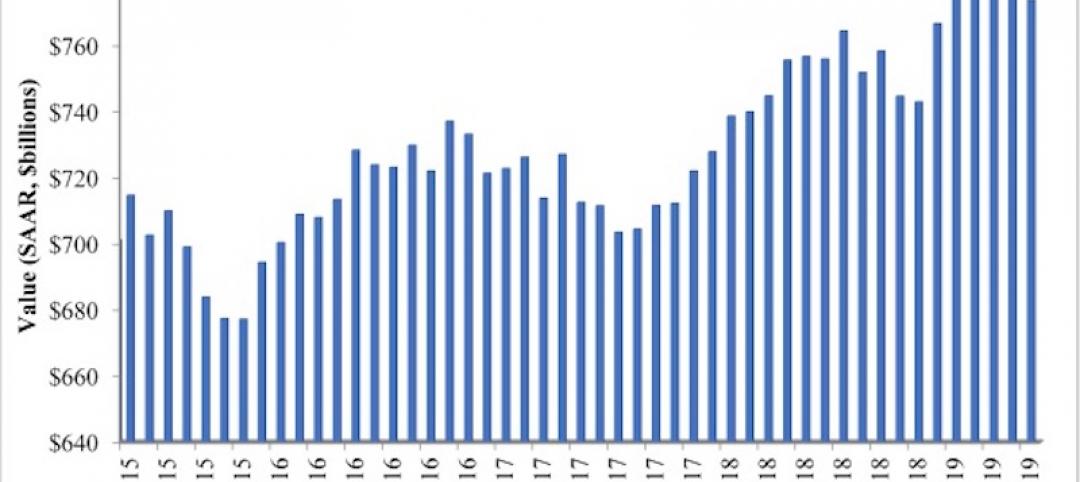

Nonresidential construction spending slows in June, remains elevated

Among the 16 nonresidential construction spending categories tracked by the Census Bureau, seven experienced increases in monthly spending.

Market Data | Jul 31, 2019

For the second quarter of 2019, the U.S. hotel construction pipeline continued its year-over-year growth spurt

The growth spurt continued even as business investment declined for the first time since 2016.

Market Data | Jul 23, 2019

Despite signals of impending declines, continued growth in nonresidential construction is expected through 2020

AIA’s latest Consensus Construction Forecast predicts growth.

Market Data | Jul 20, 2019

Construction costs continued to rise in second quarter

Labor availability is a big factor in that inflation, according to Rider Levett Bucknall report.