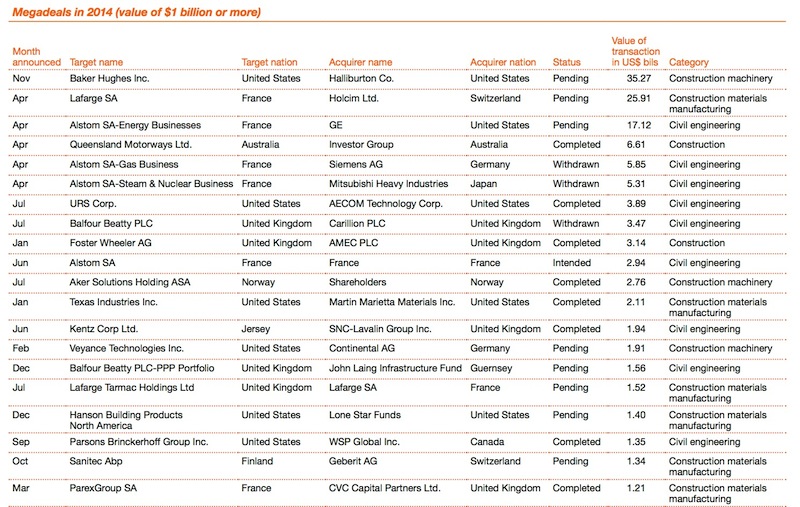

PwC's latest quarterly analysis reported that the worldwide engineering and construction industries closed 218 merger and acquisition deals in 2014 worth more than $172 billion. The numbers are more than three times greater than 2013's total of $55 billion. Last year was the busiest year for M&A activity since 2007.

There were four mega deals in the fourth quarter of 2014, including one valued at $35 billion. Overall, there were 21 mega deals last year, totaling $127 billion. The greatest number of deals took place in Asia and Oceania.

“Some of the significant year-over-year growth in M&A activity can be attributed to companies seeking to better position themselves for mega projects that not only require a longer commitment of time and capital, but also deeper pools of highly skilled talent,” said H. Kent Goetjen, U.S. engineering and construction leader at PwC. “The lack of available talent, which is being fueled in the U.S. by the retirement of the baby boomer generation, is driving up the price of acquisitions and will continue to do so for the foreseeable future.”

PwC analysts are monitoring several other trends that are expected to affect the values and locations of deals in the engineering and construction sector, including:

• The integration of design and consultancy firms with construction companies is well under way as the E&C industry continues to move toward full service integration. Firms are generally looking to leverage higher-value added services, such as design, while balancing out their regional exposure.

• A major driver of consolidation is talent needs, as companies compete for specialized technical expertise in high-demand segments. As an alternative to acquiring expertise, some companies are embarking upon joint ventures, but these are complicated and add significant operational risk to any project. Companies are positioning themselves to bid on larger, increasingly complex projects with new partners and non-traditional sources of funding.

• A flurry of smaller, local deals took place, particularly within Asia. Cross-border activity dropped to 22% of the total in the quarter, with most local activity occurring in Asia.

• Cement oversupply and tepid demand continue to plague the industry. Top players, in an attempt to maintain their market share and margin, continue to acquire smaller companies post-merger announcement of Holcim and Lafarge.

• The consolidation in Asia was not limited to the construction materials segment, and not all driven by overcapacity, as all segments of E&C experienced a pick-up in local consolidation. The uncertain economic outlook in China raises many concerns for inbound activity in Asia but does not seem to be hindering deal activity in the region.

Related Stories

Engineers | Oct 17, 2016

Confidence in construction markets is high among U.S. engineering leaders: ACEC survey

The American Council of Engineering Companies’ third quarter Engineering Business Index rose 6.2 points to 63.3—the largest quarter-to-quarter increase since the EBI’s inception.

| Sep 26, 2016

RELIGIOUS FACILITY GIANTS: A ranking of the nation’s top religious sector design and construction firms

Gensler, Leo A Daly, Brasfield & Gorrie, Layton Construction, and AECOM top Building Design+Construction’s annual ranking of the nation’s largest religious facility AEC firms, as reported in the 2016 Giants 300 Report.

Architects | Sep 21, 2016

DLR Group broadens its practice range and market penetration with addition of Westlake Reed Leskosky

The merger, say company officials, creates “a global design leader” in a consolidating industry.

Architects | Sep 15, 2016

Implicit bias: How the unconscious mind drives business decisions

Companies are tapping into the latest research in psychology and sociology to advance their diversity and inclusion efforts when it comes to hiring, promoting, compensation, and high-performance teaming, writes BD+C's David Barista.

AEC Tech | Sep 6, 2016

Innovation intervention: How AEC firms are driving growth through R&D programs

AEC firms are taking a page from the tech industry, by infusing a deep commitment to innovation and disruption into their cultural DNA.

Office Buildings | Sep 2, 2016

Eight-story digital installation added as part of ESI Design’s renovation of Denver’s Wells Fargo Center

The crown jewel of a three-year makeover project, the LED columns bring the building’s lobby to life.

| Sep 1, 2016

TRANSIT GIANTS: A ranking of the nation's top transit sector design and construction firms

Skidmore, Owings & Merrill, Perkins+Will, Skanska USA, Webcor Builders, Jacobs, and STV top Building Design+Construction’s annual ranking of the nation’s largest transit sector AEC firms, as reported in the 2016 Giants 300 Report.

| Sep 1, 2016

INDUSTRIAL GIANTS: A ranking of the nation's top industrial design and construction firms

Stantec, BRPH, Fluor Corp., Walbridge, Jacobs, and AECOM top Building Design+Construction’s annual ranking of the nation’s largest industrial sector AEC firms, as reported in the 2016 Giants 300 Report.

| Sep 1, 2016

HOTEL SECTOR GIANTS: A ranking of the nation's top hotel sector design and construction firms

Gensler, HKS, Turner Construction Co., The Whiting-Turner Contracting Co., Jacobs, and JBA Consulting Engineers top Building Design+Construction’s annual ranking of the nation’s largest hotel sector AEC firms, as reported in the 2016 Giants 300 Report.

| Sep 1, 2016

CULTURAL SECTOR GIANTS: A ranking of the nation's top cultural sector design and construction firms

Gensler, Perkins+Will, PCL Construction Enterprises, Turner Construction Co., AECOM, and WSP | Parsons Brinckerhoff top Building Design+Construction’s annual ranking of the nation’s largest cultural sector AEC firms, as reported in the 2016 Giants 300 Report.