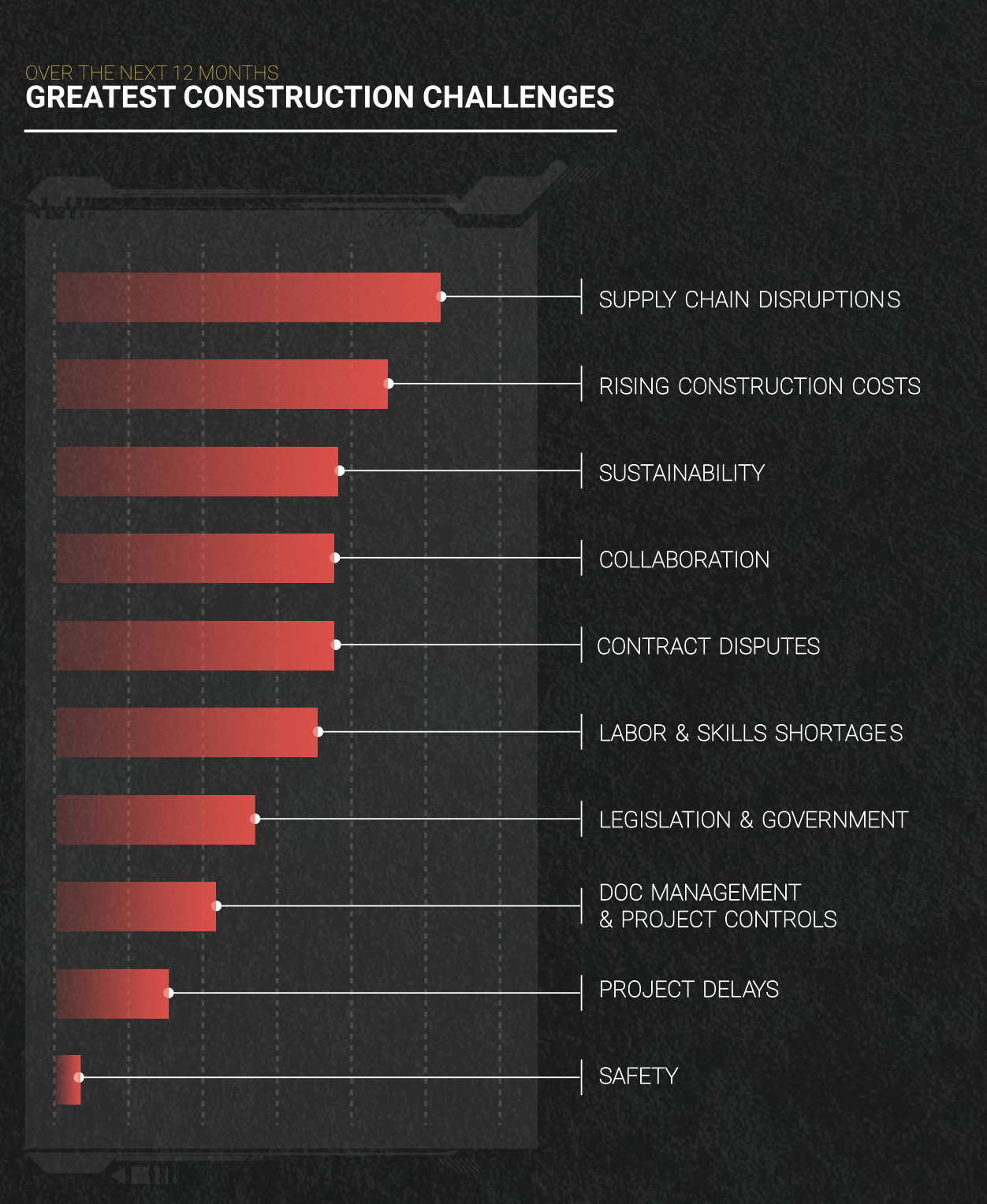

A recent survey of 514 project, site, and construction managers in the U.S. and the United Kingdom, conducted by OnePoll for XYZ Reality, a leading provider of augmented reality applications, found that 94 percent had project backlogs and 63 percent admitted to delivering projects off schedule either “somewhat” to “very frequently.”

“Poor project performance, low productivity, and costly major project failures—and high-profile industry bankruptcies—continue to dog the sector,” wrote KPMG International in its recently released 2023 Global Construction Survey, based on responses from 257 engineering and construction firms and project owners around the world (29 percent of which were based in North America).

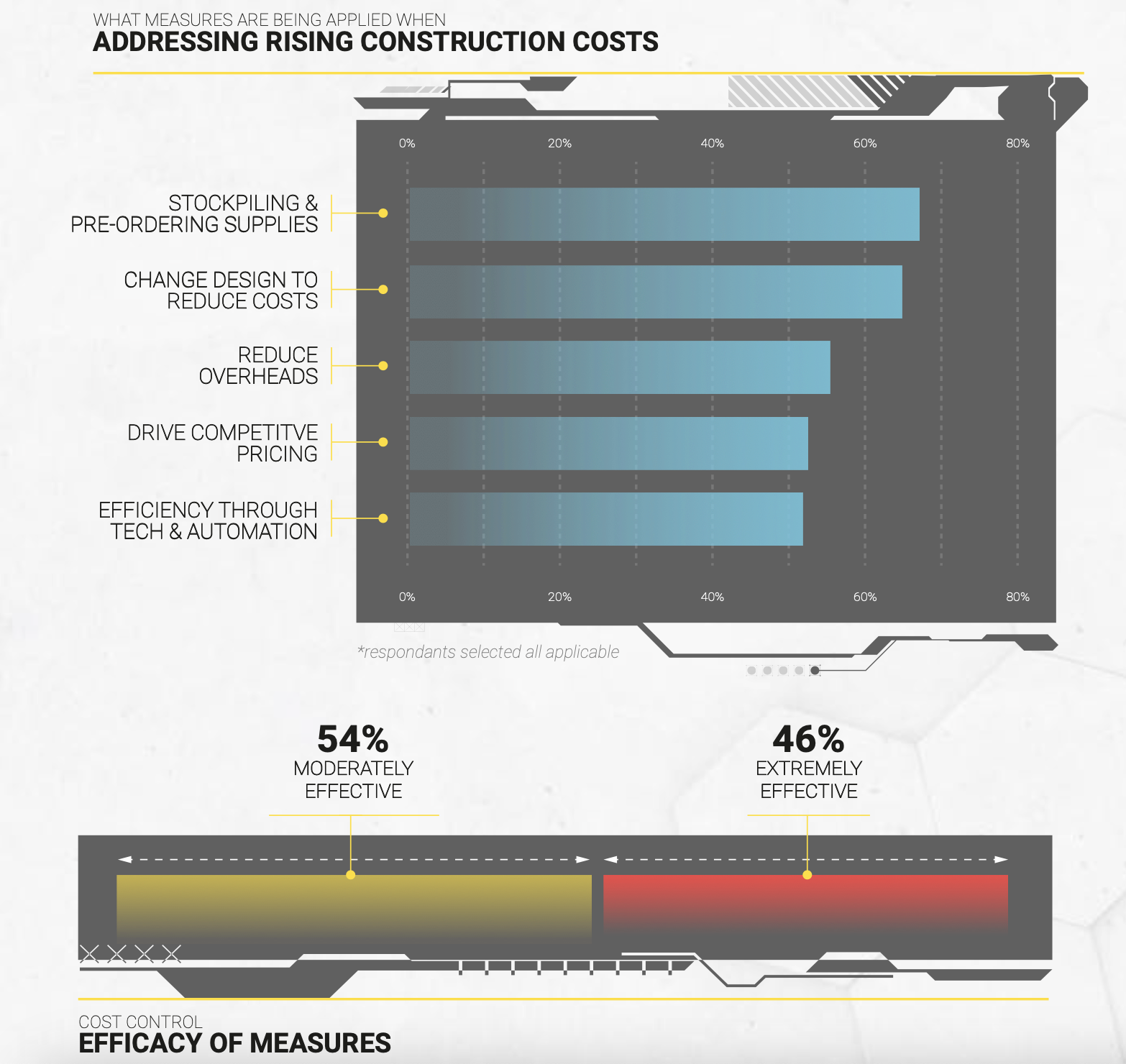

Respondents to KPMG’s survey, while mostly “cautiously optimistic” about their industry’s future, still lamented that less than half of their projects are being completed on time. Both surveys cite similar reasons why projects stall, starting with nagging supply-chain delays, labor shortages, and rising construction costs. KPMG is also seeing a “dramatic shift” by contractors away from fixed-price and guaranteed maximum-price contractors for major projects. Colin Cagney, the firm’s director of infrastructure, capital projects, and climate advisory in the U.S., surmises that contractors are attempting to mitigate their primary responsibility for performance risk.

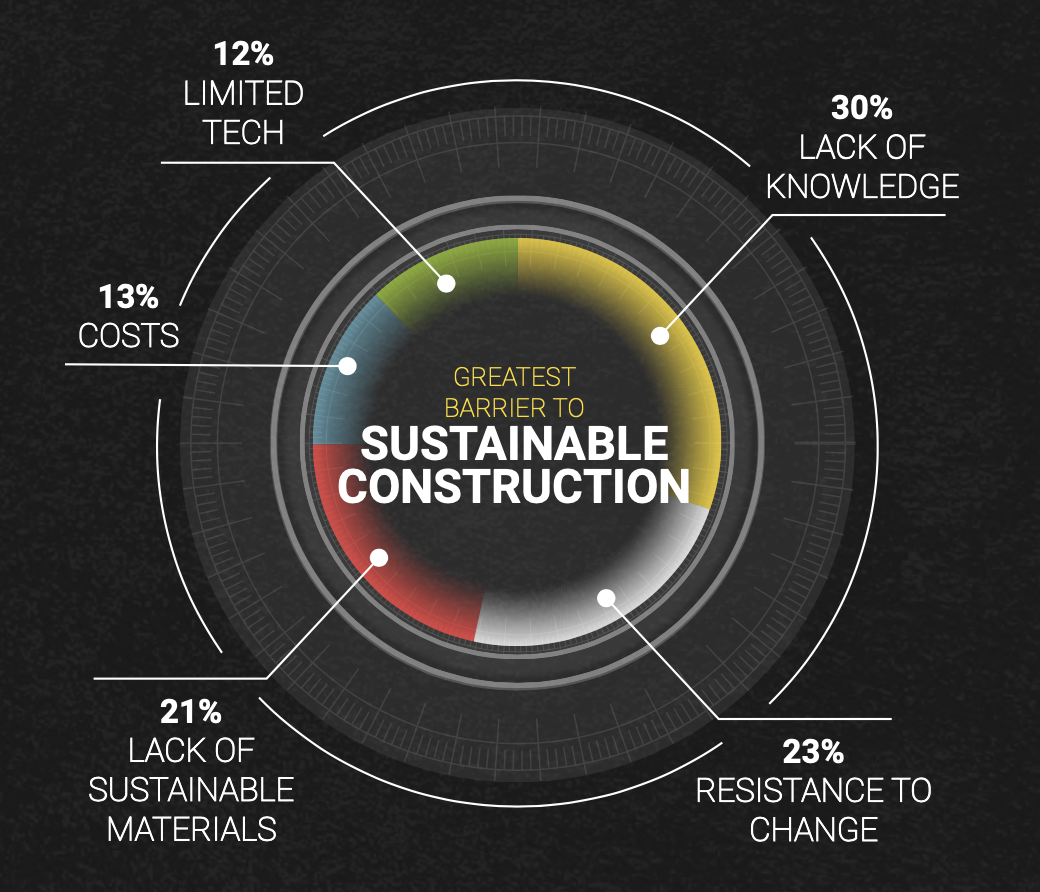

XYZ Reality’s survey notes, too, that construction firms struggle for a variety of reasons to meet their clients’ sustainability goals, and their projects get delayed as well by unexpected design changes, labor shortages, and poor jobsite communication.

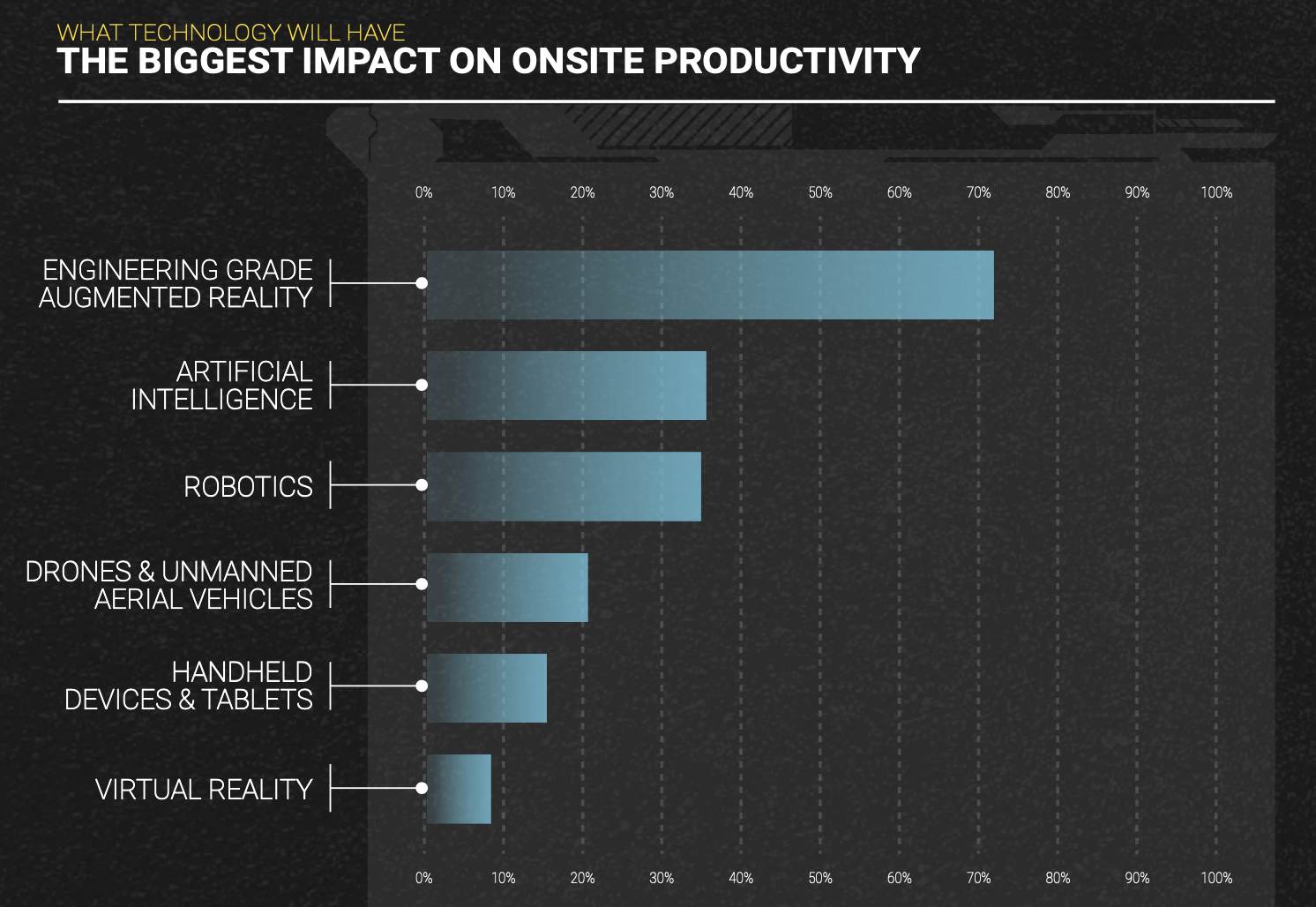

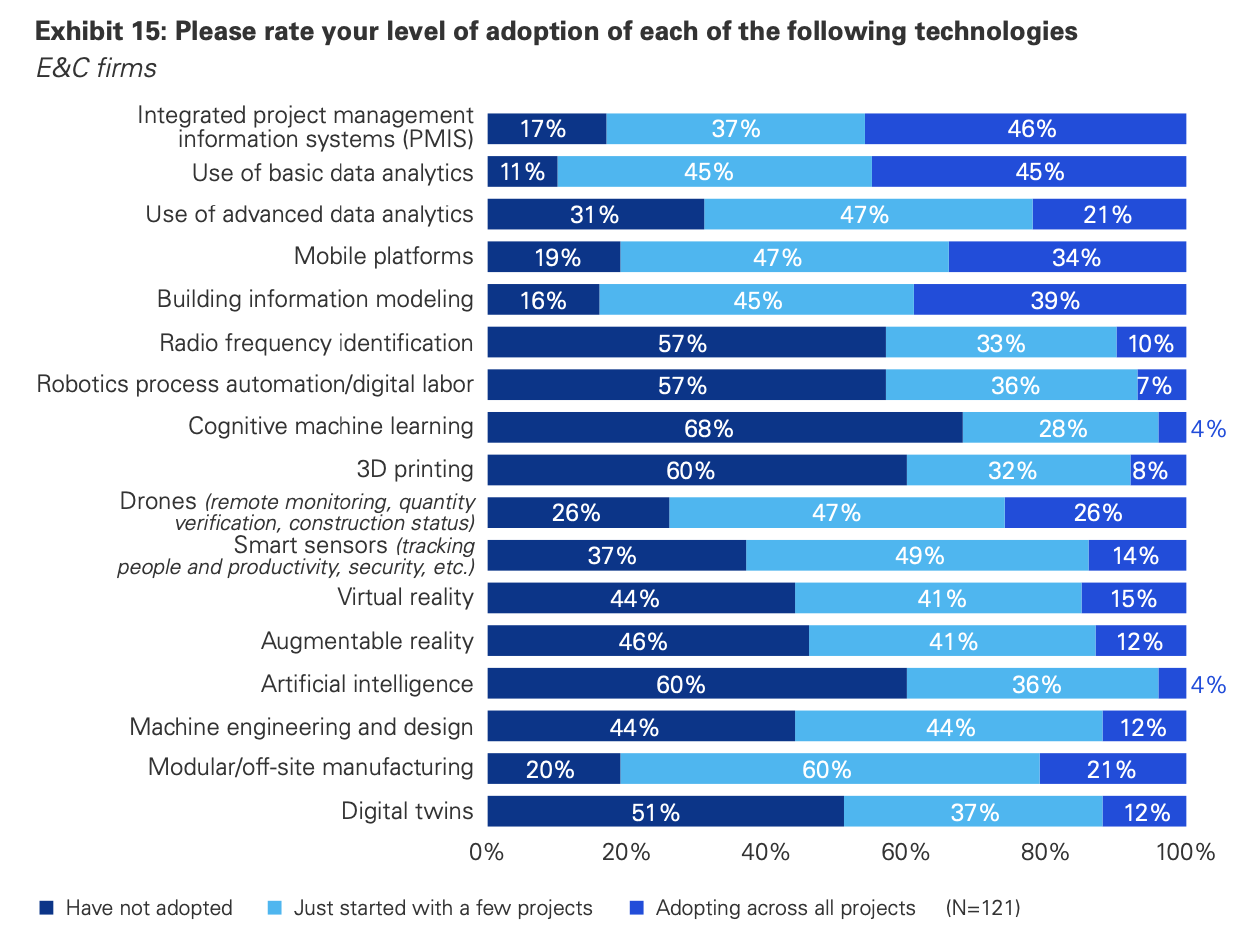

The biggest priority for respondents to KPMG’s survey is improving estimating accuracy, transferring risk, and increasing innovation. Both surveys depict an industry turning more toward technology for answers. Engineering-grade AR, AI, robotics, and drones are among the technological solutions preferred by respondents to XYZ Reality’s survey. More than eight in 10 respondents to KPMG’s survey have adopted mobile platforms, 43 percent are using robotics, and 40 percent are in early stages of using artificial intelligence. KPMG’s respondents also believe emerging technologies that include 3D printing have greater potential for delivering better returns on investment.

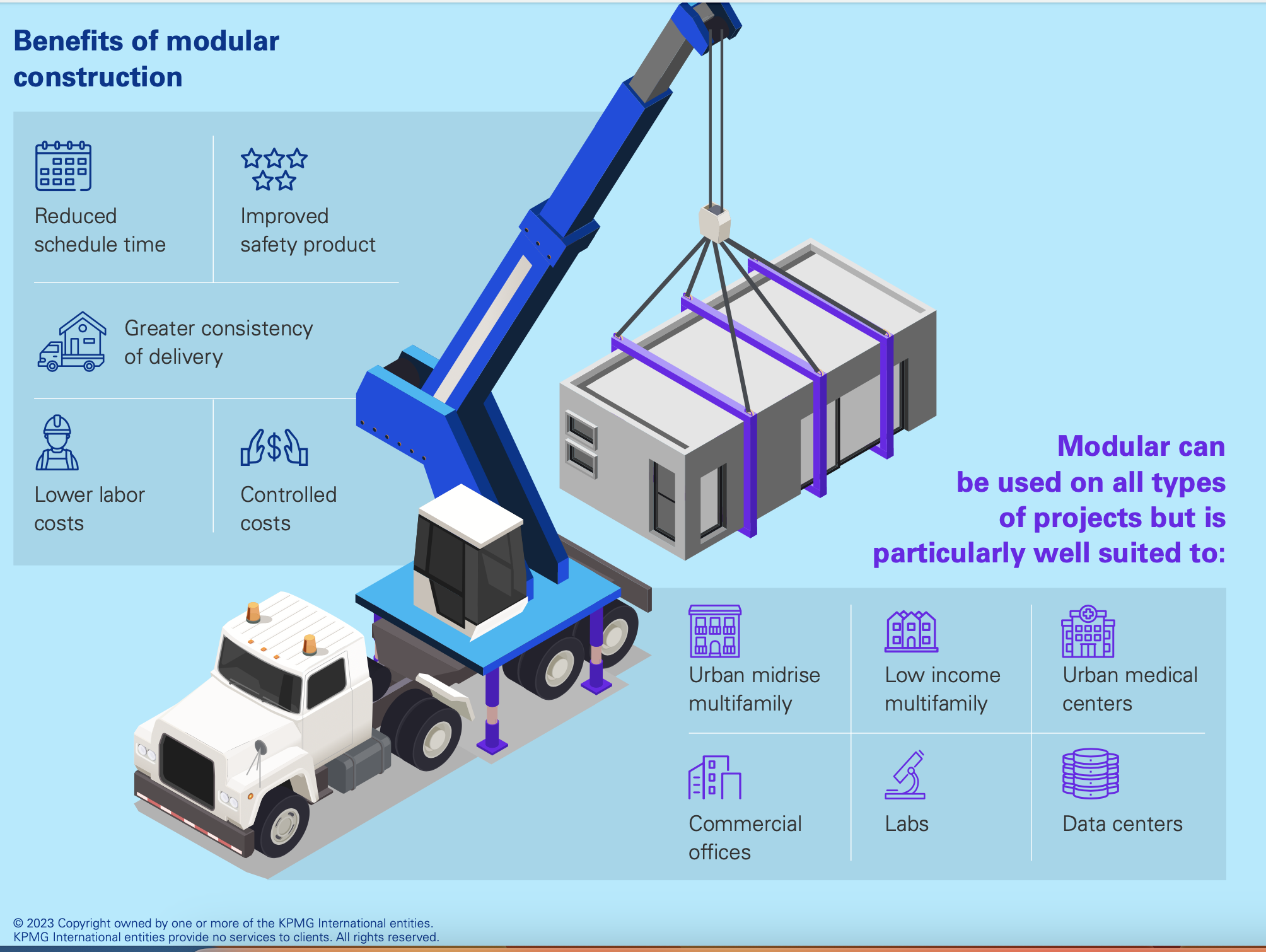

More than one-fifth of KPMG respondents have adopted modular and offsite manufacturing on all projects, and 60 percent on at least some projects.

“As our business grows, we want to be evolutionary rather than revolutionary,” stated John Murphy, CEO of J. Murphy & Sons Ltd., a London-based infrastructure construction firm, whose comments were among several respondents quoted in KPMG’s report. “We are continuously investing to keep up with the pace of technological change—constantly progressing.”

ESG and DEI are now priorities

This is KPMG’s 14th Global Construction Survey, which allows the firm the benefit of hindsight. One of the trends it has tracked is a stronger commitment among E+C firms to incorporate Environmental, Social, and Governance (ESG) precepts into their project practices. Nearly 54 percent of respondent firms “fully envision” the benefits of ESG and are aggressively pursuing maturity and improvement by embedding ESG into capital projects. (Admittedly, some of these pursuits are being mandated by stricter legislation.)

Firuzan Speroni, KPMG’s U.S. director of infrastructure, capital projects, and climate advisory, sees “a huge opportunity” for E+C firms and owners to commit to decarbonization of their buildings by measuring potential embodied carbon and choosing building materials with help to reduce it.

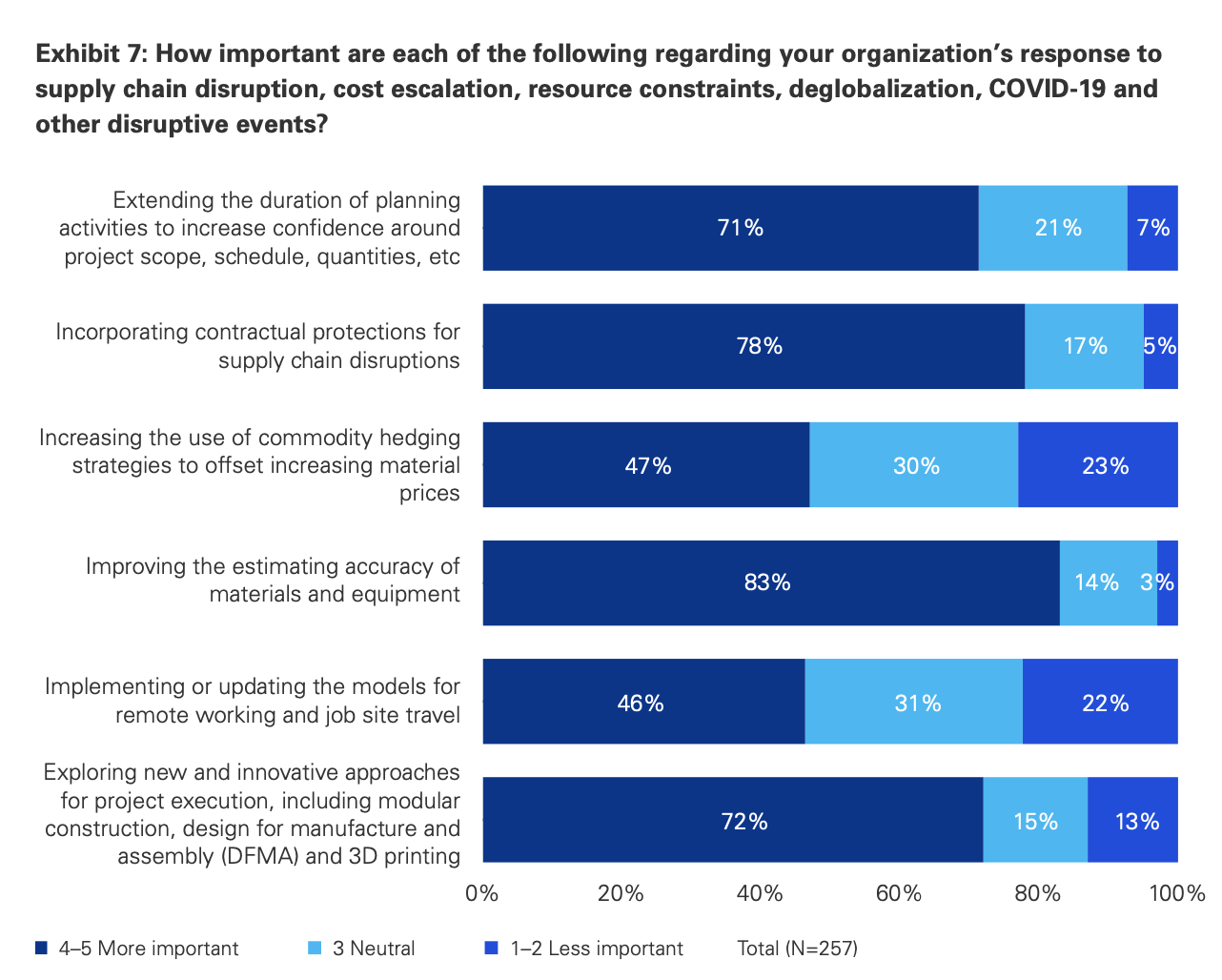

Respondents to the 2023 global survey ranked Diversity, Equity, and Inclusion as the third-most-important factor determining their success. Half of those respondents cited the importance of diversified workplace demographics to help address disruption. And 46 percent agreed that updating models for remote working and jobsite travel can contribute to construction projects’ resilience. However, the survey also found that the industry needs to do a better job of attracting and retaining talent. (For example, owners were only “relatively” concerned about reducing greenhouse gas emissions from their projects.)

Finding answers in tech

Both surveys highlight the centrality of innovation to the success of projects and businesses. For example, in 2017 E+C firms were only starting to deploy project management information systems, sensors, drones, or other robotics. This year’s survey, on the other hand, found that 81 percent of respondents from E+C firms say their organizations have adopted, or are starting to adopt, mobile platforms. The use of virtual reality tool has almost doubled (to 56 percent of respondents from 28 percent in 2017). Nearly half of E+C firms responding to the survey have adopted digital twin on at least some of their projects.

“The successful adopters are championing innovation from the very top, and investing in educating their teams,” observed Suneal Vora, a Partner in Business Consulting-Capital Projects and Industry 4.0 for KPMG in India. E+C firms must advocate for innovation, though, as owners seem somewhat less willing to adopt new technologies for their projects.

Keep up with a changing landscape

In summary, the key takeaways from the KPMG Global Construction Survey are:

•Address productivity as a matter of urgency, by taking an outside-in approach

•Master enterprise risk management, and have the confidence to resist a race to the bottom in choosing and financing projects

•Truly embed ESG as a component of a company’s sustainability profile and access to capital and talent

•Become data masters, which can help make jobsites safer and attract a new breed of digital worker.

Related Stories

Market Data | Aug 29, 2017

Hidden opportunities emerge from construction industry challenges

JLL’s latest construction report shows stability ahead with tech and innovation leading the way.

Architects | Aug 21, 2017

AIA: Architectural salaries exceed gains in the broader economy

AIA’s latest compensation report finds average compensation for staff positions up 2.8% from early 2015.

Market Data | Aug 17, 2017

Marcum Commercial Construction Index reports second quarter spending increase in commercial and office construction

Spending in all 12 of the remaining nonresidential construction subsectors retreated on both an annualized and monthly basis.

Industry Research | Aug 11, 2017

NCARB releases latest data on architectural education, licensure, and diversity

On average, becoming an architect takes 12.5 years—from the time a student enrolls in school to the moment they receive a license.

Market Data | Aug 4, 2017

U.S. grand total construction starts growth projection revised slightly downward

ConstructConnect’s quarterly report shows courthouses and sports stadiums to end 2017 with a flourish.

Market Data | Aug 2, 2017

Nonresidential Construction Spending falls in June, driven by public sector

June’s weak construction spending report can be largely attributed to the public sector.

Market Data | Jul 31, 2017

U.S. economic growth accelerates in second quarter; Nonresidential fixed investment maintains momentum

Nonresidential fixed investment, a category of GDP embodying nonresidential construction activity, expanded at a 5.2% seasonally adjusted annual rate.

Multifamily Housing | Jul 27, 2017

Game rooms and game simulators popular amenities in multifamily developments

The number of developments providing space for physical therapy was somewhat surprising, according to a new survey.

Architects | Jul 25, 2017

AIA 2030 Commitment expands beyond 400 architecture firms

The 2016 Progress Report is now available.

Market Data | Jul 25, 2017

Moderating economic growth triggers construction forecast downgrade for 2017 and 2018

Prospects for the construction industry have weakened with developments over the first half of the year.