Enabling talent, managing cost, and expanding influence are the three primary mandates that corporate real estate (CRE) executives are grappling with in their companies.

In its inaugural Americas Occupier Survey 2015/16, the CBRE Institute polled 229 executives about their strategies priorities, and practices. Forty-five percent of those respondents are in the Banking and Finance or in Tech and Telecom industries.

The majority (56%) of CRE executives say they are evaluated on the value and satisfaction they create among internal stakeholders. Throughout the survey, executives noted that their roles require them to address shortages in skilled labor, escalating costs, and economic uncertainties. Not surprisingly, uncertainties for execs in the Banking and Finance sectors revolve around tighter regulations.

CRE execs are dealing with a workforce that is more culturally, generationally, and ethnically diverse than ever. That workforce “strives to connect, integrate, and find community among peers in a world that is increasingly online” the report’s authors observe. Indeed, the highest portion of the survey’s respondents, 44%, says that connectivity to partners and supports is the most important factor to their labor forces, followed by flexible working hours, flexible space, and amenities.

Fifty-seven percent of respondents say their workplace strategies are driven by employee attraction and retention. And employers of choice are delivering the ideal work experience by linking their corporate real estate missions with human resources and information technology. Such “hyper-customized” environments emphasize brand, functionality, freedom of work style and community connectivity.

But CRE executives also insist that their strategic goals are thwarted when they don’t have support from their companies’ corporate suite. Productive and flexible workspaces and greater capital expenditure for real estate investment also rank high among the factors that give CRE execs the wherewithal to accomplish their objectives.

And when it comes to data, the majority of executives say they need information that enables data visualization and decision support. “Our research indicates that an optimal approach to CRE decisions will involve selective and discriminating use of analytics, paired with the irreplaceable role of a leader’s intuition and experience,” the report says.

CRE executives often manage their firms’ portfolio costs. A remarkable 85% of those polled said their companies had used space restructuring as a lever to reduce costs in the previous 12 months. But the pendulum is swinging away from smaller workstations and lower rents to smarter workplaces and agile leasing structures The survey finds that 31% of respondents’ companies are currently using shared office facilities, and another 15% say they are considering the merits of sharing space.

An emerging co-worker model “offers environments that inspire new levels of energy and connectivity that eluded earlier incarnations of the shared workplace model.”

Lease negotiation seems preferable to relocation as a cost-saving measure. For one out of every two companies, “talent determines the market; cost pinpoints the location,” the report says. However, expansion still dictates some moving decisions, as two out of five executives polled say accessing new markets and customers drive their companies’ relocation strategies.

AEC firms, take note: building and floorplan design is a leading decision driver when real estate executives are selecting a building to move into, even more important that real estate costs, lease options, or the quality of the location’s infrastructure or amenities.

Other findings of note from the survey include:

- 70% of CRE execs say their companies use external partnerships to deliver at least one function, like project or facilities management.

- Three quarters of CRE executives say their companies operate centrally.

- Half of the companies polled—which are all based in the Americas—favor India and Southeast Asia as expansion destinations.

Related Stories

Market Data | Nov 2, 2016

Nonresidential construction spending down in September, but August data upwardly revised

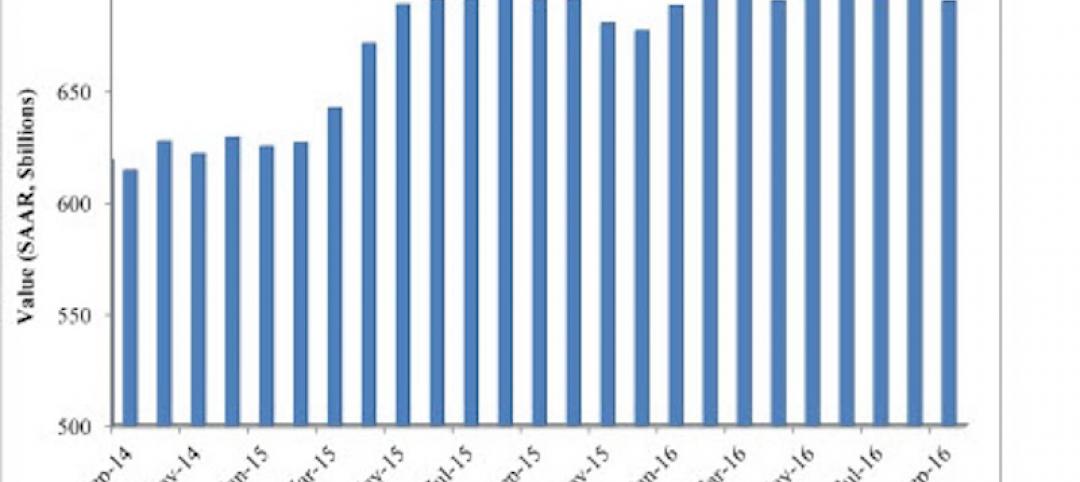

The government revised the August nonresidential construction spending estimate from $686.6 billion to $696.6 billion.

Market Data | Oct 31, 2016

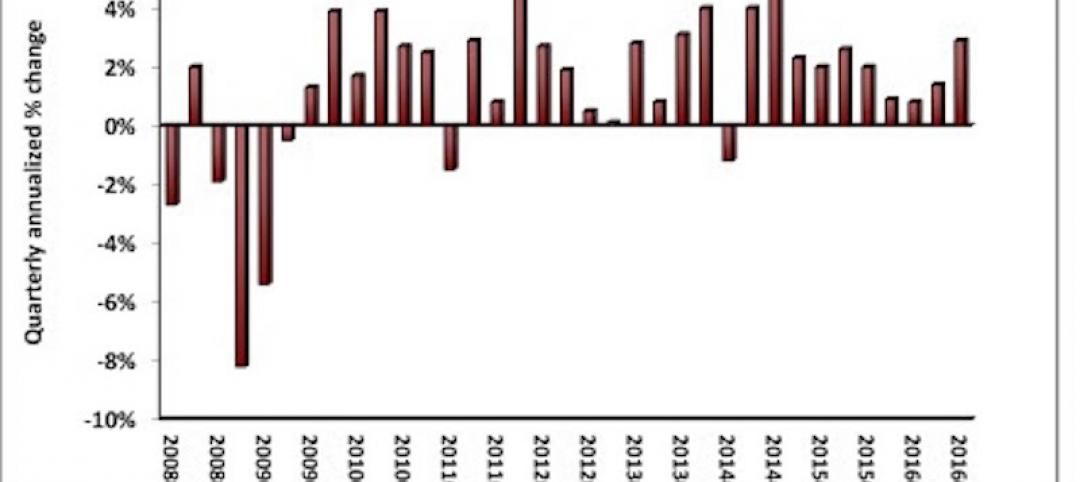

Nonresidential fixed investment expands again during solid third quarter

The acceleration in real GDP growth was driven by a combination of factors, including an upturn in exports, a smaller decrease in state and local government spending and an upturn in federal government spending, says ABC Chief Economist Anirban Basu.

Market Data | Oct 28, 2016

U.S. construction solid and stable in Q3 of 2016; Presidential election seen as influence on industry for 2017

Rider Levett Bucknall’s Third Quarter 2016 USA Construction Cost Report puts the complete spectrum of construction sectors and markets in perspective as it assesses the current state of the industry.

Industry Research | Oct 25, 2016

New HOK/CoreNet Global report explores impact of coworking on corporate real rstate

“Although coworking space makes up less than one percent of the world’s office space, it represents an important workforce trend and highlights the strong desire of today’s employees to have workplace choices, community and flexibility,” says Kay Sargent, Director of WorkPlace at HOK.

Market Data | Oct 24, 2016

New construction starts in 2017 to increase 5% to $713 billion

Dodge Outlook Report predicts moderate growth for most project types – single family housing, commercial and institutional building, and public works, while multifamily housing levels off and electric utilities/gas plants decline.

High-rise Construction | Oct 21, 2016

The world’s 100 tallest buildings: Which architects have designed the most?

Two firms stand well above the others when it comes to the number of tall buildings they have designed.

Market Data | Oct 19, 2016

Architecture Billings Index slips consecutive months for first time since 2012

“This recent backslide should act as a warning signal,” said AIA Chief Economist, Kermit Baker.

Market Data | Oct 11, 2016

Building design revenue topped $28 billion in 2015

Growing profitability at architecture firms has led to reinvestment and expansion

Market Data | Oct 4, 2016

Nonresidential spending slips in August

Public sector spending is declining faster than the private sector.

Industry Research | Oct 3, 2016

Structure Tone survey shows cost is still a major barrier to building green

Climate change, resilience and wellness are also growing concerns.