Through September, spending on nonresidential construction was up 9.2%, to $883.9 billion, according to preliminary estimates by the Commerce Department’s Bureau of the Census. Sectors hard-hit by the coronavirus pandemic—including lodging, retail/commercial, and even office—were showing signs of life.

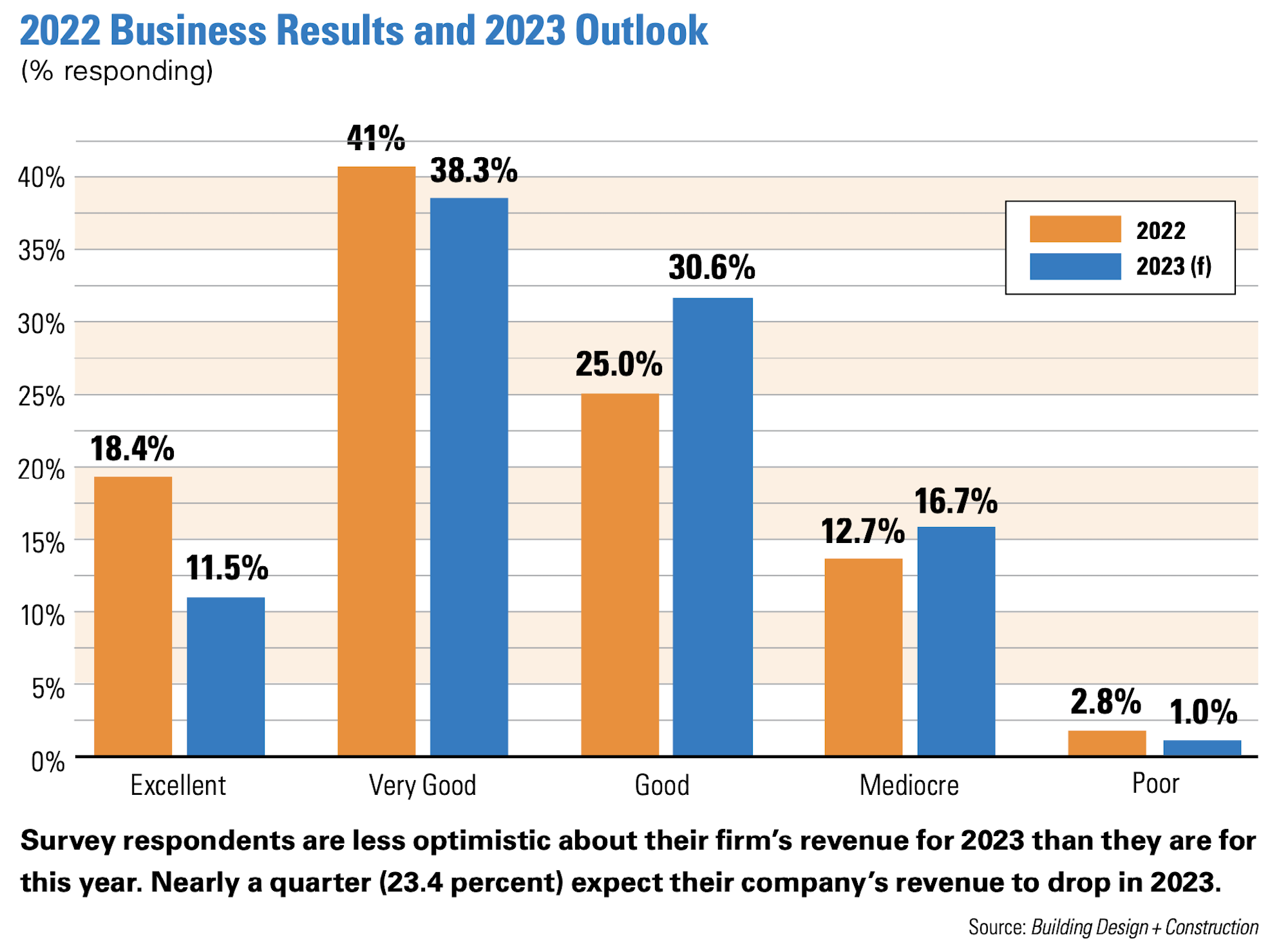

So it makes sense that a recent polling of 212 architects, engineers, contractors, and developer/owners found nearly three-fifths of respondents—59.4%—rating 2022 an “excellent” or “good” business year. Only 15.6% rated the year “mediocre” or “poor.”

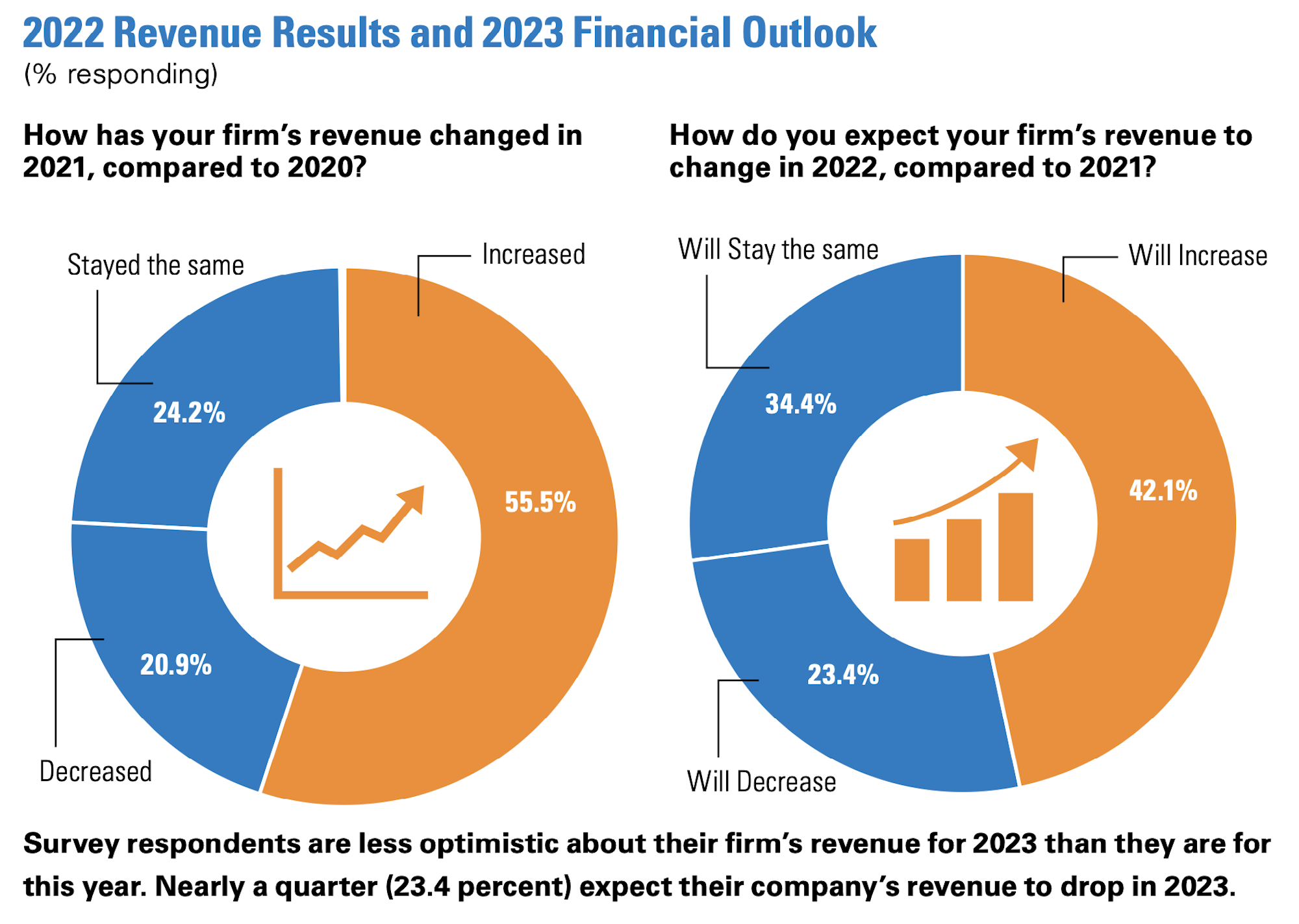

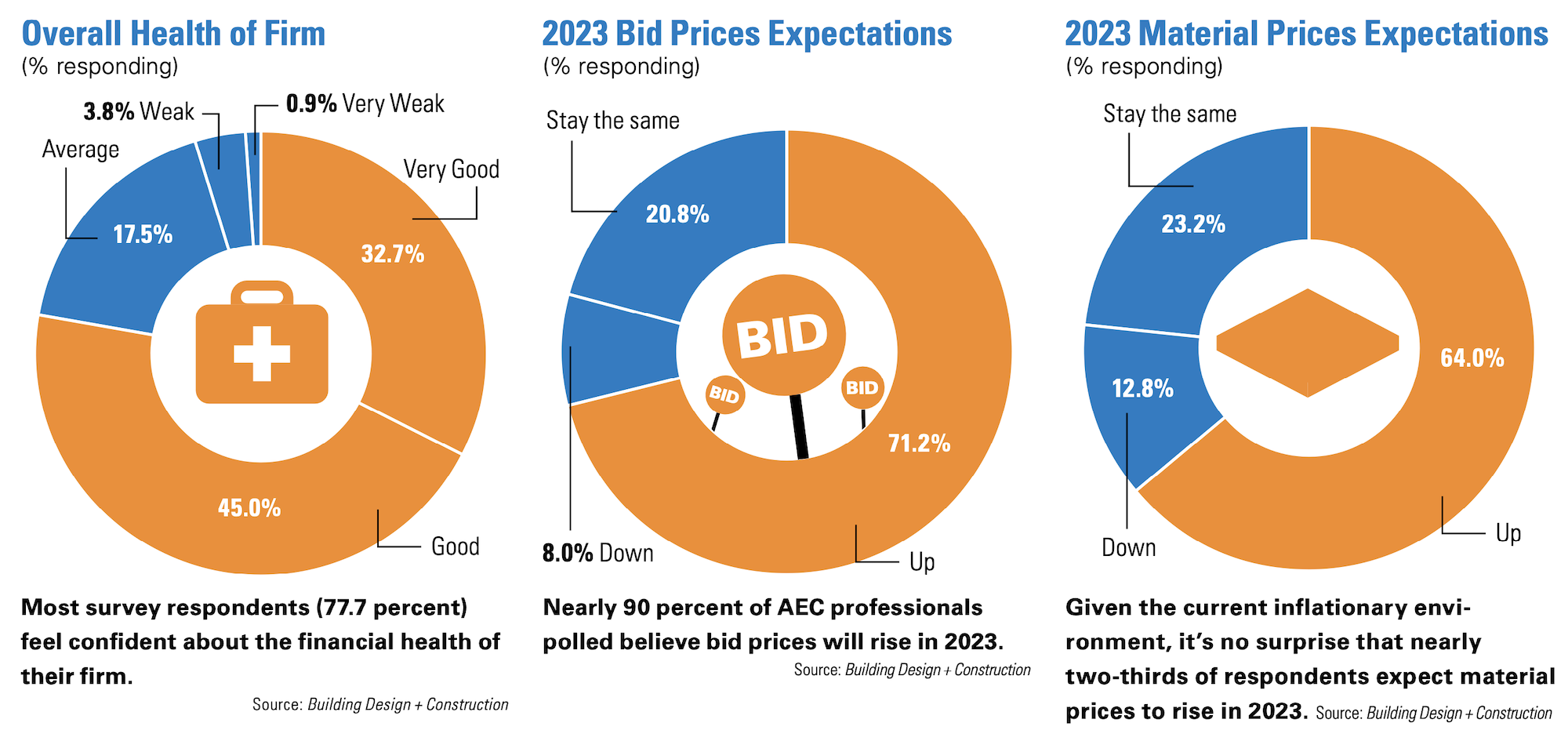

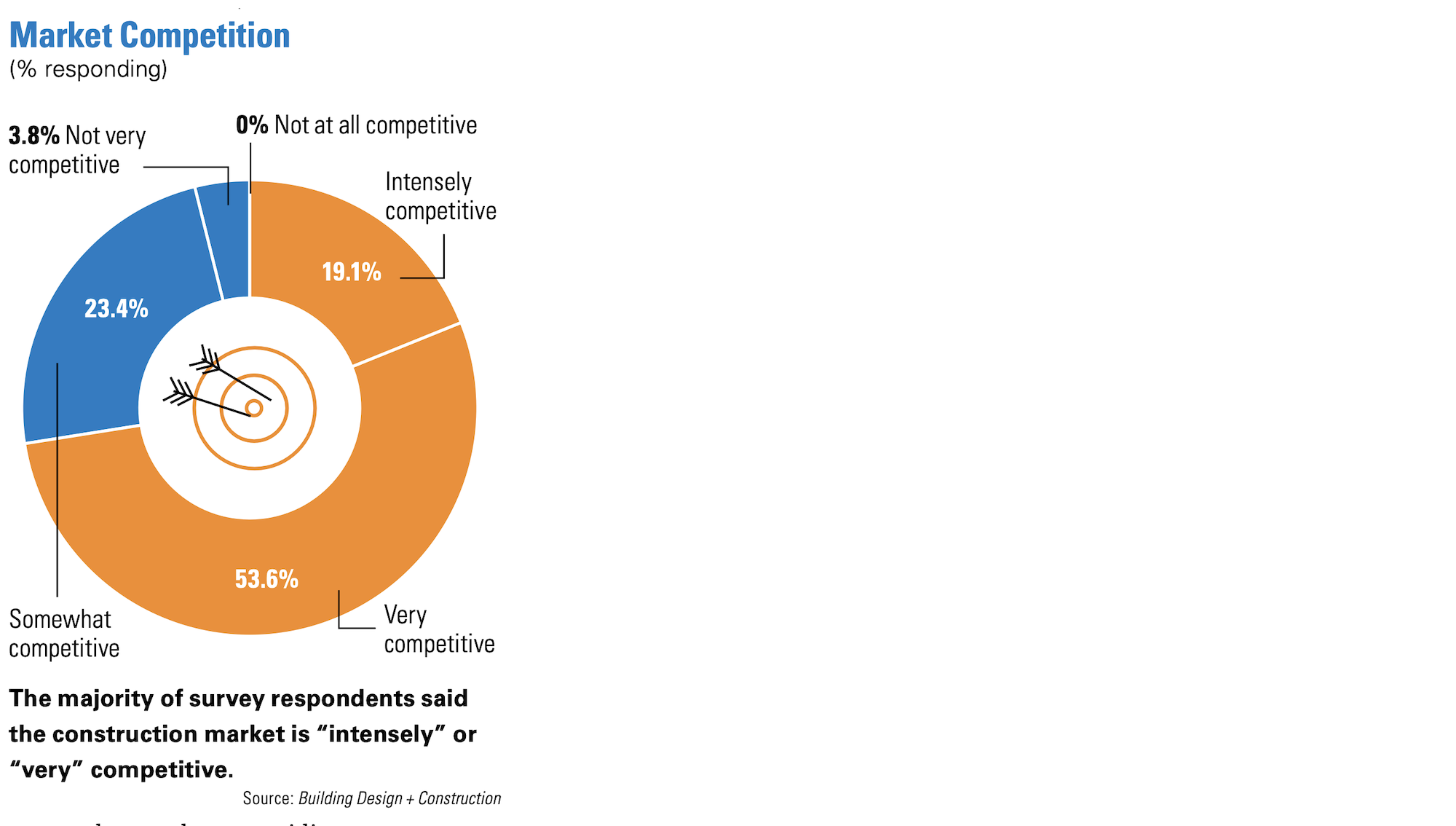

The vast majority of firms, 77.7%, rated their overall health “very good” or “good.” Conversely, only 4.7% saw their firms’ financial condition as either “weak” or “very weak.” Among the firms polled, 55% confirmed their revenue had increased, and another 20.9% said their revenue was level with last year’s. Gains were achieved despite nearly three-quarters of the firms surveyed characterizing the construction/materials market hobbled by supply-chain snags as “intensely” or “very” competitive.

Euphoria, though, might be short-lived, and firms are tempering their prognoses about the future. Nearly one-quarter—23.4%—expect their revenue to be down in 2023, and another 34.4% predict a flat year. Competition ranked third, behind general economic conditions and inflation, as the most important concern AEC firms believe they will face next year. Nearly two-thirds—64%—anticipate that materials prices will continue to rise in 2023. An even higher number, 71.2%, said they were girding for increases in bid prices for projects.

Our poll also found at least one-fifth of firms are concerned about the availability of capital funding for projects, regulations, cashflow management, and keeping their staffs motivated.

When asked about what business development strategies they planned to deploy next year, more than half—53.4%—said they would hire selectively to burnish their firms’ competitiveness, and 47.1% were planning to step up their staff training and education to enhance competitiveness.

Other business strategies these firms are plotting include increasing their marketing and public relations (25.3% of firms polled currently don’t use social media, and among that do LinkedIn is their preferred platform), investing more in technology, and creating new service or business opportunity.

U.S. design and construction firms pick their battles, sector by sector

Our survey asked AEC firms to assess their prospects in 18 construction sectors. Sizable percentages (at least 30%) were hopeful about business for airports, data centers, government/military buildings, healthcare, industrial/warehouse, multifamily and senior living residential, science + technology, and university. At least 20% of respondents saw their prospects as “average” for performing arts centers, hospitality, K-12 education, and sports and recreations. AEC firms placed offices and interior fitouts, religious, and retail/commercial in the “weak” or “very weak” categories.

Here's a closer look at their responses. Keep in mind that these firms aren’t active in every sector, so the numbers providing ratings were smaller than the total in each category. It’s also worth noting that nearly one-third of the AEC firms polled generate between 25% and 74% of their annual business from reconstruction projects:

• Healthcare appears to hold out the greatest opportunities for next year. More than 45% of respondents rated their prospects in this sector as excellent or good. Multifamily received those ratings from 43.1% or AEC firms polled, industrial/warehouse from 39.7%, and data centers from 37.8%.

• Through September, construction spending in the office sector was up only 0.7%, according to Census Bureau estimates. The AEC firms that responded to our survey aren’t anticipating a rebound in this sector any time soon: 41.3% rated their prospects weak or very week. Another 23.5% gave the same ratings to office interiors and fitouts.

Even though Census estimates that the commercial sector (which encompasses retail) was up 22.4% through September, our survey’s respondents are still taking a wait-and-see approach, as 33.3% saw their prospects in retail next year as weak or very weak.

• 29% of respondents said their firms don’t build in the retail sector. And even with the uptick in firms that have expanded their practices and services, only around 10% of our survey’s respondents see mergers or acquisitions in their immediate futures. Our survey reveals an industry whose firms, in many cases, focus on a limited array of typologies and clients, and leave other sectors to specialists.

It was not surprising that 53.2% of respondent firms aren’t building airports and 41.2% aren’t active in the religious sector. Only about half of respondent firms—46.2%—engage performing arts center projects, and 44.3% keep their distances from data centers. But even some of the broader sectors, notably education, find between 30% and 33% of respondent firms absent. Nearly two-fifths aren’t active in science + technology construction, either, and more than two-fifths don’t build in the multifamily sector.

Related Stories

Market Data | Apr 6, 2017

Architecture marketing: 5 tools to measure success

We’ve identified five architecture marketing tools that will help your firm evaluate if it’s on the track to more leads, higher growth, and broader brand visibility.

Market Data | Apr 3, 2017

Public nonresidential construction spending rebounds; overall spending unchanged in February

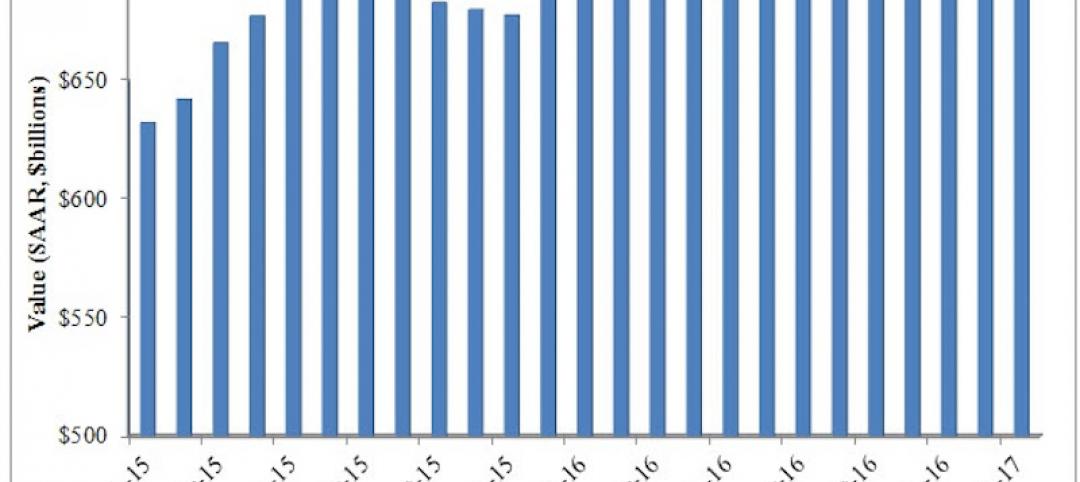

The segment totaled $701.9 billion on a seasonally adjusted annualized rate for the month, marking the seventh consecutive month in which nonresidential spending sat above the $700 billion threshold.

Market Data | Mar 29, 2017

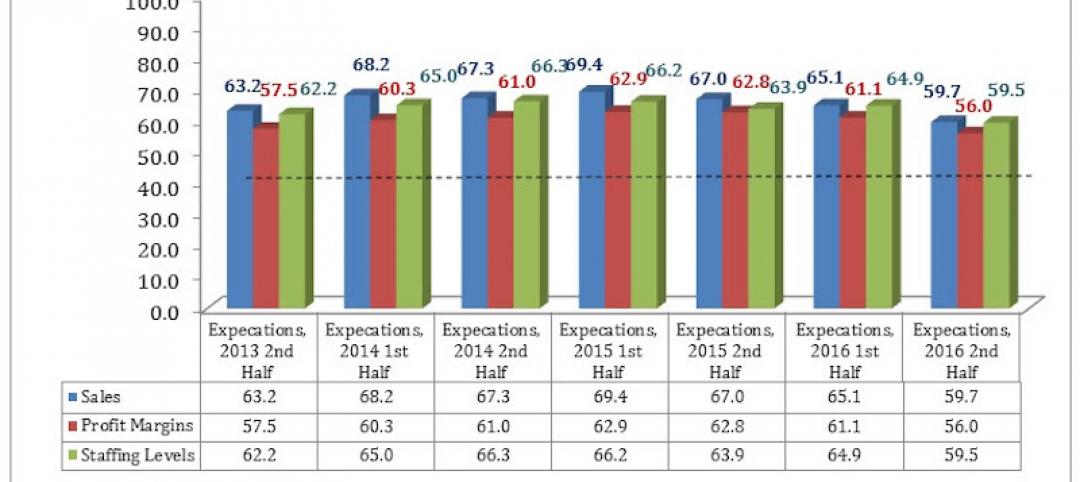

Contractor confidence ends 2016 down but still in positive territory

Although all three diffusion indices in the survey fell by more than five points they remain well above the threshold of 50, which signals that construction activity will continue to be one of the few significant drivers of economic growth.

Industry Research | Mar 24, 2017

The business costs and benefits of restroom maintenance

Businesses that have pleasant, well-maintained restrooms can turn into customer magnets.

Industry Research | Mar 22, 2017

Progress on addressing US infrastructure gap likely to be slow despite calls to action

Due to a lack of bipartisan agreement over funding mechanisms, as well as regulatory hurdles and practical constraints, Moody’s expects additional spending to be modest in 2017 and 2018.

Industry Research | Mar 21, 2017

Staff recruitment and retention is main concern among respondents of State of Senior Living 2017 survey

The survey asks respondents to share their expertise and insights on Baby Boomer expectations, healthcare reform, staff recruitment and retention, for-profit competitive growth, and the needs of middle-income residents.

Industry Research | Mar 14, 2017

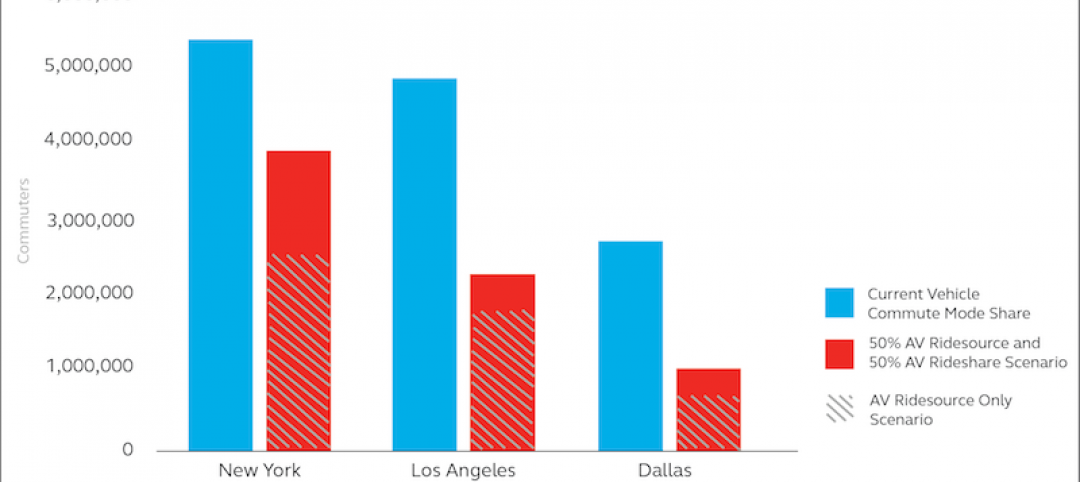

6 ways cities can prepare for a driverless future

A new report estimates 7 million drivers will shift to autonomous vehicles in 3 U.S. cities.

Office Buildings | Mar 7, 2017

Large creative office projects generate staggering returns for property investors

A new Transwestern report examines the adaptive reuse trend across the U.S.

Industry Research | Mar 7, 2017

These are the 10 most expensive cities in the world to build in

Paris, Frankfurt, and Macau are all on the list, but none of them are more expensive than the city in the number one spot.

Office Buildings | Mar 2, 2017

White paper from Perkins Eastman and Three H examines how design can inform employee productivity and wellbeing

This paper is the first in a planned three-part series of studies on the evolution of diverse office environments and how the contemporary activity-based workplace (ABW) can be uniquely tailored to support a range of employee personalities, tasks and work modes.