While materials and labor price hikes continue to create havoc, they don’t seem to be shackling demand or activity for nonresidential construction, according to Skanska’s Summer 2023 Construction Market Trends Report, which looks at pricing and supply-chain trends for 14 product groups, and forecasts local construction costs for 21 markets across the U.S.

“Despite being the most expensive construction environment we have ever experienced … the health of the construction industry remains quite strong,” wrote Steve Stouthamer, Executive Vice President, Project Planning, Skanska USA Building, and one of the Skanska executives who produced this 43-page report. Stouthamer added that commercial office development and residential markets remain the most challenged by interest rate pressures, and offices are still contending with high vacancy rates.

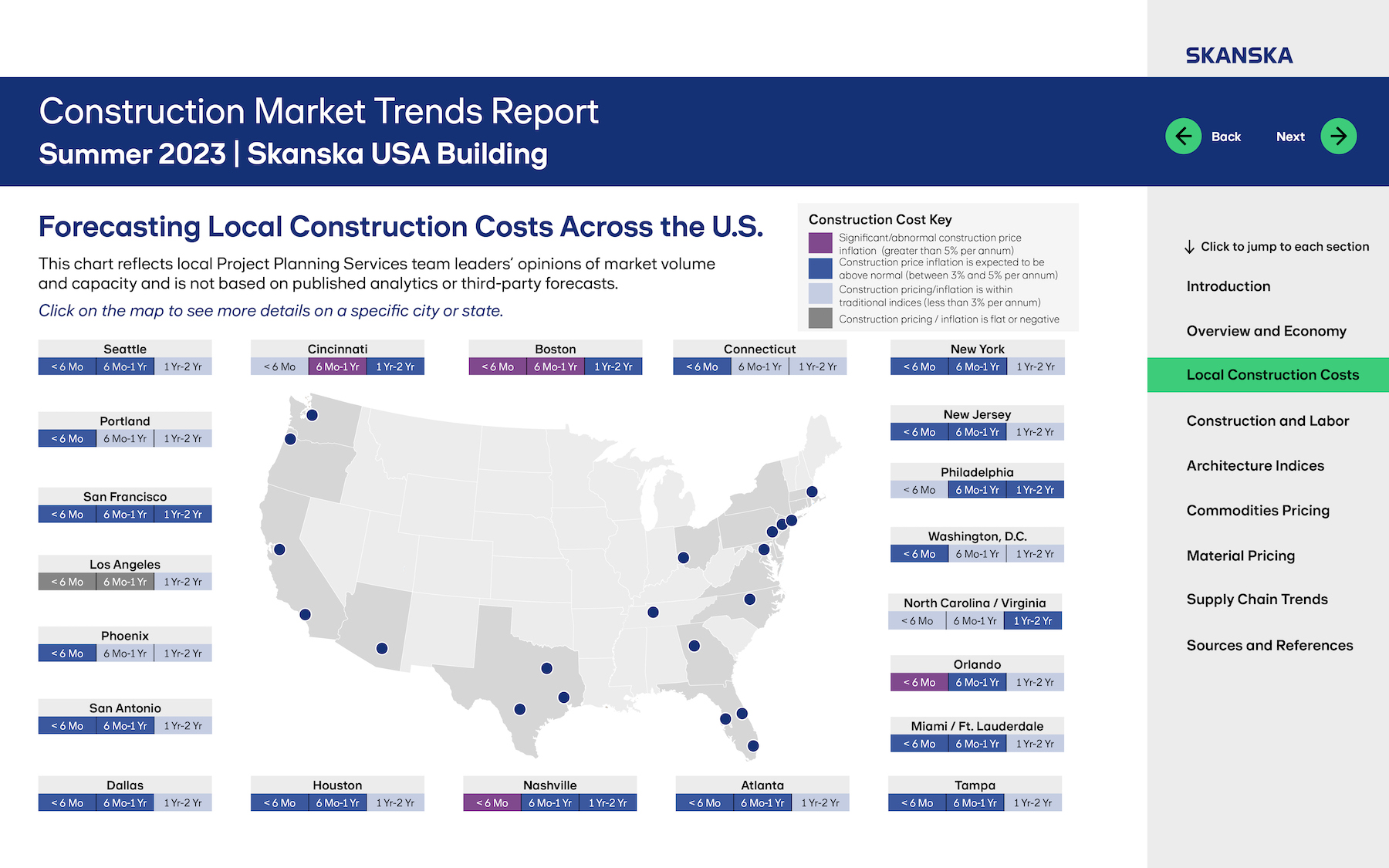

Skanska anticipates significant or abnormal construction price inflation (greater than 5 percent per year) over the next six to 12 months in Nashville, Boston, Cincinnati, and Orlando. Indeed, with the exception of Los Angeles and the North Carolina/Virginia region, the other markets that Skanksa’s report tracks are expected to experience at least above-normal (3-5% per annum) construction price inflation over the next six to 24 months.

Different sectors driving local economies

Skanska evaluated business conditions and prospects for each of the markets it tracked.

Take Seattle, for example: New labor agreements, coupled with manpower shortages and the availability of materials and equipment, are pushing construction prices up. But much-needed tourism is returning there, re-energizing the retail, hospitality, and aviation sectors. And outside of the downtown core, Skanska saw “plenty of opportunities for new projects,” notably in K-12, mass transit, and aviation.

In Philadelphia, the same inflation dynamic exists. But that hasn’t stopped Philly’s healthcare sector from gaining momentum, and life sciences continues to be vibrant, “with new capital projects and office as clients realize the importance of new amenity space to bring staff back to work.” Skanska also foresees a laggard Higher Ed sector in recovery, with several new projects under consideration for this year and next.

Skanska’s report cited the Architecture Billings Index in June as another barometer of construction demand, and the news was mixed. While business conditions have improved for architecture firms in all regions except the West, the pace of growth inquiries since March has slowed, and the value of new design contracts has declined.

An uncertain stability for construction costs

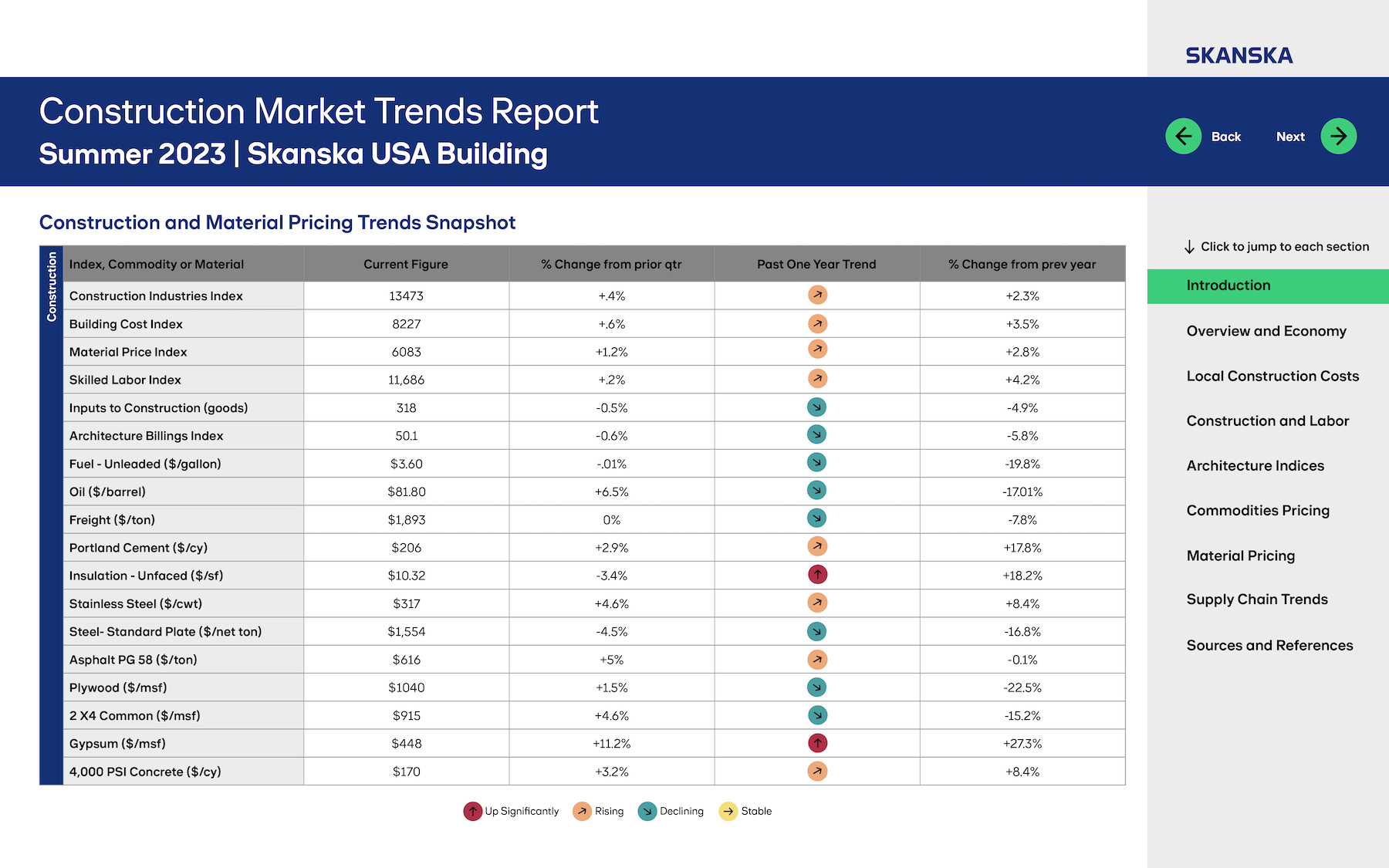

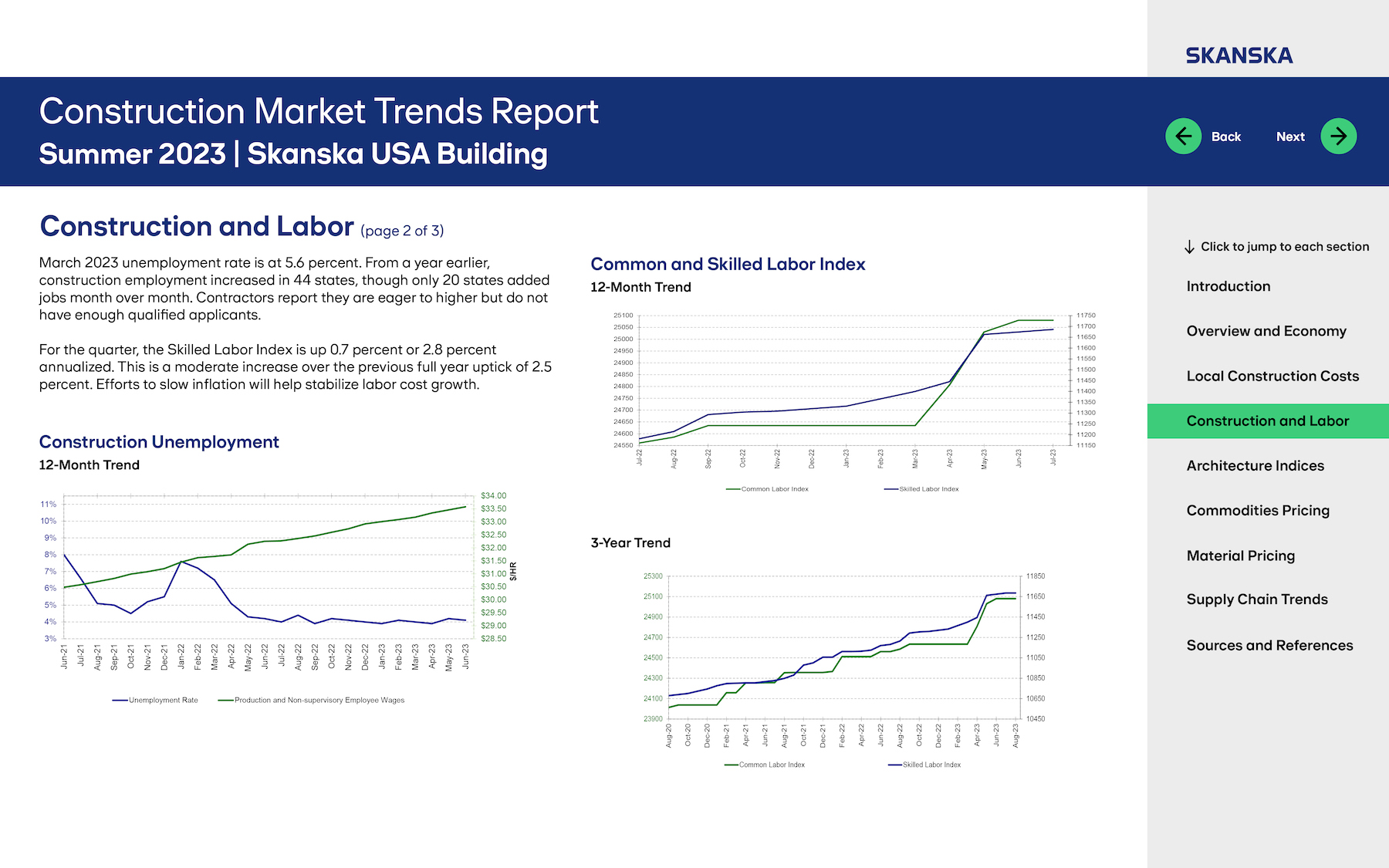

Every metro market tracked in Skanska’s report has had to cope with rising costs for materials and labor, which Skanska estimates rose nationally by 4.2% and 2.8% respectively, compared to the same period a year ago. But only two product categories—unfaced insulation and 4,000-psi gypsum—were up significantly: by 18.2% and 27.3%, respectively. Conversely, the costs of three product groups tracked–-standard plate steel, plywood, and 2x4s—were trending downward. Skanska also reported declines in the cost of fuel, oil, and freight, though the firm expected fuel costs to remain “elevated” through the rest of this year.

Softness in asphalt pricing is tied to lower seasonal demand, and Skanska expects prices for this material to increase again based on infrastructure work. Cement and concrete prices continued to improve early this year, but could increase dramatically as the weather got warmer. The pricing for structural steel has also stabilized, but Skanska expects a slight uptick in the future. Pricing for aluminum and copper, despite moderate declines, remain high compared to historical levels, as demand is strong.

As for product availability, Skanska said that over the previous quarter, the construction supply chain has continued to improve, “most notably around raw material prices for PVC resins, steel, copper, and lumber.” The supply chain for roofing products “has fully recovered.” Inventory for plumbing and fixtures appears to be healthy.

The challenges lie with HVAC and electrical gear availability. though several HVAC equipment manufacturers have reported improvements in their backlogs of orders due to increased factory capacity. (The one glaring exception is chillers that still have lead times of between 45 and 65 weeks.)

Skanska predicted that the construction industry’s lean toward electrification, as well as investment in data centers, will likely last for several more years. Investment in production capacity for electrical equipment products should allow manufacturers to be able to keep up with “persistent demand.”

Regional takes on construction costs

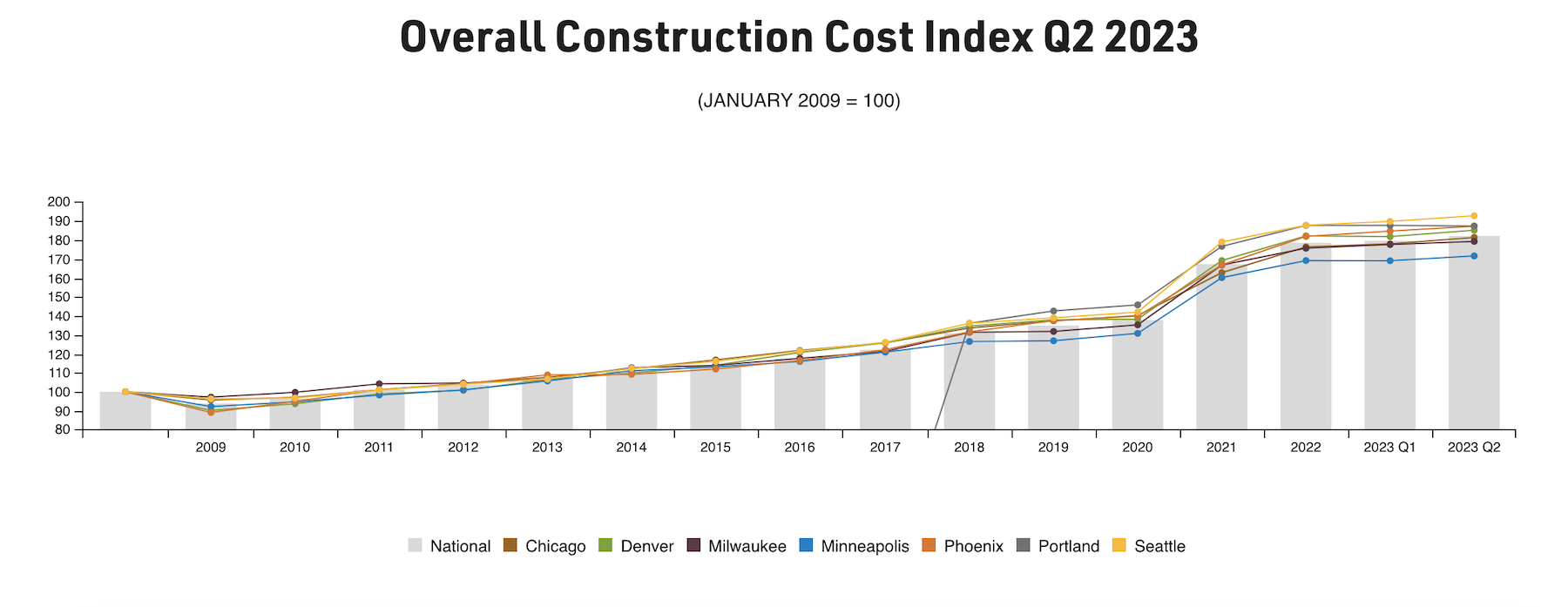

Looking at market conditions from a slightly narrower perspective, Mortenson’s just-released nonresidential Construction Cost Index, which tracks quarterly spending and inflation trends in seven markets—Seattle, Portland, Denver, Phoenix, Milwaukee, Chicago, and Minneapolis—stood at 182 nationally in the second quarter of 2023, or 8.72% higher than for all of 2021. Within that time frame, Phoenix saw the biggest increase in its index (12.22% to 187.3), and Portland the smallest (6.06% to 187.4).

“Our construction cost index shows a continued flattening of material costs, suggesting pandemic, supply-chain, and inflation-related increases experienced over the last two years have largely abated,” states Mortenson. Nationally, nonresidential construction costs during Q223 increased year over year by 2.94%. Mortenson’s overall outlook for nonresidential construction remains optimistic but also cautious, primarily because increasing labor costs “are beginning to offset the stabilization.”

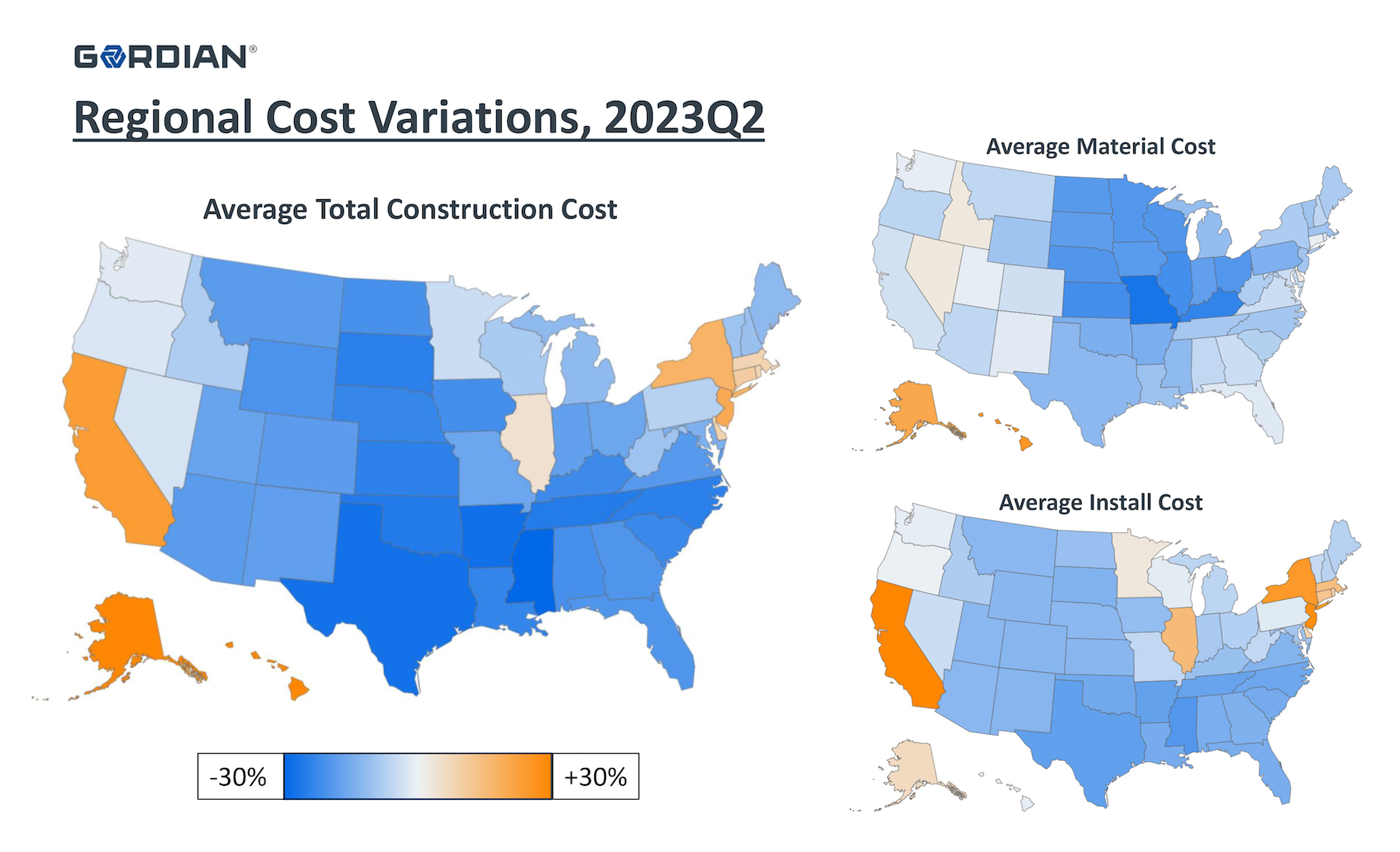

Data from Gordian’s RSMeans City Cost Index illustrates how dramatically costs differ by region, and how doing business in coastal markets is more expensive.

The City Cost Index takes into account the costs of labor, materials, and equipment, and compares that aggregate number to a national average of 30 major U.S. cities. The cost model encompasses 66 materials, 21 trades, and six pieces of equipment (plus fuel and maintenance costs).

The map above illustrates regional cost differences during the second quarter of 2023. Here are some takeaways:

•The average costs of construction are highest across California, Hawaii, and Alaska; and lowest across Mississippi;

•Materials costs are highest as you move farther east and west from the Mississippi River;

•Costs for installation (labor and equipment) are highest in the West and Northeast.

Related Stories

Self-Storage Facilities | Dec 16, 2022

Self-storage development booms in high multifamily construction areas

A 2022 RentCafe analysis finds that self-storage units swelled in conjunction with metros’ growth in apartment complexes.

Market Data | Dec 13, 2022

Contractors' backlog of work reaches three-year high

U.S. construction firms have, on average, 9.2 months of work in the pipeline, according to ABC's latest Construction Backlog Indicator.

Contractors | Dec 6, 2022

Slow payments cost the construction industry $208 billion in 2022

The cost of floating payments for wages and invoices represents $208 billion in excess cost to the construction industry, a 53% increase from 2021, according to a survey by Rabbet, a provider of construction finance software.

Mass Timber | Dec 1, 2022

Cross laminated timber market forecast to more than triple by end of decade

Cross laminated timber (CLT) is gaining acceptance as an eco-friendly building material, a trend that will propel its growth through the end of the 2020s. The CLT market is projected to more than triple from $1.11 billion in 2021 to $3.72 billion by 2030, according to a report from Polaris Market Research.

Market Data | Nov 15, 2022

Construction demand will be a double-edged sword in 2023

Skanska’s latest forecast sees shorter lead times and receding inflation, but the industry isn’t out of the woods yet.

Reconstruction & Renovation | Nov 8, 2022

Renovation work outpaces new construction for first time in two decades

Renovations of older buildings in U.S. cities recently hit a record high as reflected in architecture firm billings, according to the American Institute of Architects (AIA).

Market Data | Nov 3, 2022

Building material prices have become the calm in America’s economic storm

Linesight’s latest quarterly report predicts stability (mostly) through the first half of 2023

Building Team | Nov 1, 2022

Nonresidential construction spending increases slightly in September, says ABC

National nonresidential construction spending was up by 0.5% in September, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau.

Hotel Facilities | Oct 31, 2022

These three hoteliers make up two-thirds of all new hotel development in the U.S.

With a combined 3,523 projects and 400,490 rooms in the pipeline, Marriott, Hilton, and InterContinental dominate the U.S. hotel construction sector.

Codes and Standards | Oct 26, 2022

‘Landmark study’ offers key recommendations for design-build delivery

The ACEC Research Institute and the University of Colorado Boulder released what the White House called a “landmark study” on the design-build delivery method.