Prices for inputs to construction fell 0.5% in August but are 8.1% higher than at the same time one year ago, according to an Associated Builders and Contractors analysis of Bureau of Labor Statistics data released today. Nonresidential construction input prices fell 0.4% in August but are up 8.3% year-over-year. Softwood lumber prices plummeted 9.6% in August yet are up 5% on a yearly basis (down from a 19.5% increase year-over-year in July).

“Stakeholders will be tempted to look upon this month’s inputs to the construction Producer Price Index report as evidence that the cycle of rapidly rising prices is nearing an end,” said ABC Chief Economist Anirban Basu. “Prices of key inputs have been high for quite some time, which would tend to induce a larger supply of these items and, in turn, moderate prices.

“Some may also conclude that ongoing progress in trade negotiations with nations including Mexico and Canada has helped to moderate input prices. Still others might point to growing economic turmoil in nations like Turkey and Argentina. Economists would also note the likely impact of a strong U.S. dollar on import and commodity prices. While all of these are potential explanations, another possibility is that the August data are largely statistical aberrations. Metal prices continue to move higher on a monthly basis, with recently enacted tariffs representing a likely explanation.

“Softwood lumber, the subject of an ongoing trade dispute with the Canadians, experienced a significant dip in price on a monthly basis,” said Basu. “The price of softwood may have fallen in response to a weakening single-family residential construction market, as home builders have been wrestling with a combination of labor shortages, higher land prices and weakening demand due to higher mortgage rates.

“In the final analysis, the falling input prices trend likely won’t continue,” said Basu. “The economy is still strong, and ABC’s Construction Backlog Indicator remains elevated in both public and private construction segments. Inflation expectations have shifted, with purchasers of construction services now anticipating price increases and therefore more willing to accommodate them. Moreover, issues related to tariffs and trade wars persist. Accordingly, estimators and construction companies continue to consider the likelihood of additional input price increases for the balance of 2018 and into 2019.”

Related Stories

Industry Research | Apr 25, 2023

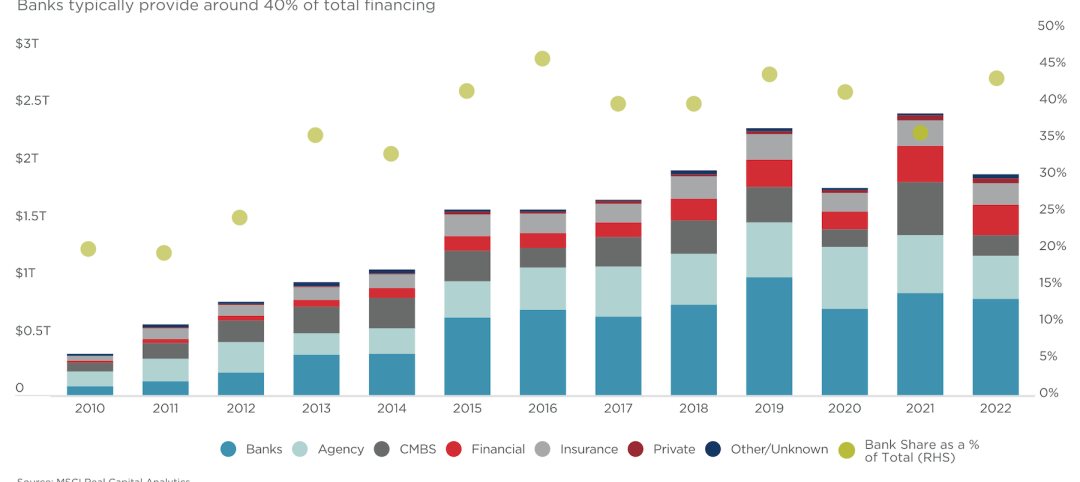

The commercial real estate sector shouldn’t panic (yet) about recent bank failures

A new Cushman & Wakefield report depicts a “well capitalized” banking industry that is responding assertively to isolated weaknesses, but is also tightening its lending.

Architects | Apr 21, 2023

Architecture billings improve slightly in March

Architecture firms reported a modest increase in March billings. This positive news was tempered by a slight decrease in new design contracts according to a new report released today from The American Institute of Architects (AIA). March was the first time since last September in which billings improved.

Contractors | Apr 19, 2023

Rising labor, material prices cost subcontractors $97 billion in unplanned expenses

Subcontractors continue to bear the brunt of rising input costs for materials and labor, according to a survey of nearly 900 commercial construction professionals.

Data Centers | Apr 14, 2023

JLL's data center outlook: Cloud computing, AI driving exponential growth for data center industry

According to JLL’s new Global Data Center Outlook, the mass adoption of cloud computing and artificial intelligence (AI) is driving exponential growth for the data center industry, with hyperscale and edge computing leading investor demand.

Healthcare Facilities | Apr 13, 2023

Healthcare construction costs for 2023

Data from Gordian breaks down the average cost per square foot for a three-story hospital across 10 U.S. cities.

Higher Education | Apr 13, 2023

Higher education construction costs for 2023

Fresh data from Gordian breaks down the average cost per square foot for a two-story college classroom building across 10 U.S. cities.

Market Data | Apr 13, 2023

Construction input prices down year-over-year for first time since August 2020

Construction input prices increased 0.2% in March, according to an Associated Builders and Contractors analysis of U.S. Bureau of Labor Statistics Producer Price Index data released today. Nonresidential construction input prices rose 0.4% for the month.

Market Data | Apr 11, 2023

Construction crane count reaches all-time high in Q1 2023

Toronto, Seattle, Los Angeles, and Denver top the list of U.S/Canadian cities with the greatest number of fixed cranes on construction sites, according to Rider Levett Bucknall's RLB Crane Index for North America for Q1 2023.

Contractors | Apr 11, 2023

The average U.S. contractor has 8.7 months worth of construction work in the pipeline, as of March 2023

Associated Builders and Contractors reported that its Construction Backlog Indicator declined to 8.7 months in March, according to an ABC member survey conducted March 20 to April 3. The reading is 0.4 months higher than in March 2022.

Market Data | Apr 6, 2023

JLL’s 2023 Construction Outlook foresees growth tempered by cost increases

The easing of supply chain snags for some product categories, and the dispensing with global COVID measures, have returned the North American construction sector to a sense of normal. However, that return is proving to be complicated, with the construction industry remaining exceptionally busy at a time when labor and materials cost inflation continues to put pricing pressure on projects, leading to caution in anticipation of a possible downturn. That’s the prognosis of JLL’s just-released 2023 U.S. and Canada Construction Outlook.