Slower growth in the general economy, brought on by seemingly mounting national and international vulnerabilities, is putting downward pressure on the construction industry, whose sectors expanded last year by 20% or more but are moderating to single-digit growth levels.

That’s the viewpoint of the American Institute of Architects’ semiannual Consensus Construction Forecast Panel, which expects building construction spending to increase by just under 6%, its growth rate through the first half of the year, through 2017.

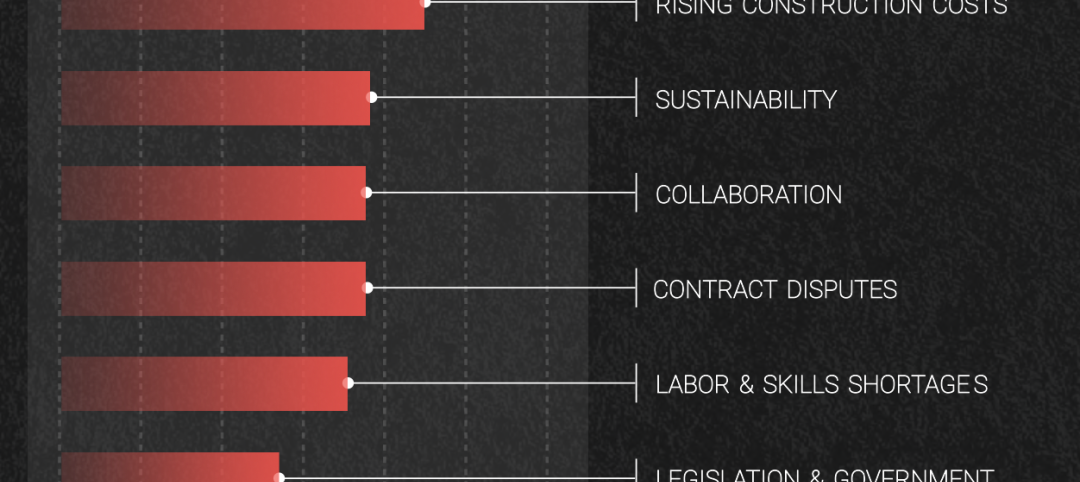

To view an interactive chart comparing the forecasts from the seven market watchers on the Panel, click here.

AIA puts out its Consensus to project business conditions for the coming 12 to 18 months. Kermit Baker, Hon. AIA, the Institute’s chief economist, notes that several factors—job growth, consumer confidence, low interest and inflation rates, and a trending single-family housing market—offer positive economic signs.

Good reception is also coming from AIA’s Architectural Buildings Index, a historically reliable indicator of future spending in the nonresidential sector. The latest data indicate that architectural firms are increasing their backlog of project activity.

Still, there is a growing list of issues “that threatens to unhinge this economic expansion, both national and international,” Baker writes.

These include:

•A weak manufacturing sector, which has declined 13 of the past 17 months dating back to the beginning of 2015.

•Sagging international economies that could diminish U.S. exports. China, Brazil, and Russia “continue to face difficulties,” observes Baker. And the U.K.’s recent split from the European Union could instigate more restrictive trade policies. On the other hand, a stronger U.S. dollar provides incentives for increasing imports.

•The upcoming presidential election, and the “unusually high” level of uncertainty regarding post-election policies.

Baker cites a recent Urban Land-generated consensus forecast of real estate trends that suggests “we are in the latter stages of this current real estate cycle,” where vacancy rates are expected to increase, and rent increases to slow, for multifamily housing and hotel rooms through 2017 and 2018.

Spending on hotel construction is on pace to increase by a still-healthy 7.6% in 2017, but down from 17.9% in 2016, according to AIA’s consensus forecast. Office space spending will grow by 14.7% this year, but only by 7.5% next.

The institutional side is expected rise by 6.7% this year and next. Healthcare facilities spending should increase to 5% next year, from 2.3% in 2016. Public Safety is expected to recover from a 3.7% decline to a 3.3% gain next year. Spending on Education construction, one of the industry’s big tickets, should see a slight downtick in growth, to 6.3% in 2017 from 6.5% this year.

Related Stories

Multifamily Housing | Jun 29, 2023

5 ways to rethink the future of multifamily development and design

The Gensler Research Institute’s investigation into the residential experience indicates a need for fresh perspectives on residential design and development, challenging norms, and raising the bar.

Apartments | Jun 27, 2023

Average U.S. apartment rent reached all-time high in May, at $1,716

Multifamily rents continued to increase through the first half of 2023, despite challenges for the sector and continuing economic uncertainty. But job growth has remained robust and new households keep forming, creating apartment demand and ongoing rent growth. The average U.S. apartment rent reached an all-time high of $1,716 in May.

Contractors | Jun 26, 2023

Most top U.S. contractors rarely deliver projects on time: new study

About 63% of leading U.S. contractors are delivering projects out of schedule, according to a survey of over 300 C-suite executives and owners in the construction industry by XYZ Reality. The study implies that the industry is struggling with significant backlogs due, in part, to avoidable defects, scan, and rework.

Industry Research | Jun 15, 2023

Exurbs and emerging suburbs having fastest population growth, says Cushman & Wakefield

Recently released county and metro-level population growth data by the U.S. Census Bureau shows that the fastest growing areas are found in exurbs and emerging suburbs.

Contractors | Jun 13, 2023

The average U.S. contractor has 8.9 months worth of construction work in the pipeline, as of May 2023

Associated Builders and Contractors reported that its Construction Backlog Indicator remained unchanged at 8.9 months in May, according to an ABC member survey conducted May 20 to June 7. The reading is 0.1 months lower than in May 2022. Backlog in the infrastructure category ticked up again and has now returned to May 2022 levels. On a regional basis, backlog increased in every region but the Northeast.

Industry Research | Jun 13, 2023

Two new surveys track how the construction industry, in the U.S. and globally, is navigating market disruption and volatility

The surveys, conducted by XYZ Reality and KPMG International, found greater willingness to embrace technology, workplace diversity, and ESG precepts.

| Jun 5, 2023

Communication is the key to AEC firms’ mental health programs and training

The core of recent awareness efforts—and their greatest challenge—is getting workers to come forward and share stories.

Mass Timber | Jun 2, 2023

First-of-its-kind shake test concludes mass timber’s seismic resilience

Last month, a 10-story mass timber structure underwent a seismic shake test on the largest shake table in the world.

Contractors | May 24, 2023

The average U.S. contractor has 8.9 months worth of construction work in the pipeline, as of April 2023

Contractor backlogs climbed slightly in April, from a seven-month low the previous month, according to Associated Builders and Contractors.

Multifamily Housing | May 23, 2023

One out of three office buildings in largest U.S. cities are suitable for residential conversion

Roughly one in three office buildings in the largest U.S. cities are well suited to be converted to multifamily residential properties, according to a study by global real estate firm Avison Young. Some 6,206 buildings across 10 U.S. cities present viable opportunities for conversion to residential use.