Last year’s boon in single-family housing construction will have an impact on the availability and cost of building materials for nonresidential construction in 2021, which is expected to be a year of “decreasing work volume,” according to JLL’s latest Construction Forecast being released today.

Nonresidential starts were down 24% last year, and are expected to decline again in 2021. Yet, JLL sees an industry that has become more resilient and better positioned to function during the pandemic recovery.

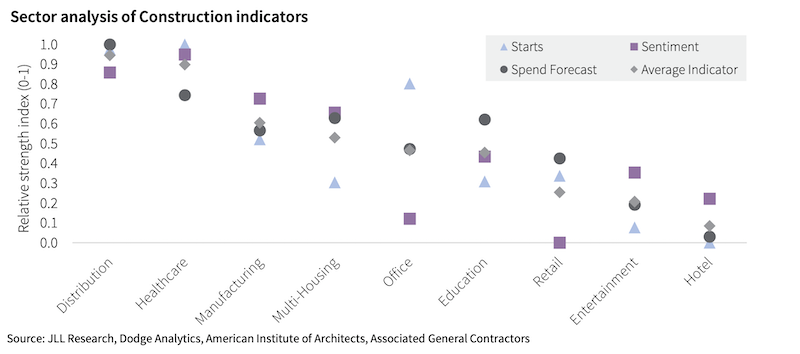

Healthcare and industrial should be the growth winners in construction spending this year. Chart: JLL

Healthcare and industrial should be the growth winners in construction spending this year. Chart: JLL

This recovery won’t be like the last one during the Great Recession in the late 2000s. For one thing, the range between sector forecasts is wider.

JLL analyzed three indicators of future growth: construction starts, construction industry sentiment, and forecast construction spending across nine nonresidential sectors. The clear winners, in its estimation, will be distribution and healthcare. The clear stragglers: hotels and entertainment. The office sector shows the least consensus.

LUMBER PRICING WILL CONTINUE TO BE VOLATILE

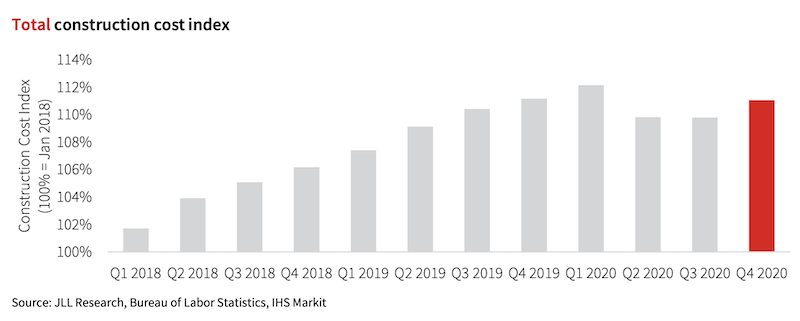

The boon in new-home construction is having an impact on overall construction costs. Chart: JLL

The boon in new-home construction is having an impact on overall construction costs. Chart: JLL

In addition, this has not been a total construction shutdown. Single-family housing starts increased by 11% last year, and have continued to grow since last May. (According to the latest Census Bureau estimates, single-family starts in January, at an annualized rate of 1,269,000 units, were up 29.9% over the same month in 2020.)

Residential construction employment was also up last year, by 1.2%, while nonres construction employment dipped 3.9%. That growth is affecting labor and materials markets. “The growth in residential is the primary cause of our forecast for elevated cost inflation in the coming year,” states JLL.

This year, it predicts that construction cost increases will be in the higher range between 3.5% and 5.5%. Labor costs will be up in the 2-5% range. Material costs will rise 4-6% and volatility “will remain elevated.” Nonres construction spending will stabilize from the early stages of the pandemic, but still decline between 5% and 8%, although JLL foresees an upswing in the third and fourth quarter, and more typical industry growth in 2022.

One silver lining from the pandemic is that it “spurred three years of construction tech adoption to be condensed into the last nine months of 2020,” observes JLL. It cites a recent Associated General Contractors survey that found contractors planning to increase their spending for all 14 ConTech categories listed.

Labor demand should also continue, although the key to any construction recovery, states JLL, will be how quickly the population is vaccinated against COVID-19. The industry’s labor shortage was a big enough buffer to absorb some of the pandemic’s shock, and through the entire post-pandemic period “there have been more active job openings in construction than at the peak of the last expansion in 2006-2007.”

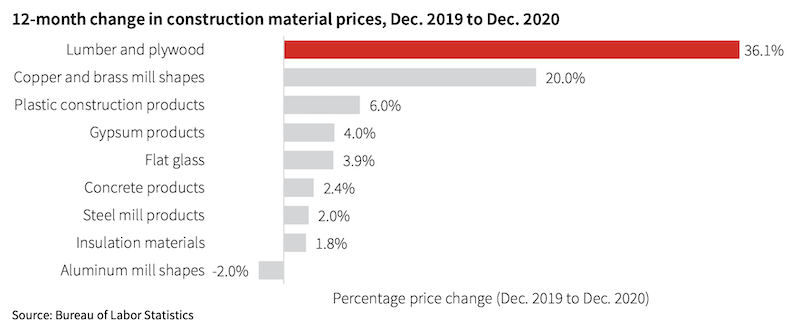

As for materials pricing, volatility will affect lumber, plywood, copper and brass mill shapes. The least volatile, price-wise, should be concrete, flat glass, insulation, and plastic construction products.

Lumber and plywood pricing is expected to remain unpredictable. Chart: JLL

Lumber and plywood pricing is expected to remain unpredictable. Chart: JLL

NEW ADMINISTRATION COULD SHAKE UP CONSTRUCTION

JLL weighed in on the potential impact of the Biden Administration on the construction industry. The next stimulus package, if passed by Congress, should keep the economy’s growth from reversing. A large infrastructure bill “is a good possibility later this year,” which JLL thinks could be an “accelerant” to construction inflation.

Interestingly, JLL doesn’t think either a reduction in immigration restrictions or an increase in the minimum wage to $15 per hour would have a substantive impact on projects, wages, or costs, except in states like Texas where construction wages are lower than the federal rate.

Related Stories

Market Data | Apr 4, 2023

Nonresidential construction spending up 0.4% in February 2023

National nonresidential construction spending increased 0.4% in February, according to an Associated Builders and Contractors analysis of data published by the U.S. Census Bureau. On a seasonally adjusted annualized basis, nonresidential spending totaled $982.2 billion for the month, up 16.8% from the previous year.

Multifamily Housing | Mar 24, 2023

Average size of new apartments dropped sharply in 2022

The average size of new apartments in 2022 dropped sharply in 2022, as tracked by RentCafe. Across the U.S., the average new apartment size was 887 sf, down 30 sf from 2021, which was the largest year-over-year decrease.

Multifamily Housing | Mar 14, 2023

Multifamily housing rent rates remain flat in February 2023

Multifamily housing asking rents remained the same for a second straight month in February 2023, at a national average rate of $1,702, according to the new National Multifamily Report from Yardi Matrix. As the economy continues to adjust in the post-pandemic period, year-over-year growth continued its ongoing decline.

Contractors | Mar 14, 2023

The average U.S. contractor has 9.2 months worth of construction work in the pipeline, as of February 2023

Associated Builders and Contractors reported today that its Construction Backlog Indicator increased to 9.2 months in February, according to an ABC member survey conducted Feb. 20 to March 6. The reading is 1.2 months higher than in February 2022.

Industry Research | Mar 9, 2023

Construction labor gap worsens amid more funding for new infrastructure, commercial projects

The U.S. construction industry needs to attract an estimated 546,000 additional workers on top of the normal pace of hiring in 2023 to meet demand for labor, according to a model developed by Associated Builders and Contractors. The construction industry averaged more than 390,000 job openings per month in 2022.

Market Data | Mar 7, 2023

AEC employees are staying with firms that invest in their brand

Hinge Marketing’s latest survey explores workers’ reasons for leaving, and offers strategies to keep them in the fold.

Multifamily Housing | Feb 21, 2023

Multifamily housing investors favoring properties in the Sun Belt

Multifamily housing investors are gravitating toward Sun Belt markets with strong job and population growth, according to new research from Yardi Matrix. Despite a sharp second-half slowdown, last year’s nationwide $187 billion transaction volume was the second-highest annual total ever.

Contractors | Feb 14, 2023

The average U.S. contractor has nine months worth of construction work in the pipeline

Associated Builders and Contractors reports today that its Construction Backlog Indicator declined 0.2 months to 9.0 in January, according to an ABC member survey conducted Jan. 20 to Feb. 3. The reading is 1.0 month higher than in January 2022.

Office Buildings | Feb 9, 2023

Post-Covid Manhattan office market rebound gaining momentum

Office workers in Manhattan continue to return to their workplaces in sufficient numbers for many of their employers to maintain or expand their footprint in the city, according to a survey of more than 140 major Manhattan office employers conducted in January by The Partnership for New York City.

Giants 400 | Feb 9, 2023

New Giants 400 download: Get the complete at-a-glance 2022 Giants 400 rankings in Excel

See how your architecture, engineering, or construction firm stacks up against the nation's AEC Giants. For more than 45 years, the editors of Building Design+Construction have surveyed the largest AEC firms in the U.S./Canada to create the annual Giants 400 report. This year, a record 519 firms participated in the Giants 400 report. The final report includes 137 rankings across 25 building sectors and specialty categories.