In the third quarter of 2018, the U.S. office market again showed steady improvement, according to Transwestern’s national outlook for the sector. Absorption reached 22.7 million square feet, vacancy remained stable at 10.1%, and asking rents increased by 4.0%, annually.

Ryan Tharp, Research Director in Dallas, said the strong economy has contributed to the office market’s momentum, despite softer income growth in a very tight labor market.

“Real gross domestic product increased at an annualized 3.5%, according to first estimates, and personal consumption contributed 2.7% to that rate,” Tharp said. “Because inflation has remained in line with the Federal Reserve’s target of 2.0%, consumer and business confidence should keep the office market healthy well into 2019.”

A positive sign is that year-to-date net absorption in the office market was 17.1% higher at the end of the third quarter than it was for the same period last year. Dallas-Fort Worth, San Francisco and Denver led in absorption by a significant margin for the prior 12 months, with a combined 13.3 million square feet.

Meanwhile, demand and supply are headed for equilibrium as new construction activity peaked in early 2017. In the third quarter, only 146.3 million square feet was under construction nationally.

“It’s encouraging to see that office demand is broad-based across multiple sectors, with the technology and coworking sectors driving demand as we move later in the cycle,” said Michael Soto, Research Manager in Los Angeles. “If demand continues unabated, rental rate growth should moderate.”

Year-over-year, Minneapolis, San Antonio, and Charlotte, North Carolina, have experienced the most dramatic rent growth, all coming in at 10% or greater. The strong performance of secondary markets demonstrates that the office sector is not being propped up by a few formidable markets.

Download the national office market report at: http://twurls.com/3q18-us-

Related Stories

| Jun 5, 2023

Communication is the key to AEC firms’ mental health programs and training

The core of recent awareness efforts—and their greatest challenge—is getting workers to come forward and share stories.

Contractors | May 24, 2023

The average U.S. contractor has 8.9 months worth of construction work in the pipeline, as of April 2023

Contractor backlogs climbed slightly in April, from a seven-month low the previous month, according to Associated Builders and Contractors.

Multifamily Housing | May 23, 2023

One out of three office buildings in largest U.S. cities are suitable for residential conversion

Roughly one in three office buildings in the largest U.S. cities are well suited to be converted to multifamily residential properties, according to a study by global real estate firm Avison Young. Some 6,206 buildings across 10 U.S. cities present viable opportunities for conversion to residential use.

Industry Research | May 22, 2023

2023 High Growth Study shares tips for finding success in uncertain times

Lee Frederiksen, Managing Partner, Hinge, reveals key takeaways from the firm's recent High Growth study.

Multifamily Housing | May 8, 2023

The average multifamily rent was $1,709 in April 2023, up for the second straight month

Despite economic headwinds, the multifamily housing market continues to demonstrate resilience, according to a new Yardi Matrix report.

Market Data | May 2, 2023

Nonresidential construction spending up 0.7% in March 2023 versus previous month

National nonresidential construction spending increased by 0.7% in March, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau. On a seasonally adjusted annualized basis, nonresidential spending totaled $997.1 billion for the month.

Hotel Facilities | May 2, 2023

U.S. hotel construction up 9% in the first quarter of 2023, led by Marriott and Hilton

In the latest United States Construction Pipeline Trend Report from Lodging Econometrics (LE), analysts report that construction pipeline projects in the U.S. continue to increase, standing at 5,545 projects/658,207 rooms at the close of Q1 2023. Up 9% by both projects and rooms year-over-year (YOY); project totals at Q1 ‘23 are just 338 projects, or 5.7%, behind the all-time high of 5,883 projects recorded in Q2 2008.

Market Data | May 1, 2023

AEC firm proposal activity rebounds in the first quarter of 2023: PSMJ report

Proposal activity for architecture, engineering and construction (A/E/C) firms increased significantly in the 1st Quarter of 2023, according to PSMJ’s Quarterly Market Forecast (QMF) survey. The predictive measure of the industry’s health rebounded to a net plus/minus index (NPMI) of 32.8 in the first three months of the year.

Industry Research | Apr 25, 2023

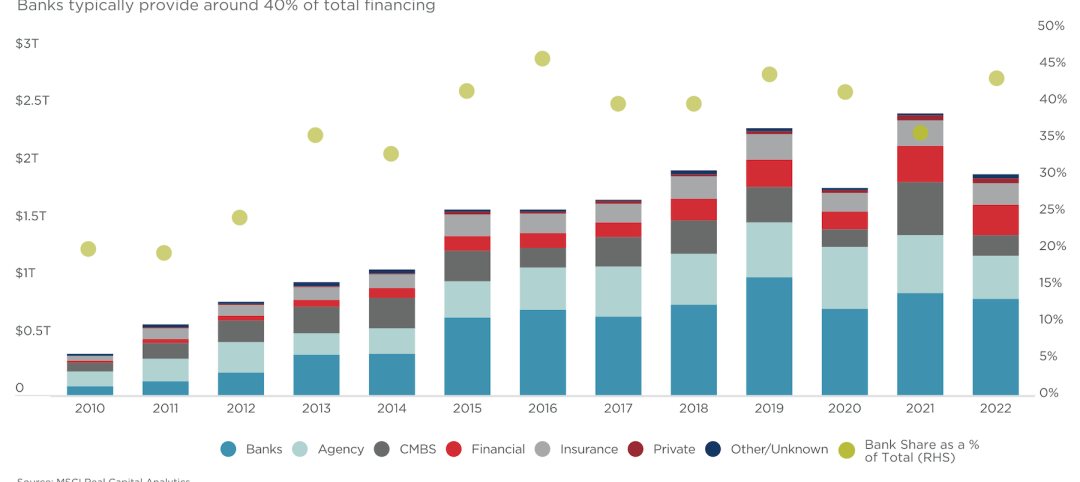

The commercial real estate sector shouldn’t panic (yet) about recent bank failures

A new Cushman & Wakefield report depicts a “well capitalized” banking industry that is responding assertively to isolated weaknesses, but is also tightening its lending.

Architects | Apr 21, 2023

Architecture billings improve slightly in March

Architecture firms reported a modest increase in March billings. This positive news was tempered by a slight decrease in new design contracts according to a new report released today from The American Institute of Architects (AIA). March was the first time since last September in which billings improved.