As seen in the Lodging Econometrics (LE) Q4'21 United States Construction Pipeline Trend Report, the franchise companies with the largest U.S. construction pipelines at year-end 2021 are Marriott International with 1,345 projects/170,586 rooms, followed by Hilton Worldwide with 1,239 projects/141,053 rooms, and InterContinental Hotels Group (IHG) with 761 projects/76,987 rooms. These three companies combined account for 69% of the projects and 67% of the rooms in the total U.S. construction pipeline.

At the end of Q4'21, over 56% of Hilton’s projects in the pipeline are in the early planning project stage, a record-high by projects in this stage for the company, with 689 projects/76,058 rooms. Hilton has 228 projects/29,036 under construction at Q4 and 322 projects/35,959 rooms scheduled to start within the next 12 months. Marriott also hit a record high for both projects and rooms in early planning at the end of the fourth quarter, with 534 projects/63,120 rooms. Marriott has 262 projects, accounting for 38,289 rooms under construction at the end of Q4 and 549 projects/69,177 rooms are scheduled to start in the next 12 months. IHG currently has 121 projects, accounting for 11,376 rooms, in the early planning stage. 136 projects, with 16,221 rooms, in IHG’s pipeline, are in the under construction stage while 504 projects/49,390 rooms are scheduled to start within the next 12 months.

The leading brands by project count for the top three franchise companies continue to be Hilton’s Home2 Suites by Hilton with 421 projects/43,824 rooms, IHG’s Holiday Inn Express with 288 projects/27,620 rooms, and Marriott’s Fairfield Inn with 247 projects/23,344 rooms. These three brands dominate the pipeline and combined claim 20% of the projects.

Other notable brands in the pipeline for the top franchise companies at Q4 are Marriott’s TownePlace Suites with 239 projects/22,759 rooms and Residence Inn with 212 projects/25,896 rooms; Hilton’s Tru by Hilton brand with 222 projects/21,222 rooms and the Hampton by Hilton brand with 267 projects/27,577 rooms; and IHG’s Avid Hotel with 148 projects/12,885 rooms and Staybridge Suites with 124 projects/12,734 rooms.

Through year-end 2021, Marriott, Hilton, and IHG branded hotels represented 585 new hotel openings with 73,415 rooms. 201 of the hotels were Hilton brands, 267 were Marriott brands, and another 117 were IHG brands. The LE forecast for new hotel openings in 2022 anticipates that Marriott will open 207 projects/27,258 rooms, for a growth rate of 3.1%. Next is Hilton with 165 projects/18,764 rooms, for a growth rate of 2.5%, followed by IHG with 115 projects/12,397 rooms forecast to open for a growth rate of 2.9%. In 2023, Marriot is expected to open another 211 projects/25,056 rooms for a growth rate of 2.7%. LE predicts Hilton will open 173 projects/21,450 rooms, for a 2.8% growth rate by year-end 2023, while IHG is expected to see a 3.4% growth rate in 2023, with 148 new hotel projects, accounting for 15,146 rooms.

Related Stories

Industry Research | Apr 28, 2017

A/E Industry lacks planning, but still spending large on hiring

The average 200-person A/E Firm is spending $200,000 on hiring, and not budgeting at all.

Market Data | Apr 19, 2017

Architecture Billings Index continues to strengthen

Balanced growth results in billings gains in all regions.

Market Data | Apr 13, 2017

2016’s top 10 states for commercial development

Three new states creep into the top 10 while first and second place remain unchanged.

Market Data | Apr 6, 2017

Architecture marketing: 5 tools to measure success

We’ve identified five architecture marketing tools that will help your firm evaluate if it’s on the track to more leads, higher growth, and broader brand visibility.

Market Data | Apr 3, 2017

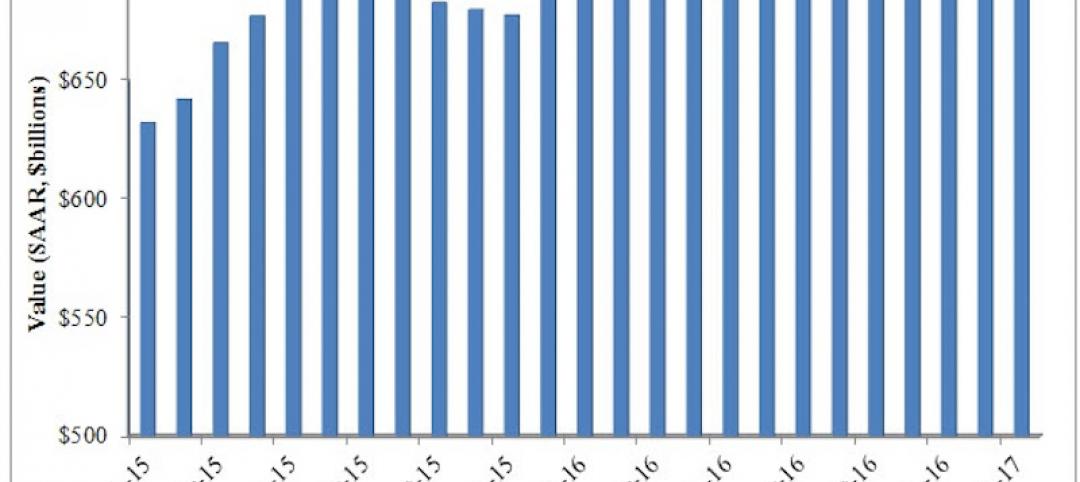

Public nonresidential construction spending rebounds; overall spending unchanged in February

The segment totaled $701.9 billion on a seasonally adjusted annualized rate for the month, marking the seventh consecutive month in which nonresidential spending sat above the $700 billion threshold.

Market Data | Mar 29, 2017

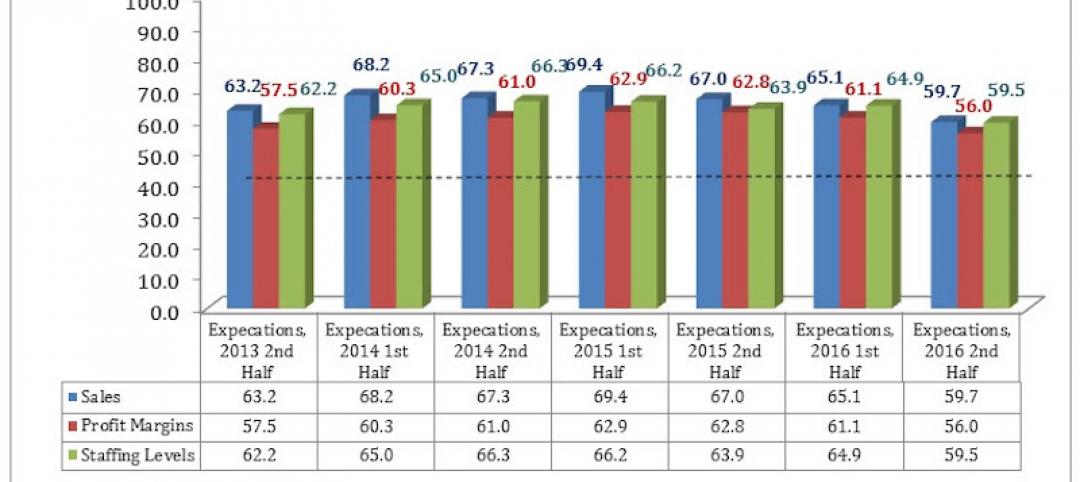

Contractor confidence ends 2016 down but still in positive territory

Although all three diffusion indices in the survey fell by more than five points they remain well above the threshold of 50, which signals that construction activity will continue to be one of the few significant drivers of economic growth.

Market Data | Mar 24, 2017

These are the most and least innovative states for 2017

Connecticut, Virginia, and Maryland are all in the top 10 most innovative states, but none of them were able to claim the number one spot.

Market Data | Mar 22, 2017

After a strong year, construction industry anxious about Washington’s proposed policy shifts

Impacts on labor and materials costs at issue, according to latest JLL report.

Market Data | Mar 22, 2017

Architecture Billings Index rebounds into positive territory

Business conditions projected to solidify moving into the spring and summer.

Market Data | Mar 15, 2017

ABC's Construction Backlog Indicator fell to end 2016

Contractors in each segment surveyed all saw lower backlog during the fourth quarter, with firms in the heavy industrial segment experiencing the largest drop.