As seen in the Lodging Econometrics (LE) Q4'21 United States Construction Pipeline Trend Report, the franchise companies with the largest U.S. construction pipelines at year-end 2021 are Marriott International with 1,345 projects/170,586 rooms, followed by Hilton Worldwide with 1,239 projects/141,053 rooms, and InterContinental Hotels Group (IHG) with 761 projects/76,987 rooms. These three companies combined account for 69% of the projects and 67% of the rooms in the total U.S. construction pipeline.

At the end of Q4'21, over 56% of Hilton’s projects in the pipeline are in the early planning project stage, a record-high by projects in this stage for the company, with 689 projects/76,058 rooms. Hilton has 228 projects/29,036 under construction at Q4 and 322 projects/35,959 rooms scheduled to start within the next 12 months. Marriott also hit a record high for both projects and rooms in early planning at the end of the fourth quarter, with 534 projects/63,120 rooms. Marriott has 262 projects, accounting for 38,289 rooms under construction at the end of Q4 and 549 projects/69,177 rooms are scheduled to start in the next 12 months. IHG currently has 121 projects, accounting for 11,376 rooms, in the early planning stage. 136 projects, with 16,221 rooms, in IHG’s pipeline, are in the under construction stage while 504 projects/49,390 rooms are scheduled to start within the next 12 months.

The leading brands by project count for the top three franchise companies continue to be Hilton’s Home2 Suites by Hilton with 421 projects/43,824 rooms, IHG’s Holiday Inn Express with 288 projects/27,620 rooms, and Marriott’s Fairfield Inn with 247 projects/23,344 rooms. These three brands dominate the pipeline and combined claim 20% of the projects.

Other notable brands in the pipeline for the top franchise companies at Q4 are Marriott’s TownePlace Suites with 239 projects/22,759 rooms and Residence Inn with 212 projects/25,896 rooms; Hilton’s Tru by Hilton brand with 222 projects/21,222 rooms and the Hampton by Hilton brand with 267 projects/27,577 rooms; and IHG’s Avid Hotel with 148 projects/12,885 rooms and Staybridge Suites with 124 projects/12,734 rooms.

Through year-end 2021, Marriott, Hilton, and IHG branded hotels represented 585 new hotel openings with 73,415 rooms. 201 of the hotels were Hilton brands, 267 were Marriott brands, and another 117 were IHG brands. The LE forecast for new hotel openings in 2022 anticipates that Marriott will open 207 projects/27,258 rooms, for a growth rate of 3.1%. Next is Hilton with 165 projects/18,764 rooms, for a growth rate of 2.5%, followed by IHG with 115 projects/12,397 rooms forecast to open for a growth rate of 2.9%. In 2023, Marriot is expected to open another 211 projects/25,056 rooms for a growth rate of 2.7%. LE predicts Hilton will open 173 projects/21,450 rooms, for a 2.8% growth rate by year-end 2023, while IHG is expected to see a 3.4% growth rate in 2023, with 148 new hotel projects, accounting for 15,146 rooms.

Related Stories

| Jun 5, 2023

Communication is the key to AEC firms’ mental health programs and training

The core of recent awareness efforts—and their greatest challenge—is getting workers to come forward and share stories.

Contractors | May 24, 2023

The average U.S. contractor has 8.9 months worth of construction work in the pipeline, as of April 2023

Contractor backlogs climbed slightly in April, from a seven-month low the previous month, according to Associated Builders and Contractors.

Multifamily Housing | May 23, 2023

One out of three office buildings in largest U.S. cities are suitable for residential conversion

Roughly one in three office buildings in the largest U.S. cities are well suited to be converted to multifamily residential properties, according to a study by global real estate firm Avison Young. Some 6,206 buildings across 10 U.S. cities present viable opportunities for conversion to residential use.

Industry Research | May 22, 2023

2023 High Growth Study shares tips for finding success in uncertain times

Lee Frederiksen, Managing Partner, Hinge, reveals key takeaways from the firm's recent High Growth study.

Multifamily Housing | May 8, 2023

The average multifamily rent was $1,709 in April 2023, up for the second straight month

Despite economic headwinds, the multifamily housing market continues to demonstrate resilience, according to a new Yardi Matrix report.

Market Data | May 2, 2023

Nonresidential construction spending up 0.7% in March 2023 versus previous month

National nonresidential construction spending increased by 0.7% in March, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau. On a seasonally adjusted annualized basis, nonresidential spending totaled $997.1 billion for the month.

Hotel Facilities | May 2, 2023

U.S. hotel construction up 9% in the first quarter of 2023, led by Marriott and Hilton

In the latest United States Construction Pipeline Trend Report from Lodging Econometrics (LE), analysts report that construction pipeline projects in the U.S. continue to increase, standing at 5,545 projects/658,207 rooms at the close of Q1 2023. Up 9% by both projects and rooms year-over-year (YOY); project totals at Q1 ‘23 are just 338 projects, or 5.7%, behind the all-time high of 5,883 projects recorded in Q2 2008.

Market Data | May 1, 2023

AEC firm proposal activity rebounds in the first quarter of 2023: PSMJ report

Proposal activity for architecture, engineering and construction (A/E/C) firms increased significantly in the 1st Quarter of 2023, according to PSMJ’s Quarterly Market Forecast (QMF) survey. The predictive measure of the industry’s health rebounded to a net plus/minus index (NPMI) of 32.8 in the first three months of the year.

Industry Research | Apr 25, 2023

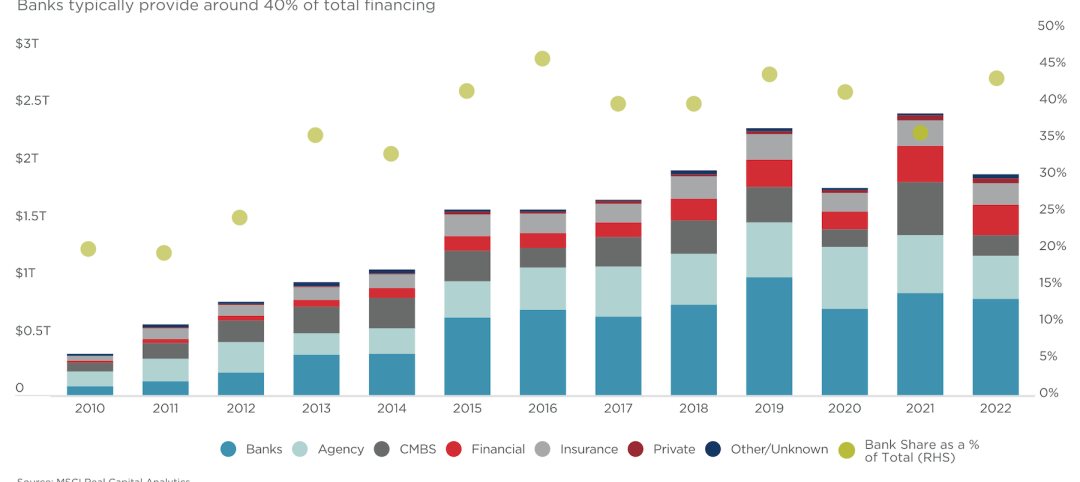

The commercial real estate sector shouldn’t panic (yet) about recent bank failures

A new Cushman & Wakefield report depicts a “well capitalized” banking industry that is responding assertively to isolated weaknesses, but is also tightening its lending.

Architects | Apr 21, 2023

Architecture billings improve slightly in March

Architecture firms reported a modest increase in March billings. This positive news was tempered by a slight decrease in new design contracts according to a new report released today from The American Institute of Architects (AIA). March was the first time since last September in which billings improved.