Construction costs are expected to increase by around 6 percent in 2021, and grow by another 4 to 7 percent in 2021, according to JLL’s Construction Cost Outlook for the second half of this year.

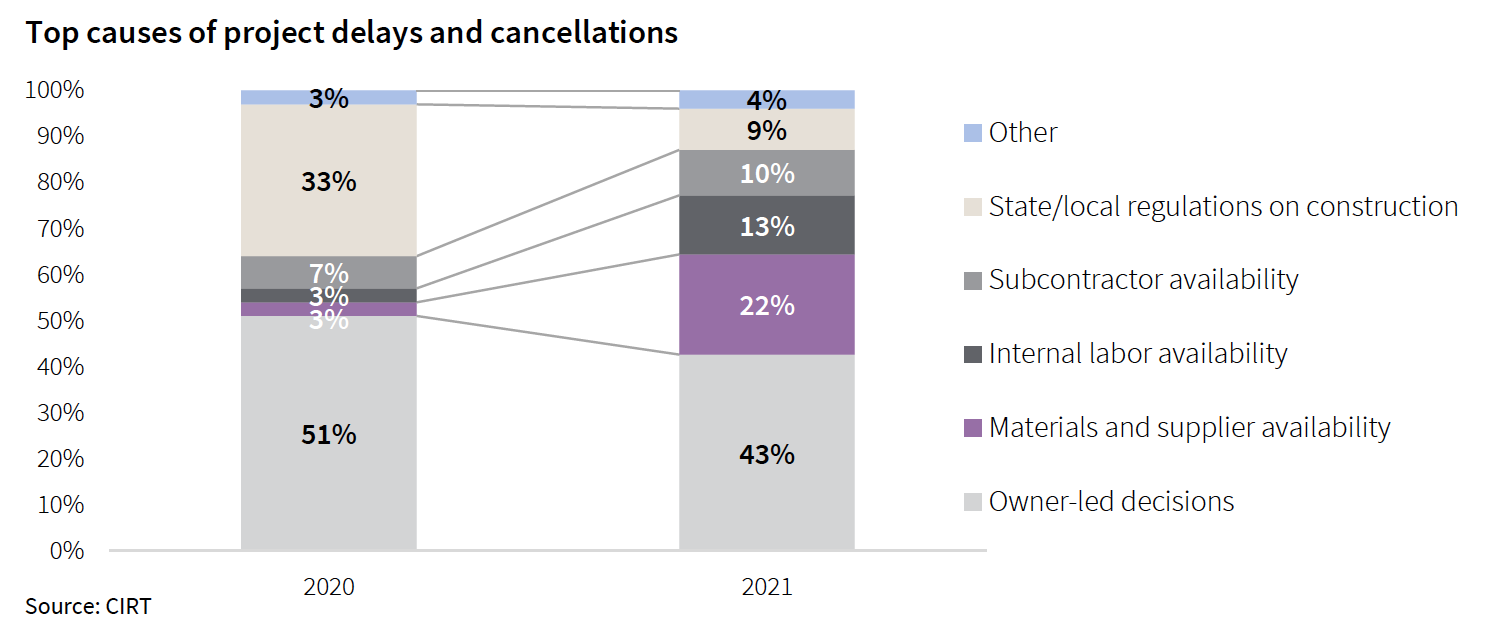

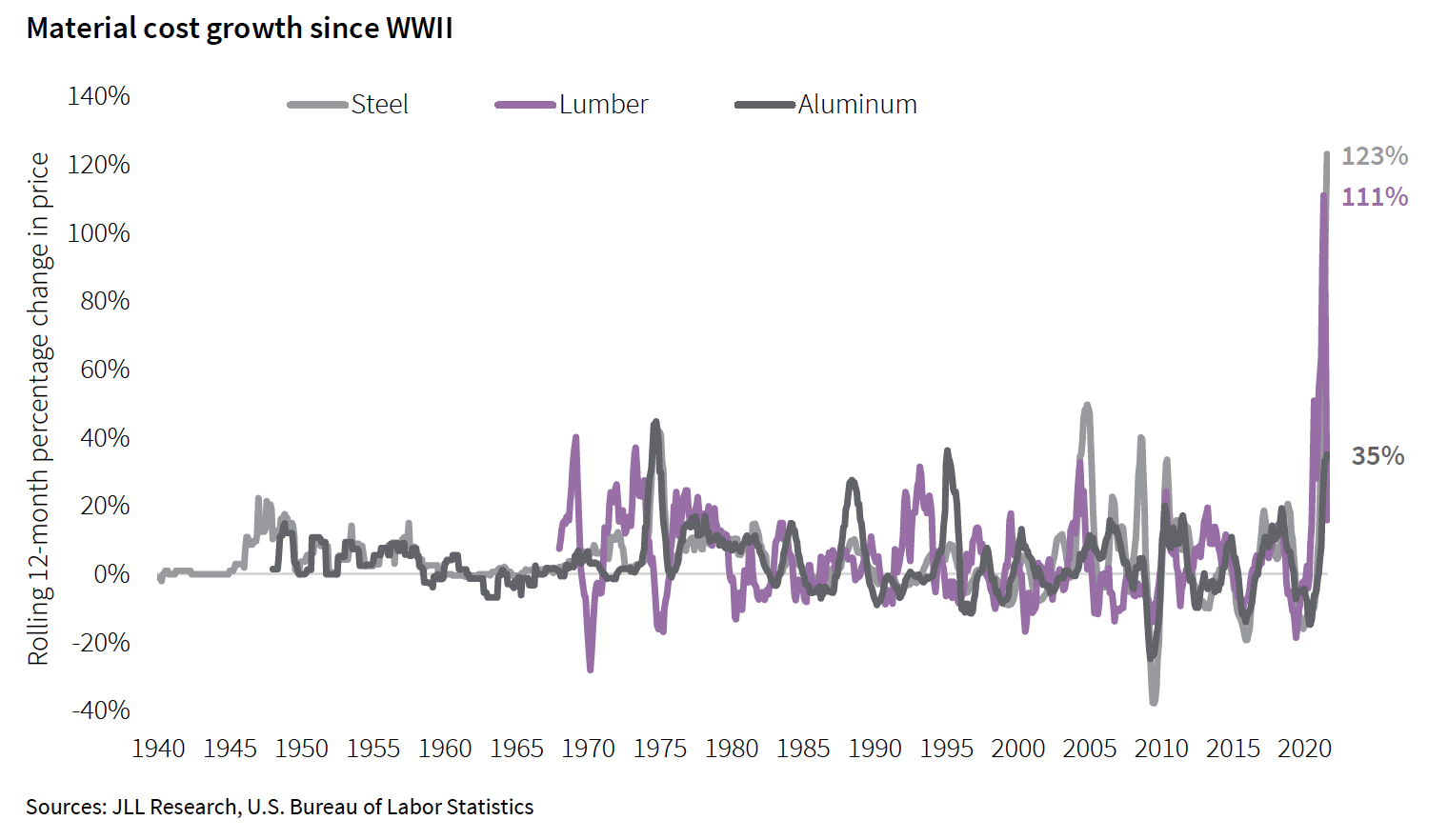

The Outlook tracks what has been “unprecedented” volatility in materials prices, which for the 12 months through August 2021 soared by 23 percent. Over that same period, labor costs rose by 4.46 percent, bringing total construction costs up by 4.51 percent. “The lack of available labor has led to more project delays so far in 2021 than a lack of materials, and conditions are expected to worsen over the coming year,” states Henry Esposito, JLL’s Construction Research Lead and the Outlook’s author.

Construction cost gains are occurring at a time when nonresidential construction spending was down by 9.5 percent for the 12 months through July 2021. JLL does not expect a “true” rebound in that spending until the Spring or Summer of next year. And don’t count on any immediate jolt from the federal infrastructure bill that, even if it passes, won’t impact construction spending or costs for two to six years out.

Construction recovery also faces two big immediate challenges:

Supply chain delays and record-high cost increases continue to put pressure on project execution and profitability. And the delta variant and future waves of the pandemic have the potential to slow economic growth, weakening the construction rebound “and calling into question some of the rosier predictions for 2022.” The Outlook states.

SHORTAGES AND DELAYS WILL CONTINUE THROUGH ‘22

As demand for new projects continues to grow and contractor backlogs fill, there will be less incentive to bid aggressively, and contractors will aim to pass through cost increases to owners as soon as the market can bear it. This combination of factors leads JLL to extend its forecasts for 4.5 to 7.5 percent final cost growth for nonresidential construction in calendar year 2021 and to predict a similar 4 to 7 percent cost growth range for 2022.

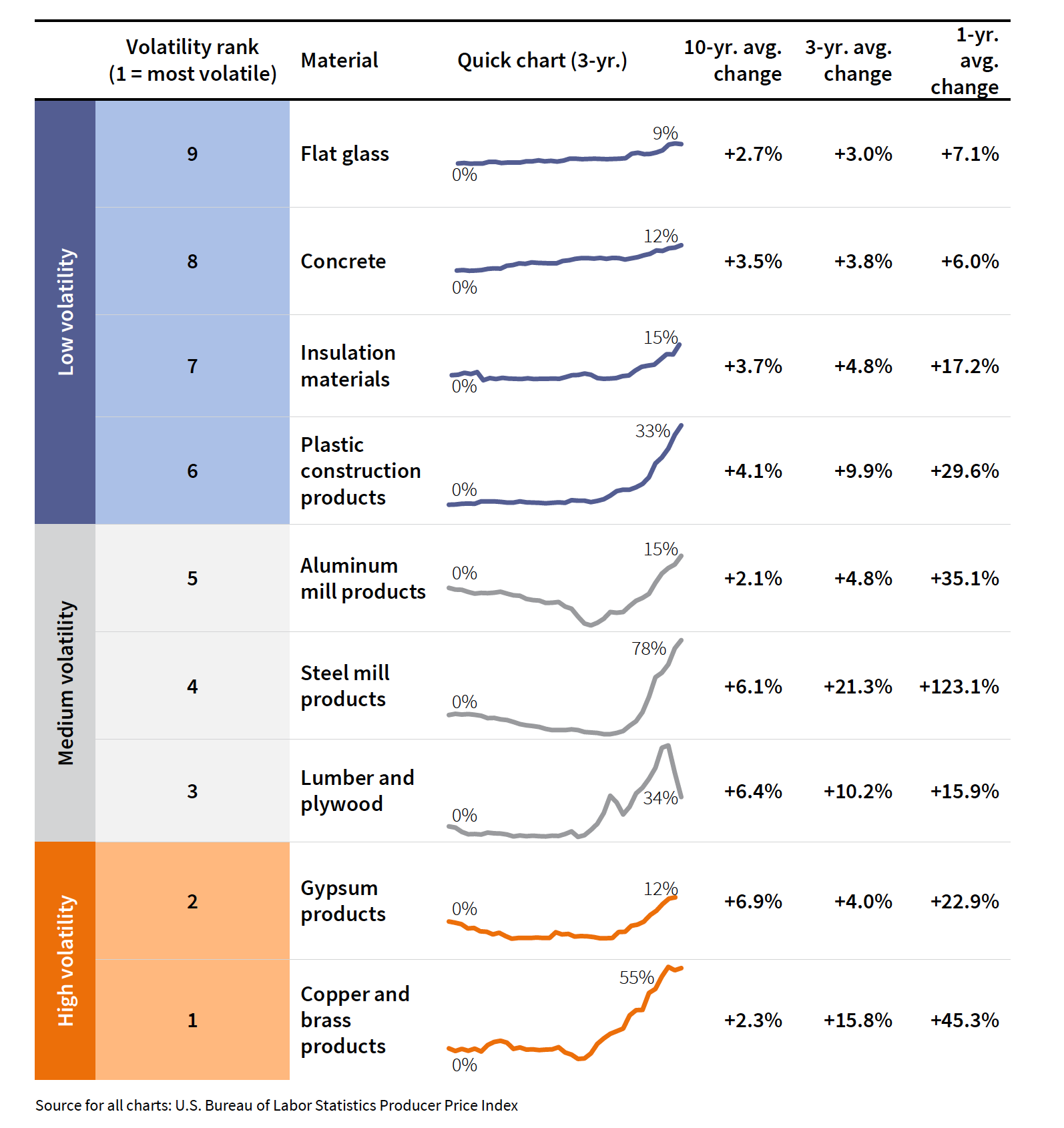

Some materials costs will ease, but the average increase will land somewhere between 5 and 11 percent. Aside from costs, the most pressing issues for most construction materials right now are lead times and delays. “Hopes for major relief during 2021 have been largely dashed, with hope for a return to normal now pushed out into 2022,” says JLL. The most pressing development might be the recent coup d’état in Guinea, which is one the world’s largest exporters of bauxite, the ore needed to produce aluminum.

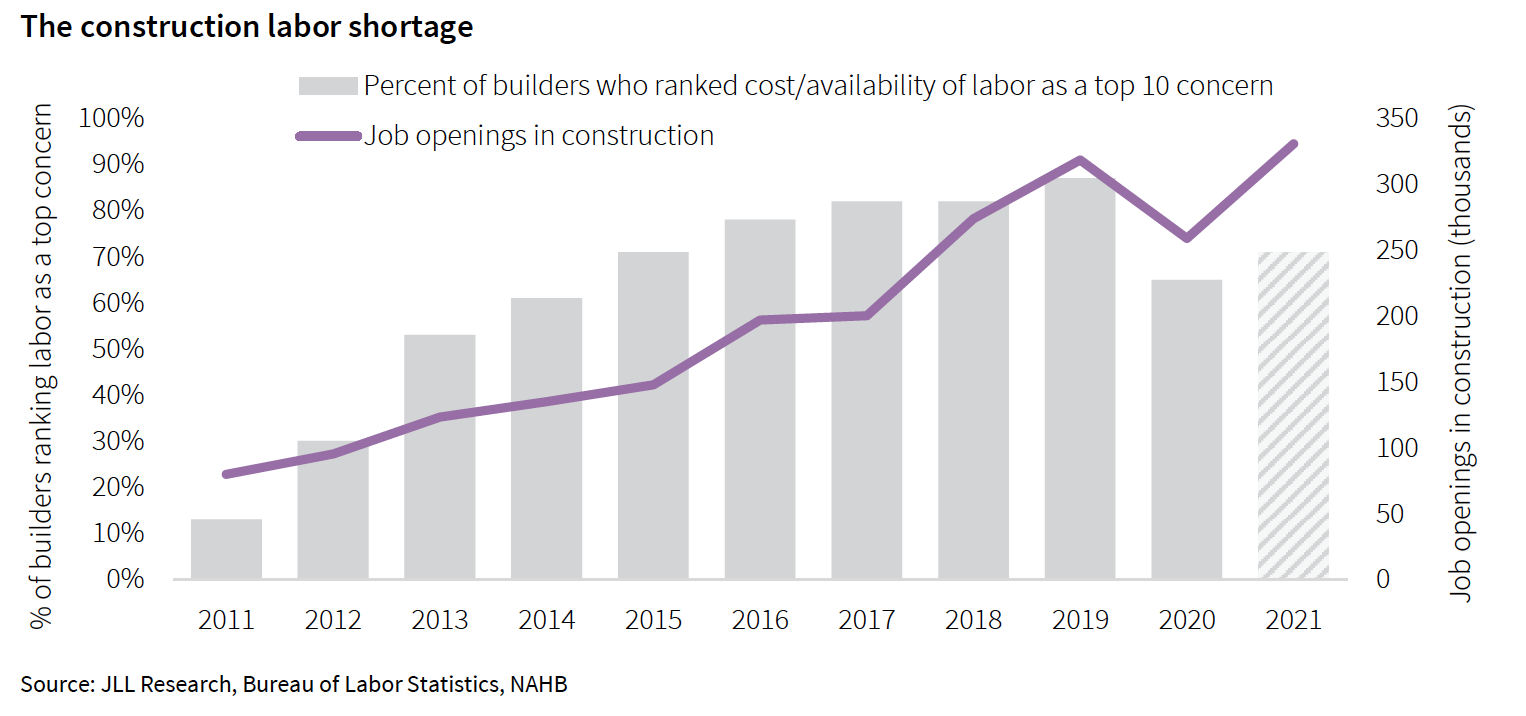

The industry’s labor shortage isn’t abating, either. From 2015 to 2019, the number of open and unfilled jobs in construction across the country doubled to 300,000. And while construction was one of the fastest sectors to recover from the pandemic, its workforce numbers still fall far short of demand, which is why JLL expects labor costs to grow in the 3 to 6 percent range. Construction also has the lowest vaccination rate, and the highest vaccine hesitancy rate, of any major industry, so jobsite workers remain more vulnerable to airborne infection that might sideline them.

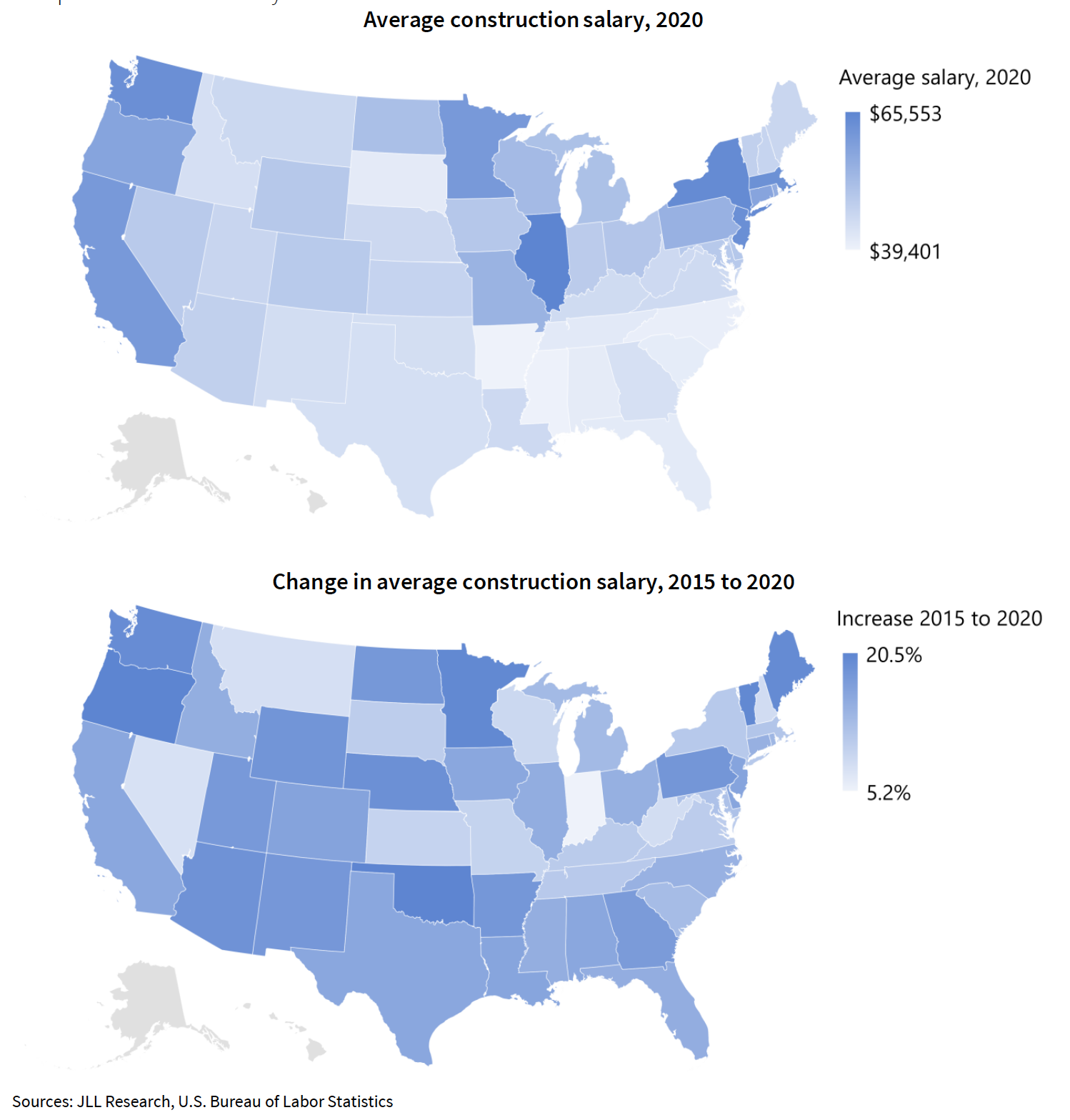

JLL shows that high-wage states are clustered in the Northeast corridor and the West Coast. The Midwest is also a high-cost region, with Illinois standing out as the top state, while the entire Southeast is the cheapest area of the country to hire workers. Wage growth across the country, on the other hand, is more evenly distributed, and some of the top states in total wages—such as Illinois, New York, and California—are only in the middle of the distribution pack.

Related Stories

Market Data | Nov 15, 2022

Construction demand will be a double-edged sword in 2023

Skanska’s latest forecast sees shorter lead times and receding inflation, but the industry isn’t out of the woods yet.

Reconstruction & Renovation | Nov 8, 2022

Renovation work outpaces new construction for first time in two decades

Renovations of older buildings in U.S. cities recently hit a record high as reflected in architecture firm billings, according to the American Institute of Architects (AIA).

Market Data | Nov 3, 2022

Building material prices have become the calm in America’s economic storm

Linesight’s latest quarterly report predicts stability (mostly) through the first half of 2023

Building Team | Nov 1, 2022

Nonresidential construction spending increases slightly in September, says ABC

National nonresidential construction spending was up by 0.5% in September, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau.

Hotel Facilities | Oct 31, 2022

These three hoteliers make up two-thirds of all new hotel development in the U.S.

With a combined 3,523 projects and 400,490 rooms in the pipeline, Marriott, Hilton, and InterContinental dominate the U.S. hotel construction sector.

Codes and Standards | Oct 26, 2022

‘Landmark study’ offers key recommendations for design-build delivery

The ACEC Research Institute and the University of Colorado Boulder released what the White House called a “landmark study” on the design-build delivery method.

Building Team | Oct 26, 2022

The U.S. hotel construction pipeline shows positive growth year-over-year at Q3 2022 close

According to the third quarter Construction Pipeline Trend Report for the United States from Lodging Econometrics (LE), the U.S. construction pipeline stands at 5,317 projects/629,489 rooms, up 10% by projects and 6% rooms Year-Over-Year (YOY).

Designers | Oct 19, 2022

Architecture Billings Index moderates but remains healthy

For the twentieth consecutive month architecture firms reported increasing demand for design services in September, according to a new report today from The American Institute of Architects (AIA).

Market Data | Oct 17, 2022

Calling all AEC professionals! BD+C editors need your expertise for our 2023 market forecast survey

The BD+C editorial team needs your help with an important research project. We are conducting research to understand the current state of the U.S. design and construction industry.

Market Data | Oct 14, 2022

ABC’s Construction Backlog Indicator Jumps in September; Contractor Confidence Remains Steady

Associated Builders and Contractors reports today that its Construction Backlog Indicator increased to 9.0 months in September, according to an ABC member survey conducted Sept. 20 to Oct. 5.