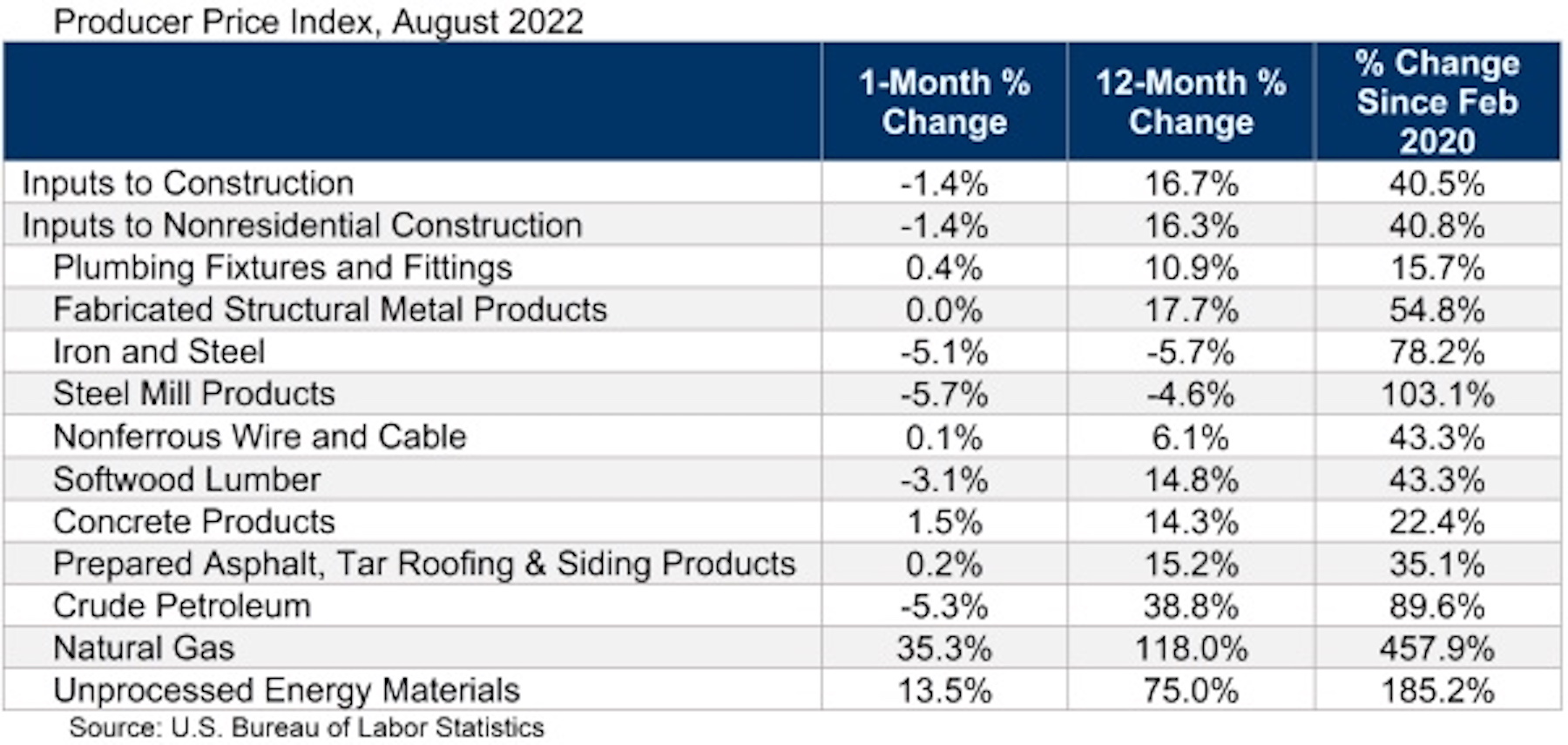

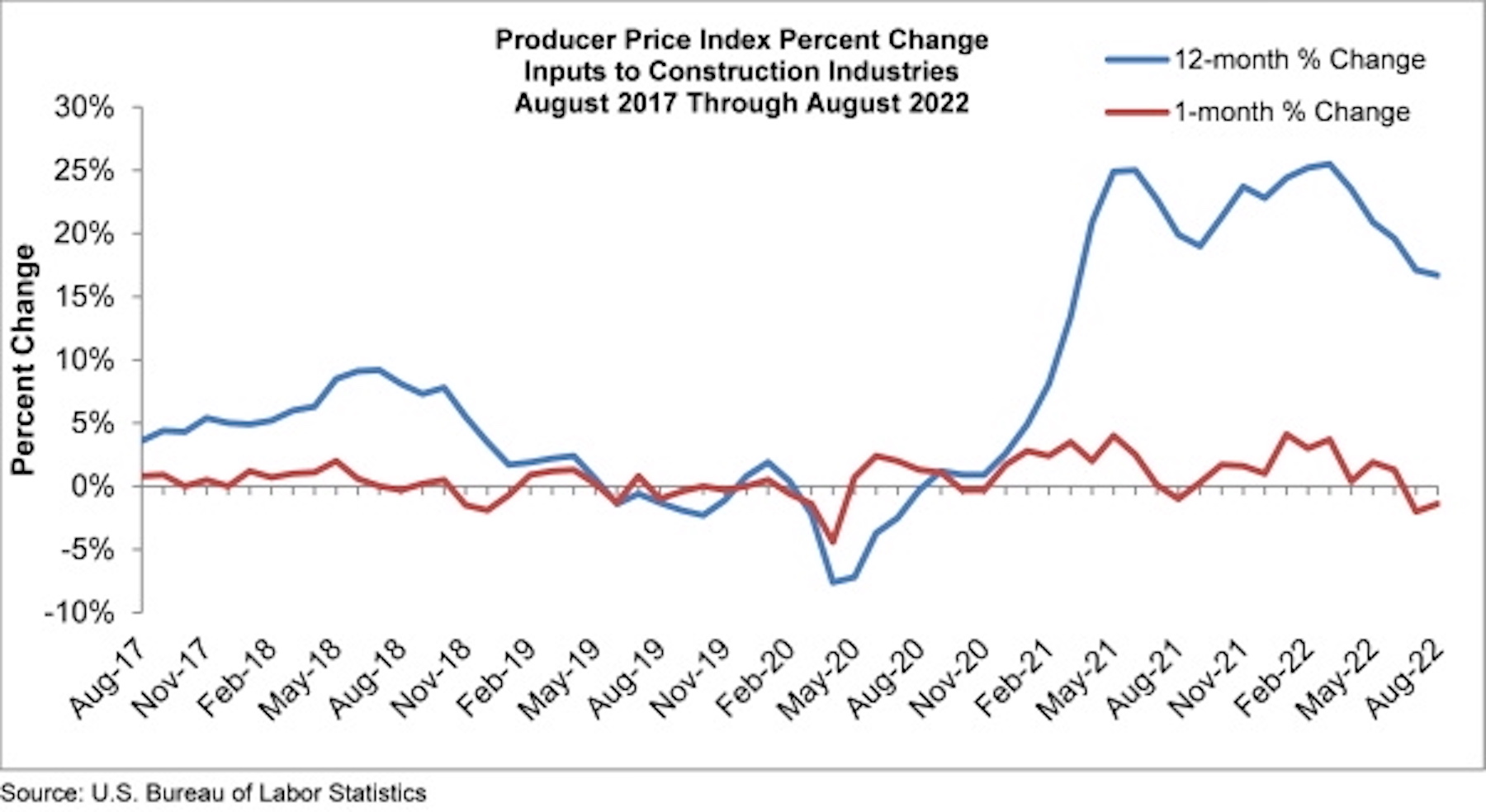

Construction input prices decreased 1.4% in August compared to the previous month, according to an Associated Builders and Contractors analysis of U.S. Bureau of Labor Statistics Producer Price Index data released today. Nonresidential construction input prices fell 1.4% for the month as well.

Construction input prices are up 16.7% from a year ago, while nonresidential construction input prices are 16.3% higher. Input prices were up in six of 11 subcategories* on a monthly basis. Natural gas prices increased 35.3% (and are 457.9% higher than they were in February 2020), followed by unprocessed energy materials prices, which rose 13.5%. Crude petroleum prices were down 5.3% in August.

"Until yesterday's Consumer Price Index report, investors and other market-watchers had been delighted by recent inflation news," said ABC Chief Economist Anirban Basu. "Today's Producer Price Index report supplies additional evidence that wholesale inflation is edging lower from the highs observed earlier this year. While this may create a sense of relief among contractors, this is no time for complacency.

"With COVID-19 lockdowns persisting in China, the world's leading manufacturer, and Europe facing severe energy crises, supply chain disruptions will persist," said Basu. "That suggests that construction materials and equipment prices are likely to remain elevated even if year-over-year price increases moderate. Public construction workers remain in short supply, including in the category of public construction. The upshot is that inflation is poised to remain stubbornly high even as some begin to declare victory. Estimators and others in the construction industry should be on guard for occasional surges in inflation during the months ahead."

Based on ABC's Construction Confidence Index and Backlog Indicator, many contractors expect to pass along their cost increases to project owners during the months ahead," said Basu. "Some contractors may be in for a rude surprise. With borrowing costs rising and risk of recession elevated, it is perfectly conceivable that project owners will become increasingly resistant to elevated charges for the delivery of construction services. Based on nonresidential construction spending data, that process has already begun. Accordingly, contractors should remain laser-focused on cashflow and weeding out costs as opportunities arise."

Related Stories

Contractors | Feb 13, 2024

The average U.S. contractor has 8.4 months worth of construction work in the pipeline, as of January 2024

Associated Builders and Contractors reported today that its Construction Backlog Indicator declined to 8.4 months in January, according to an ABC member survey conducted from Jan. 22 to Feb. 4. The reading is down 0.6 months from January 2023.

Codes | Feb 9, 2024

Illinois releases stretch energy code for building construction

Illinois is the latest jurisdiction to release a stretch energy code that provides standards for communities to mandate more efficient building construction. St. Louis, Mo., and a few states, including California, Colorado, and Massachusetts, currently have stretch codes in place.

Giants 400 | Feb 8, 2024

Top 10 Telecommunications Building Construction Firms for 2023

AECOM, LeChase Construction Services, Robins & Morton, and Salas O'Brien top BD+C's ranking of the nation's largest telecommunications building general contractors and construction management (CM) firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report.

Construction Firms for 2023, Photo by Ben Allan on Unsplash")

Giants 400 | Feb 8, 2024

Top 20 Integrated Project Delivery (IPD) Construction Firms for 2023

Barton Malow, DPR Construction, Hensel Phelps, and Whiting-Turner top BD+C's ranking of the nation's largest integrated project delivery (IPD) construction firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Feb 8, 2024

Top 90 Design-Build Construction Firms for 2023

Hensel Phelps, Ryan Companies US, Gray Construction, Haskell, and Burns & McDonnell top BD+C's ranking of the nation's largest design-build construction firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Feb 8, 2024

Top 20 Public Library Construction Firms for 2023

Gilbane Building Company, Skanska USA, Manhattan Construction, McCownGordon Construction, and C.W. Driver Companies top BD+C's ranking of the nation's largest public library general contractors and construction management (CM) firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Feb 8, 2024

Top 30 Public Library Engineering Firms for 2023

KPFF Consulting Engineers, Tetra Tech High Performance Buildings Group, Thornton Tomasetti, WSP, and Dewberry top BD+C's ranking of the nation's largest public library engineering and engineering/architecture (EA) firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Feb 8, 2024

Top 35 Performing Arts Center and Concert Venue Construction Firms for 2023

The Whiting-Turner Contracting Company, Holder Construction, McCarthy Holdings, Clark Group, and Gilbane Building Company top BD+C's ranking of the nation's largest performing arts center and concert venue general contractors and construction management (CM) firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Feb 8, 2024

Top 40 Museum Construction Firms for 2023

Turner Construction, Clark Group, Bancroft Construction, STO Building Group, and Alberici-Flintco top BD+C's ranking of the nation's largest museum and gallery general contractors and construction management (CM) firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report.

Market Data | Feb 7, 2024

New download: BD+C's February 2024 Market Intelligence Report

Building Design+Construction's monthly Market Intelligence Report offers a snapshot of the health of the U.S. building construction industry, including the commercial, multifamily, institutional, and industrial building sectors. This report tracks the latest metrics related to construction spending, demand for design services, contractor backlogs, and material price trends.