More than 10 years after the end of the most severe financial crisis since the Great Depression, the U.S. economy is again making history by continuing its longest-ever expansion. Nevertheless, emerging weakness in business investment has been hinting at softening outlays, giving commercial and industrial construction contractors cause for concern, according to a mid-year economic outlook by Anirban Basu, chief economist of Associated Builders and Contractors.

“Given that every expansion in U.S. history has ended in recession, leaders of construction firms are rightly wondering when the record-setting expansion will end,” said Basu. “Looking at conditions on the ground, it likely won’t be in 2019, but 2020 could be problematic for the broader economy and 2021 for a significant number of contractors.”

Basu cites numerous vulnerabilities that could trigger a recession in 2020, including:

— Trade wars

— Softening corporate earnings

— Slowing job growth

— Elevated levels of household, corporate and government debt

— Election 2020

But there are plenty of reasons to remain optimistic. “For the most part, the economy has held up better than anticipated,” said Basu. “During the first quarter of 2019, gross domestic product expanded at a smart 3.1% annualized rate. The U.S. Bureau of Economic Analysis’ initial estimate suggests that the economy slowed to 2.1% growth during the second quarter, but that neatly beat economists’ expectation that that growth had fallen below 2%.”

“The economy could continue to prove resilient,” says Basu. “To date, the economy has navigated ongoing trade disputes and associated tariffs with aplomb. It has also withstood serial interest rate hikes, the longest federal government shutdown in history, extreme weather, shifting immigration policy, ongoing labor market shortages and a lengthy investigation regarding foreign influence in U.S. elections.”

To read the full economic outlook story, visit ConstructionExec.com.

Related Stories

Market Data | Nov 22, 2021

Only 16 states and D.C. added construction jobs since the pandemic began

Texas, Wyoming have worst job losses since February 2020, while Utah, South Dakota add the most.

Market Data | Nov 10, 2021

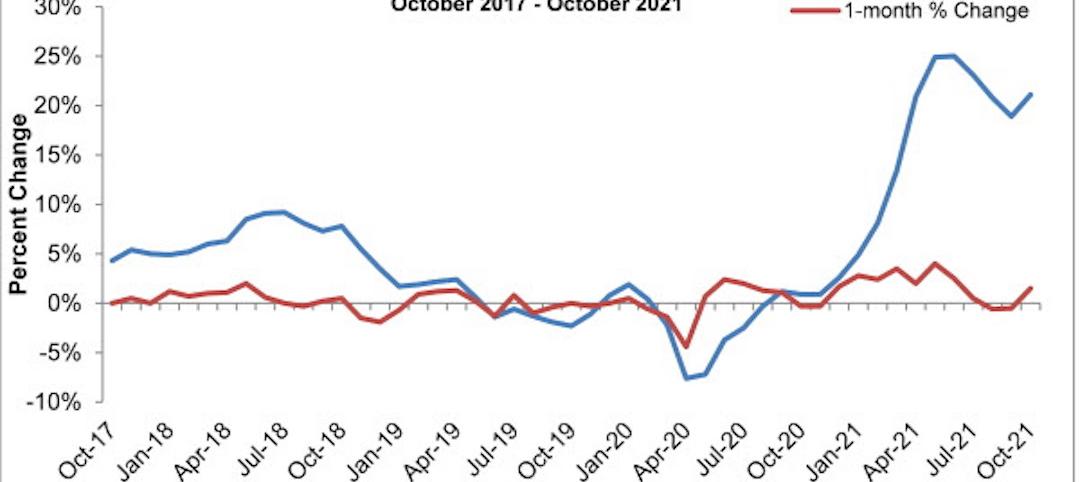

Construction input prices see largest monthly increase since June

Construction input prices are 21.1% higher than in October 2020.

Market Data | Nov 9, 2021

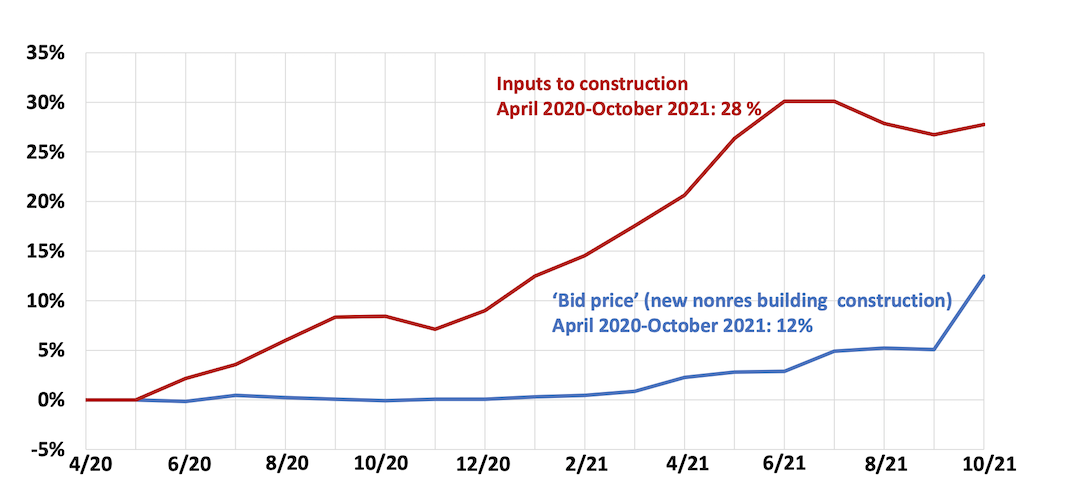

Continued increases in construction materials prices starting to drive up price of construction projects

Supply chain and labor woes continue.

Market Data | Nov 5, 2021

Construction firms add 44,000 jobs in October

Gain occurs even as firms struggle with supply chain challenges.

Market Data | Nov 3, 2021

One-fifth of metro areas lost construction jobs between September 2020 and 2021

Beaumont-Port Arthur, Texas and Sacramento--Roseville--Arden-Arcade Calif. top lists of gainers.

Market Data | Nov 2, 2021

Construction spending slumps in September

A drop in residential work projects adds to ongoing downturn in private and public nonresidential.

Hotel Facilities | Oct 28, 2021

Marriott leads with the largest U.S. hotel construction pipeline at Q3 2021 close

In the third quarter alone, Marriott opened 60 new hotels/7,882 rooms accounting for 30% of all new hotel rooms that opened in the U.S.

Hotel Facilities | Oct 28, 2021

At the end of Q3 2021, Dallas tops the U.S. hotel construction pipeline

The top 25 U.S. markets account for 33% of all pipeline projects and 37% of all rooms in the U.S. hotel construction pipeline.

Market Data | Oct 27, 2021

Only 14 states and D.C. added construction jobs since the pandemic began

Supply problems, lack of infrastructure bill undermine recovery.

Market Data | Oct 26, 2021

U.S. construction pipeline experiences highs and lows in the third quarter

Renovation and conversion pipeline activity remains steady at the end of Q3 ‘21, with conversion projects hitting a cyclical peak, and ending the quarter at 752 projects/79,024 rooms.