Prices of construction materials jumped more than 20% from January 2021 to January 2022, according to an analysis by the Associated General Contractors of America of government data released today. The association recently posted a new edition of its Construction Inflation Alert, a report to inform project owners, officials, and others about the challenges volatile materials costs, supply chain disruptions, and labor shortages posed for construction firms.\

“Unfortunately, there has been no letup early this year in the extreme cost runup that contractors endured in 2021,” said Ken Simonson, the association’s chief economist. “They are apparently passing on more of those costs but will have a continuing challenge in getting timely deliveries and finding enough workers.”

The producer price index for inputs to new nonresidential construction—the prices charged by goods producers and service providers such as distributors and transportation firms—increased by 2.6% from December to January and 20.3% over the past 12 months. In comparison, the index for new nonresidential construction—a measure of what contractors say they would charge to erect five types of nonresidential buildings—climbed by 3.8% for the month and 16.5% from a year earlier.

A wide range of inputs contributed to the more than 20% jump in the cost index, Simonson noted. The price index for steel mill products soared 112.7% over 12 months despite declining 1.6% in January. The index for plastic construction products climbed 1.8% for the month and 35.0% over 12 months. The index for diesel fuel jumped 5.1% in January and 56.5% for the year. The index for aluminum mill shapes jumped 5.6% in January and 32.7% over 12 months, while the index for copper and brass mill shapes rose 4.1% in January and 24.8% over the year. Architectural coatings such as paint had an unusually large price gain of 9.0% in January and 24.3% over 12 months. The index for lumber and plywood leaped 15.4 for the month and 21.1% year-over-year. Other inputs with double-digit increases for the past 12 months include insulation, 19.2%; trucking, 18.3%; and construction machinery and equipment, 11.4%.

Association officials said construction firms are being squeezed by increases costs for materials and labor shortages. They urged federal officials to take additional steps to address supply chain disruptions and rising materials prices. These include continuing to remove costly tariffs on key construction components.

“Spiking materials prices are making it challenging for most firms to profit from any increases in demand for new construction projects,” said Stephen E. Sandherr, the association’s chief executive officer. “Left unabated, these price increases will undermine the economic case for many development projects and limit the positive impacts of the new infrastructure bill.”

View producer price index data. View chart of gap between input costs and bid prices. View the February 2022 Construction Inflation Alert.

Related Stories

Market Data | Mar 29, 2017

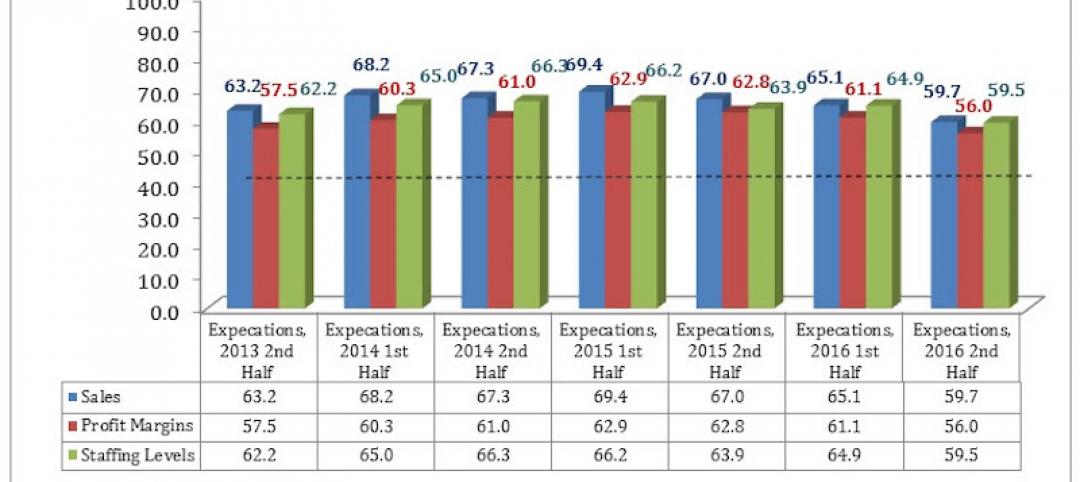

Contractor confidence ends 2016 down but still in positive territory

Although all three diffusion indices in the survey fell by more than five points they remain well above the threshold of 50, which signals that construction activity will continue to be one of the few significant drivers of economic growth.

Market Data | Mar 24, 2017

These are the most and least innovative states for 2017

Connecticut, Virginia, and Maryland are all in the top 10 most innovative states, but none of them were able to claim the number one spot.

Market Data | Mar 22, 2017

After a strong year, construction industry anxious about Washington’s proposed policy shifts

Impacts on labor and materials costs at issue, according to latest JLL report.

Market Data | Mar 22, 2017

Architecture Billings Index rebounds into positive territory

Business conditions projected to solidify moving into the spring and summer.

Market Data | Mar 15, 2017

ABC's Construction Backlog Indicator fell to end 2016

Contractors in each segment surveyed all saw lower backlog during the fourth quarter, with firms in the heavy industrial segment experiencing the largest drop.

Market Data | Feb 28, 2017

Leopardo’s 2017 Construction Economics Report shows year-over-year construction spending increase of 4.2%

The pace of growth was slower than in 2015, however.

Market Data | Feb 23, 2017

Entering 2017, architecture billings slip modestly

Despite minor slowdown in overall billings, commercial/ industrial and institutional sectors post strongest gains in over 12 months.

Market Data | Feb 16, 2017

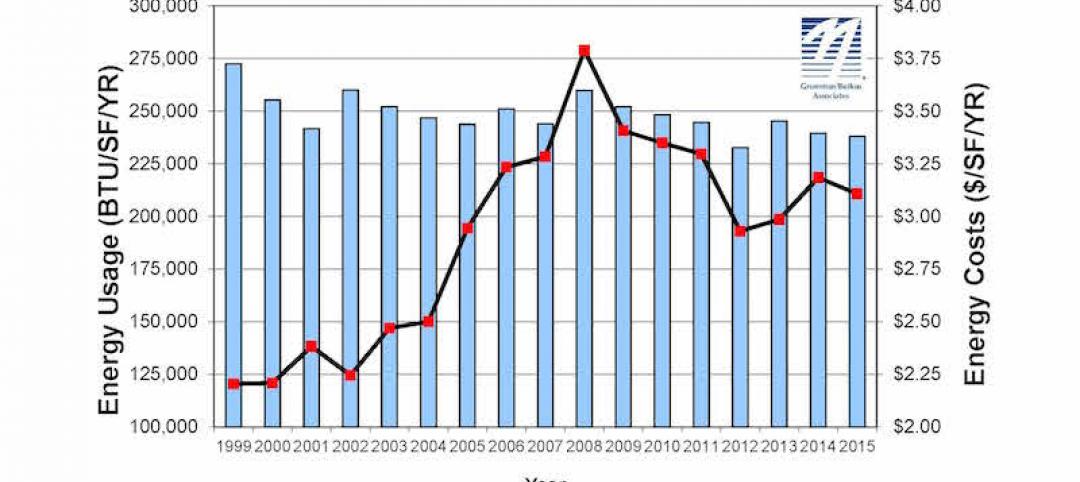

How does your hospital stack up? Grumman/Butkus Associates 2016 Hospital Benchmarking Survey

Report examines electricity, fossil fuel, water/sewer, and carbon footprint.

Market Data | Feb 1, 2017

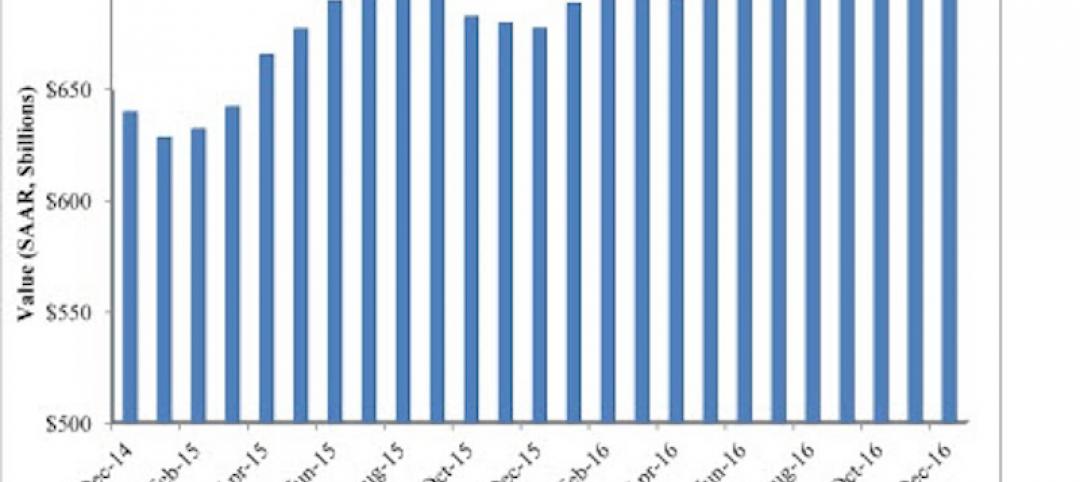

Nonresidential spending falters slightly to end 2016

Nonresidential spending decreased from $713.1 billion in November to $708.2 billion in December.

Market Data | Jan 31, 2017

AIA foresees nonres building spending increasing, but at a slower pace than in 2016

Expects another double-digit growth year for office construction, but a more modest uptick for health-related building.