Nonresidential building is on track to achieve a “breakout year” in 2015, during which spending growth could exceed 20%, according to projections by construction giant Gilbane in its Summer 2015 Construction Economics Report, “Building for the Future.”

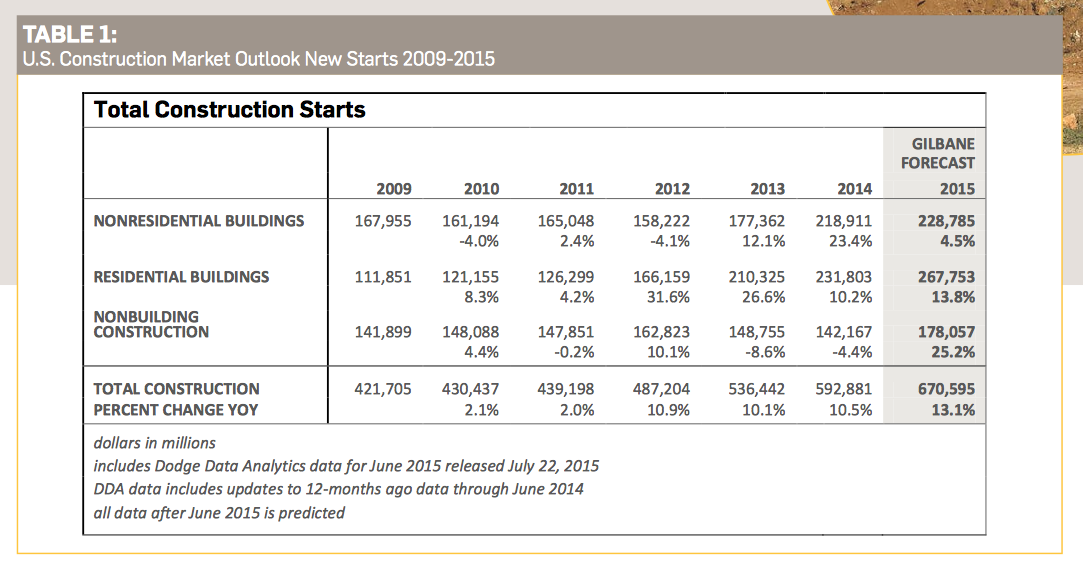

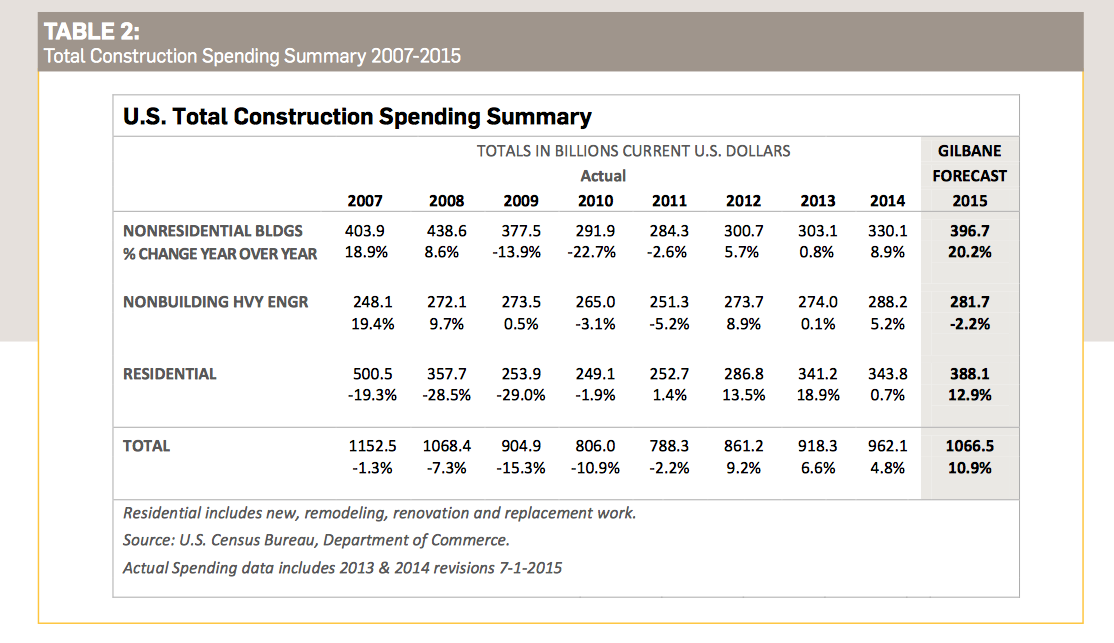

Through the first six months of the year, construction spending for residential, nonresidential building, and nonbuilding structures was increasing at the fastest pace since 2004-2005. On that basis, Gilbane expects total construction spending to expand by 10.9% to $1.067 trillion this year (the second-highest growth total ever recorded), and by more than 8% in 2016. Construction starts are expected to be up by 13.1% to 670,595 units this year.

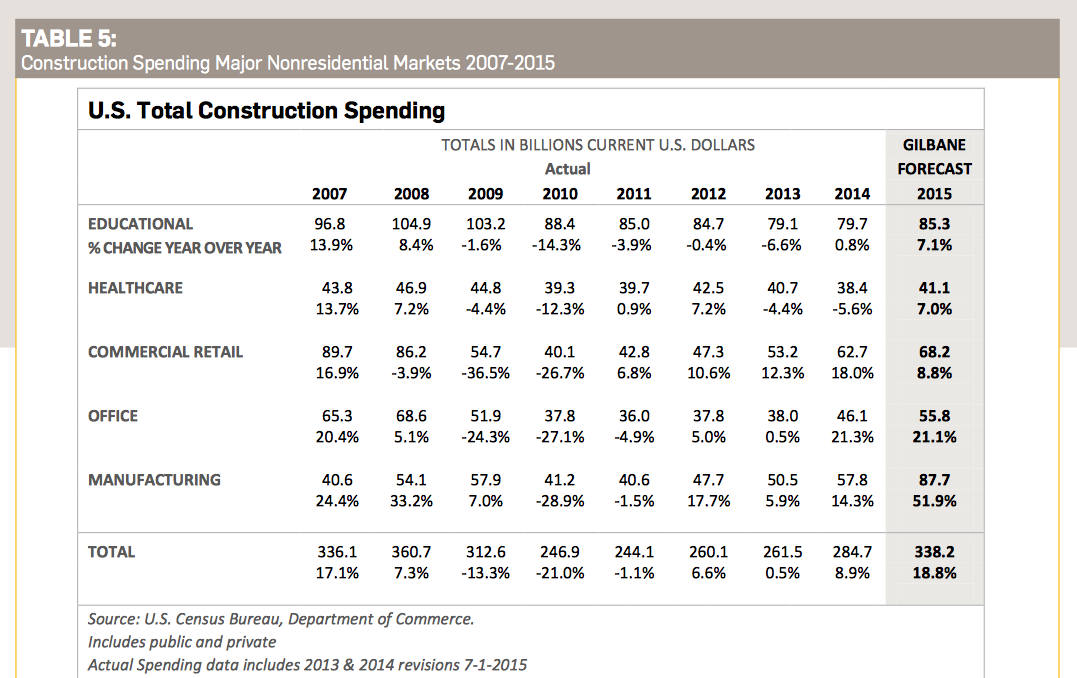

Nonresidential building starts, which hit a 10-year low in 2012, have been increasing at an average of 17% per year. Nonresidential buildings starts since March 2014 posted the best five quarters since the third quarter of 2008. Although growth should continue, expect it to do so at a more moderate rate, says Gilbane, which predicts those starts to increase this year by only 4.5% to 228,785 units. That construction activity, however, has been driving spending, which Gilbane predicts will increase by 20.2% to $396.7 billion this year. “Escalation will climb to levels typical of rapidly growing markets,” Gilbane observes.

But nonres building’s strengths vary markedly by sector:

- Total spending for manufacturing buildings in 2015 will reach $86.4 billion, up nearly 50% from 2014. No market sector has ever before recorded a 50% year-over-year increase, and manufacturing could replace perennial leader Education as nonres building’s biggest contributing sector. Gilbane foresees spending in this sector cooling off a bit next year to a still-strong 9% increase. Gilbane points out that the manufacturing sector, through the first half of 2015, accounted for 50% of total private construction spending, which is expected to increase this year by 14.5% to $781 billion.

- Spending for educational buildings in 2015 will total $85.3 billion, a 7.1% increase from 2014, the sector’s first substantial increase since 2008. After hitting a low in the fourth quarter of 2013 not seen since 2004, educational spending has rebounded steadily. Gilbane forecasts a 6% gain in 2016.

- Total spending for healthcare construction in 2015 should be up 7% to $41.1 billion. Healthcare spending is slowly recovering after descending to an eight-year low in the fourth quarter 2014. Spending is expected to rise by 6% in 2016.

- Spending for commercial/retail buildings—which was nonres’ strongest growth market in 2012 through 2014—is projected to jump by 8.8% to $68.2 billion this year. Gilbane notes that this sector. Commercial retail is expected to realize a gain of 5.4% in 2016.

- Office building spending in 2015 is on pace to grow by 21.2% to $55.8 billion this year, on top of a 21.3% increase in 2014. Office spending will maintain upward momentum in 2016 but at a slower pace, to 8.4%.

In its report, Gilbane discusses spending for residential construction, which it expects to grow this year by 12.9% to $388 billion, and then to taper off to a 0.7% increase in 2016. “In fact, from the fourth quarter of 2013 through March 2015, new housing starts practically stalled and the rate of residential spending declined,” Gilbane states.

Gilbane is skeptical—to say the least—about other forecasts that project housing starts to reach between 1.3 million and 1.5 million units this year, which would be twice to three times historical growth rates.

The Commerce Department’s estimates for July show housing starts rose by 0.2% to a seasonally adjusted annualized rate of 1.119 million units. Multifamily starts, which over the past few years have fueled housing’s growth, were off 17% to an annualized rate of 413,000 units.

In all construction sectors, the biggest potential constraint to growth continues to be the availability of labor. Gilbane notes that the number of unfilled positions on the Bureau of Labor Statistics’ Job Openings and Labor Turnover Survey for the construction industry has been over 100,000 for 26 of the 28 months through June 2015, and has been trending up since 2012.

“As work volume begins to increase over the next few years, expect productivity to decline,” Gilbane cautions.

Related Stories

Mass Timber | Apr 25, 2024

Bjarke Ingels Group designs a mass timber cube structure for the University of Kansas

Bjarke Ingels Group (BIG) and executive architect BNIM have unveiled their design for a new mass timber cube structure called the Makers’ KUbe for the University of Kansas School of Architecture & Design. A six-story, 50,000-sf building for learning and collaboration, the light-filled KUbe will house studio and teaching space, 3D-printing and robotic labs, and a ground-level cafe, all organized around a central core.

Senior Living Design | Apr 24, 2024

Nation's largest Passive House senior living facility completed in Portland, Ore.

Construction of Parkview, a high-rise expansion of a Continuing Care Retirement Community (CCRC) in Portland, Ore., completed recently. The senior living facility is touted as the largest Passive House structure on the West Coast, and the largest Passive House senior living building in the country.

Hotel Facilities | Apr 24, 2024

The U.S. hotel construction market sees record highs in the first quarter of 2024

As seen in the Q1 2024 U.S. Hotel Construction Pipeline Trend Report from Lodging Econometrics (LE), at the end of the first quarter, there are 6,065 projects with 702,990 rooms in the pipeline. This new all-time high represents a 9% year-over-year (YOY) increase in projects and a 7% YOY increase in rooms compared to last year.

ProConnect Events | Apr 23, 2024

5 more ProConnect events scheduled for 2024, including all-new 'AEC Giants'

SGC Horizon present 7 ProConnect events in 2024.

75 Top Building Products | Apr 22, 2024

Enter today! BD+C's 75 Top Building Products for 2024

BD+C editors are now accepting submissions for the annual 75 Top Building Products awards. The winners will be featured in the November/December 2024 issue of Building Design+Construction.

Resiliency | Apr 22, 2024

Controversy erupts in Florida over how homes are being rebuilt after Hurricane Ian

The Federal Emergency Management Agency recently sent a letter to officials in Lee County, Florida alleging that hundreds of homes were rebuilt in violation of the agency’s rules following Hurricane Ian. The letter provoked a sharp backlash as homeowners struggle to rebuild following the devastating 2022 storm that destroyed a large swath of the county.

Mass Timber | Apr 22, 2024

British Columbia changing building code to allow mass timber structures of up to 18 stories

The Canadian Province of British Columbia is updating its building code to expand the use of mass timber in building construction. The code will allow for encapsulated mass-timber construction (EMTC) buildings as tall as 18 stories for residential and office buildings, an increase from the previous 12-story limit.

Standards | Apr 22, 2024

Design guide offers details on rain loads and ponding on roofs

The American Institute of Steel Construction and the Steel Joist Institute recently released a comprehensive roof design guide addressing rain loads and ponding. Design Guide 40, Rain Loads and Ponding provides guidance for designing roof systems to avoid or resist water accumulation and any resulting instability.

Building Materials | Apr 22, 2024

Tacoma, Wash., investigating policy to reuse and recycle building materials

Tacoma, Wash., recently initiated a study to find ways to increase building material reuse through deconstruction and salvage. The city council unanimously voted to direct the city manager to investigate deconstruction options and estimate costs.

Student Housing | Apr 19, 2024

$115 million Cal State Long Beach student housing project will add 424 beds

A new $115 million project recently broke ground at California State University, Long Beach (CSULB) that will add housing for 424 students at below-market rates. The 108,000 sf La Playa Residence Hall, funded by the State of California’s Higher Education Student Housing Grant Program, will consist of three five-story structures connected by bridges.