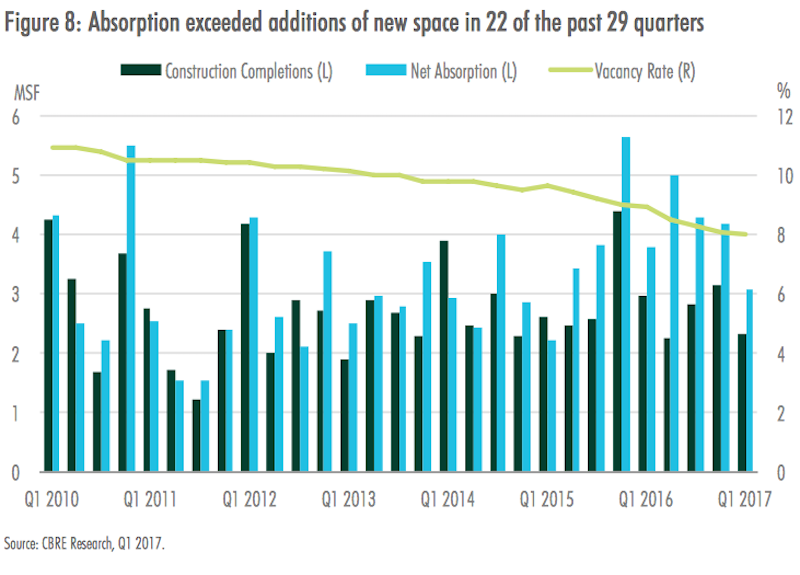

National construction of medical office buildings (MOBs) stood at 12.5 million sf in the first quarter of 2017, down slightly from a few years ago but still well above recession-era levels. However, construction continues to be outpaced by net absorptions, which between 2015 and Q1 2017 totaled 35.4 million sf, or 38% higher than completions over that same period.

In its first-ever report on U.S. Medical Office Buildings, CBRE notes that the vacancy rate for MOBs has “tightened steadily” since 2010, to its current level of 8%, a record low for this sector and well below the 13% vacancy rate for the U.S. office market.

To assess what’s driving MOB demand and development, CBRE took looked at Class A and B buildings with at least 10,000 sf of rentable area specifically designated as medical office space in 30 metros, with detailed investment and demographic profiles of each city.

It found a “resilient” MOB market that continues to benefit from several factors, not the least of which being the population growth of senior citizens. The U.S. Census Bureau estimates that the 65-plus population will nearly double between 2015 and 2055 to more than 92 million, and comprise nearly 23% of the country’s total population.

“The steep increase in both the 65+ population and anticipated greater need for in-office physician services by this group signal a continued increase in demand for health care services and medical office space in the decades ahead,” CBRE states.

Markets where the 65+ population is expected to grow strongest over the next five years include Las Vegas, Phoenix, Atlanta, Dallas-Fort Worth, Houston, and South Florida, according to Moody’s Analytics.

CBRE observes that providers are attempting to stem perennially increasing healthcare expenditures by moving more patient volume away from hospitals and toward more cost-effective outpatient facilities, such as MOBs and urgent-care centers.

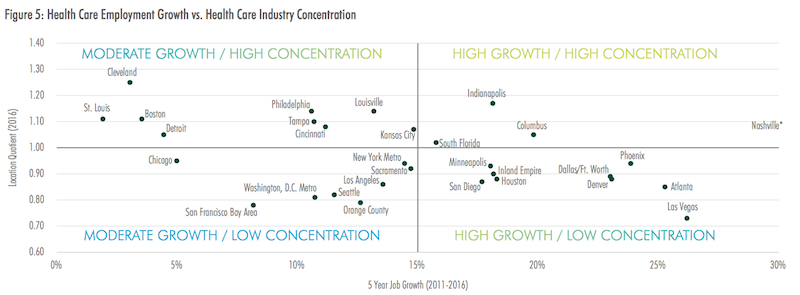

Health care jobs, particularly physicians, have been added at a much faster pace than jobs overall. Image: CBRE

Another cost-cutting trend that’s impacting healthcare real estate, says CBRE, has been the “significant uptick” in mergers and acquisitions. Consolidation among physician medical groups has been particularly strong, with deal volume surging by 19% in 2016 and 109% year-over-year in Q1 2017, according to PwC.

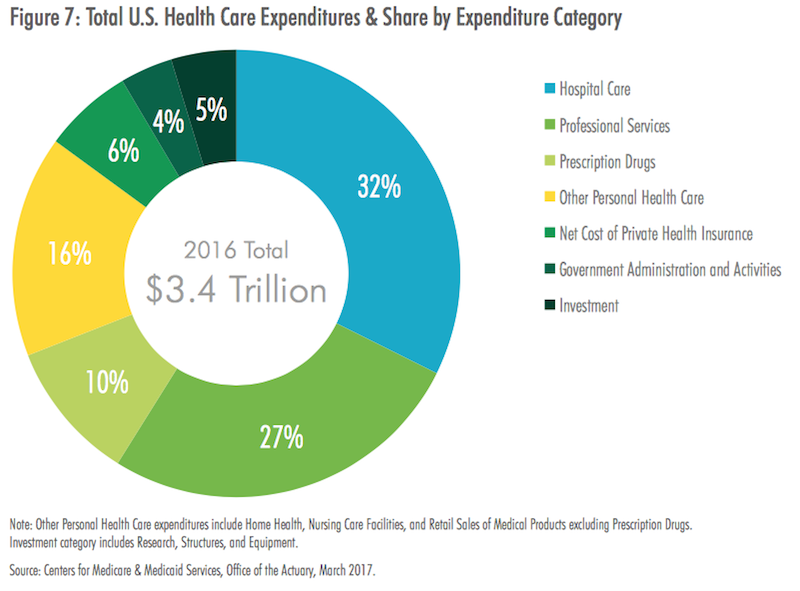

Outpatient professional services are not as expensive as hospital care, but they still accounted for nealry $900 billion in 2016. Image: CBRE.

Overall asking rents for medical office properties have remained relatively stable over the past seven years, ranging between $22 and $23 per sf per year. CBRE explains that the high cost of tenant build-outs, as well as the importance of proximity to a provider’s patient base and ancillary medical services, compel many tenants to remain in place for long periods of time.

But rent appreciation varies widely by market; average rents in New York, for example, grew by 83% since Q1 2010 to over $68 per sf in Q1 2017. Indeed, almost all of the 30 markets examined registered rent increases over the past year. And investors surveyed expect MOB rents to increase between 1% and 3% this year.

Low vacancy rates in this sector are attributed, in part, to the widening gap between completions and absorptions over the past three years.

On a yearly basis, net absorption has been increasing since 2011 when it totaled 8.1 million sf. Since then, annual absorption grew by 114% to 17.2 million sf in 2016. Four of the five markets with the most positive net absorption in 2016 were located in the South or West: Houston (436,300 sf) Tampa (413,800 sf) Phoenix (314,400 sf) and South Florida (310,703 sf). Indianapolis was the lone top market not located in the Sun Belt, ranking third with 383,700 sf of positive absorption.

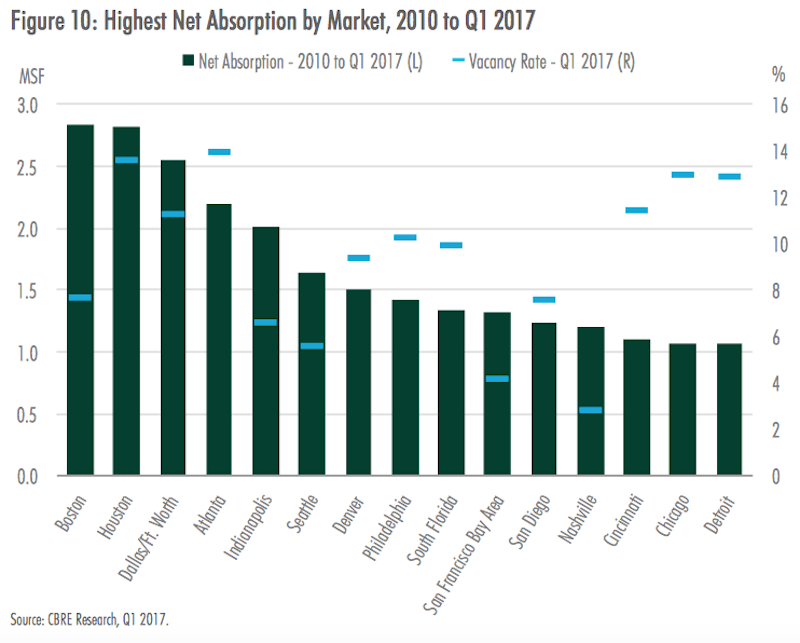

This chart compares cities' net absorptions of MOBs with their vacancy rates for that building type. Image: CBRE

New construction of MOBs is not keeping up with demand, based on net absorption rates for 30 large metros. Image: CBRE

CBRE found that as investors’ appetites for healthcare-related properties have increased, MOBs “have emerged as the most popular property type within the niche.” Ninety-seven percent of investors surveyed in 2017 were most interested in medical office properties among all health care-related real estate that met their investment criteria.

CBRE cites Real Capital Analytics research that estimates total U.S. investment volume in MOBs of at least 10,000 sf at $10.2 billion in 2016, compared to just under $4 billion in 2010. The investment total in 2016 exceeded the previous annual peak of $7.3 billion in 2006.

The Southeast and Western regions have captured a combined 44% of total MOB investment since 2010. California accounted for 56% of the western region MOB investment, with Greater Los Angeles alone representing 37% of the region’s total.

Consolidation has been a major driver of new medical office construction in recent years, as many markets lacked enough large blocks of space to meet the requirements of newly expanded health care provider groups, particularly within close to hospital campuses.

Construction has been abetted by the healthcare systems’ focus on value-based care rather than a fee-for-service approach, which has amplified the need for effective communication across provider teams, driving the need for efficient space that facilitates collaboration.

Over the past two years, completions were highest in the medical hubs of Boston and Houston, each with more than 1.2 million sf of new product delivered. Conversely, only four of the 30 markets analyzed—New York, San Francisco, Orange County, Calif., and Louisville—have had no new completions since Q2 2015.

Related Stories

Healthcare Facilities | Dec 7, 2023

New $650 million Baptist Health Care complex opens in Pensacola

Baptist Health Care’s new $650 million healthcare complex opened recently in Pensacola, Fla. Featuring a 10-story, 268-bed hospital, the project “represents the single-largest investment in the healthcare history of northwest Florida,” said Gresham Smith project executive Robert “Skip” Yauger, AIA, LEED AP. The 602,000 sf Baptist Hospital is equipped with a Level II trauma center that provides 61 exam rooms and three triage areas.

Engineers | Nov 27, 2023

Kimley-Horn eliminates the guesswork of electric vehicle charger site selection

Private businesses and governments can now choose their new electric vehicle (EV) charger locations with data-driven precision. Kimley-Horn, the national engineering, planning, and design consulting firm, today launched TREDLite EV, a cloud-based tool that helps organizations develop and optimize their EV charger deployment strategies based on the organization’s unique priorities.

Healthcare Facilities | Nov 3, 2023

The University of Chicago Medicine is building its city’s first freestanding cancer center with inpatient and outpatient services

The University of Chicago Medicine (UChicago Medicine) is building Chicago’s first freestanding cancer center with inpatient and outpatient services. Aiming to bridge longstanding health disparities on Chicago’s South Side, the $815 million project will consolidate care and about 200 team members currently spread across at least five buildings. The new facility, which broke ground in September, is expected to open to patients in spring 2027.

Sponsored | | Oct 17, 2023

The Evolution of Medical Facility Security

As the healthcare system grows, securing these facilities becomes ever more challenging. Increasingly, medical providers have multiple facilities within their networks, making traditional keying systems and credentialing impractical.

Healthcare Facilities | Oct 11, 2023

Leveraging land and light to enhance patient care

GBBN interior designer Kristin Greeley shares insights from the firm's latest project: a cancer center in Santa Fe, N.M.

Healthcare Facilities | Oct 9, 2023

Design solutions for mental health as a secondary diagnosis

Rachel Vedder, RA, LEED AP, Senior Architect, Design Collaborative, shares two design solutions for hospitals treating behavioral health patients.

Giants 400 | Oct 5, 2023

Top 115 Healthcare Construction Firms for 2023

Turner Construction, Brasfield & Gorrie, JE Dunn Construction, DPR Construction, and McCarthy Holdings top BD+C's ranking of the nation's largest healthcare sector contractors and construction management (CM) firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report. Note: This ranking includes revenue related to all healthcare buildings work, including hospitals, medical office buildings, and outpatient facilities.

Giants 400 | Oct 5, 2023

Top 90 Healthcare Engineering Firms for 2023

Jacobs, WSP, IMEG, BR+A, and Affiliated Engineers head BD+C's ranking of the nation's largest healthcare sector engineering and engineering/architecture (EA) firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report. Note: This ranking includes revenue related to all healthcare buildings work, including hospitals, medical office buildings, and outpatient facilities.

Giants 400 | Oct 5, 2023

Top 175 Healthcare Architecture Firms for 2023

HDR, HKS, CannonDesign, Stantec, and SmithGroup top BD+C's ranking of the nation's largest healthcare sector architecture and architecture/engineering (AE) firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report. Note: This ranking includes revenue related to all healthcare buildings work, including hospitals, medical office buildings, and outpatient facilities.

Adaptive Reuse | Sep 19, 2023

Transforming shopping malls into 21st century neighborhoods

As we reimagine the antiquated shopping mall, Marc Asnis, AICP, Associate, Perkins&Will, details four first steps to consider.