The news this week that the regional First Republic Bank lost $102 billion in bank deposits in the first quarter of 2023—more than half of the $176 billion the bank was holding at the end of last year—was further evidence that investors and depositors are more than a little jittery about the financial condition of the banking industry.

While First Republic stated that its deposit-and-withdrawal activities had stabilized in late March and mid April, the bank is also in the process of reducing its workforce by one quarter and slashing its executive compensation.

First Republic’s travails, coupled with the recent takeover of Silicon Valley Bank and Signature Bank by federal regulators, has industry observers wondering whether these bank failures are signs of something more ominous. This is particularly true among real estate developers that rely heavily on bank lenders to capitalize their purchases and projects.

To sort out the latest banking turmoil and where the Commercial Real Estate (CRE) sector fits in, Cushman & Wakefield on April 19 posted a list of 14 frequently asked questions and weighed in on each. The topics touched on:

•What happened?

•How is this different from other banking failures?

•Why is commercial real estate in the limelight?

•What key metrics bear watching?

“Don’t panic,” C&W advises. But developers should also be aware that recent banking failures have toughened the lending environment; the percentage of banks that say they have tightened their lending standards for CRE loans and other business loans is the highest it’s been in 13 years.

“There are reasons to be both optimistic and concerned,” says C&W. “The sky isn’t falling; at this stage, it’s more overcast than anything else.”

This doesn't look like mid-2000s déjà vu

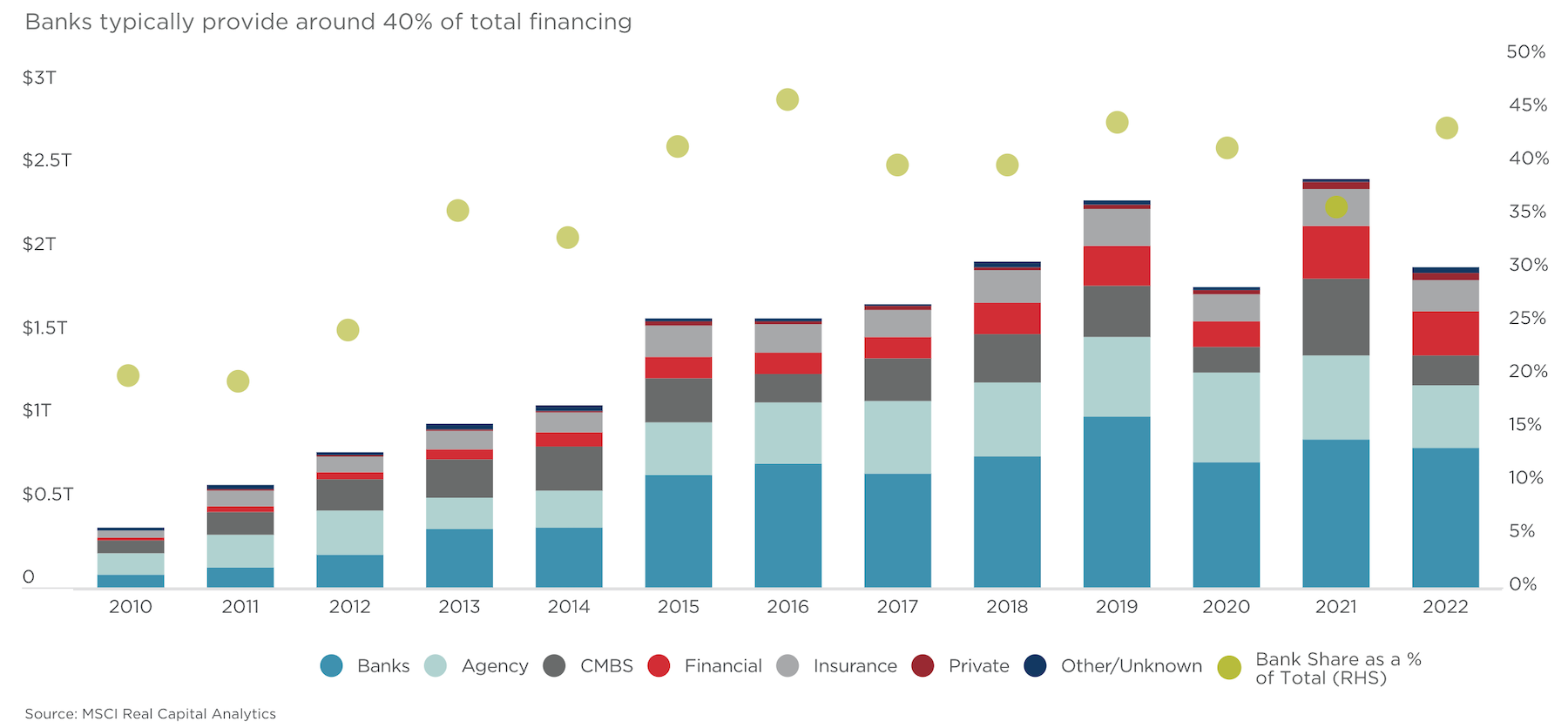

Of all the sources the CRE sector turns to for money, banks provide between 40 and 45 percent of the sector’s financing. Community and regional banks “are the lifeblood of the CRE lending landscape,” says Cushman & Wakefield. And smaller banks are responsible for the majority of multifamily, nonfarm residential, and acquisition/development/construction loan lending.

The failures of a handful of banks, out of a total of more than 5,000, don’t qualify as a crisis. And the banks that have failed in recent months had idiosyncratic factors that contributed to their unraveling. For example, C&W observes that, in the failures of Signature Bank and Silvergate Bank (the latter of which started liquidation proceedings in March), “underlying losses in the value of cryptocurrency served to act as a deposit outflow prior to outright withdrawals happening.”

C&W states that while no bank can survive a run on its deposits, and that a few more failures wouldn’t be a surprise, the U.S. banking system as a whole remains “well capitalized,” with most bank deposits spread across an array of sectors and individuals. The key in the future, C&W says, will be sustaining confidence in the solvency of that system.

It's worth noting that lenders had been pulling back on their CRE lending since last summer, homing in on high-quality assets like industrial and multifamily. C&W is keeping an eye on how the debt market perceives risk for CRE borrowers. On a broader scale, C&W is watching deposit flows, lending patterns to see how banks are navigating incoming maturities, liquidity based on the Federal Reserve’s provision of credit to banks, and jobless claims and inflation, which could be signs of recession.

Recent banking failures haven’t altered Cushman & Wakefield’s prediction of a mild recession in 2023 that will abate as tighter credit and slower economic growth stem inflation.

What C&W doesn’t predict is a repeat of the Great Financial Crisis of the mid-2000s. The financial system is “much stronger” now, and policymakers are responding to problems much quicker and aggressively. The size of the banking failures (so far, at least) is much smaller, and those failures relate not so much to credit but to the ramifications of a rising-rate environment and its impact on bond and securities values.

Most development is an attractive risk

Any weaknesses in the CRE sector will pose challenges to lenders. C&W doesn’t expect those weaknesses to pose a systemic banking sector failure. But, it cautions, there could be isolated instances of loan or credit stress for the banking sector, stemming from any combination of factors that might include oncoming loan maturity, a diminishing of underlying asset value, or deteriorating cash flows.

What does this mean for companies that are leasing space? C&W predicts that most property types will shift toward a tenant-friendlier environment. But landlords will also favor higher-quality tenants “to ensure the viability of the lease agreement.” For companies leasing space in ongoing construction, “the good news is that most development is considered to be attractive on a risk-adjusted basis.” So even if banks pull back, other lending groups are likely to step into that breech.

For signposts about what might happen next, C&W recommends following commercial mortgage-backed securities loan performance data across the CRE industry, and measuring that data against CRE debt financing. It might also be insightful to track prevailing underwriting standards and banks’ forward-looking expectations for the credit market.

What C&W doesn’t recommend is overreacting to the recent failure of Credit Suisse, and its takeover by rival UBS, as indicators of a European domino effect to what’s happening in the U.S.

Related Stories

Office Buildings | Mar 7, 2017

Large creative office projects generate staggering returns for property investors

A new Transwestern report examines the adaptive reuse trend across the U.S.

Industry Research | Mar 7, 2017

These are the 10 most expensive cities in the world to build in

Paris, Frankfurt, and Macau are all on the list, but none of them are more expensive than the city in the number one spot.

Office Buildings | Mar 2, 2017

White paper from Perkins Eastman and Three H examines how design can inform employee productivity and wellbeing

This paper is the first in a planned three-part series of studies on the evolution of diverse office environments and how the contemporary activity-based workplace (ABW) can be uniquely tailored to support a range of employee personalities, tasks and work modes.

Industry Research | Feb 15, 2017

Putting workers first should be every employer’s priority

The latest Sodexo report on workplace trends explores 10 factors that are impacting the global work environment.

Industry Research | Feb 13, 2017

How thought leadership marketing can generate referrals for your firm

The most effective way to boost your reputation is through thought leadership marketing.

Market Data | Feb 1, 2017

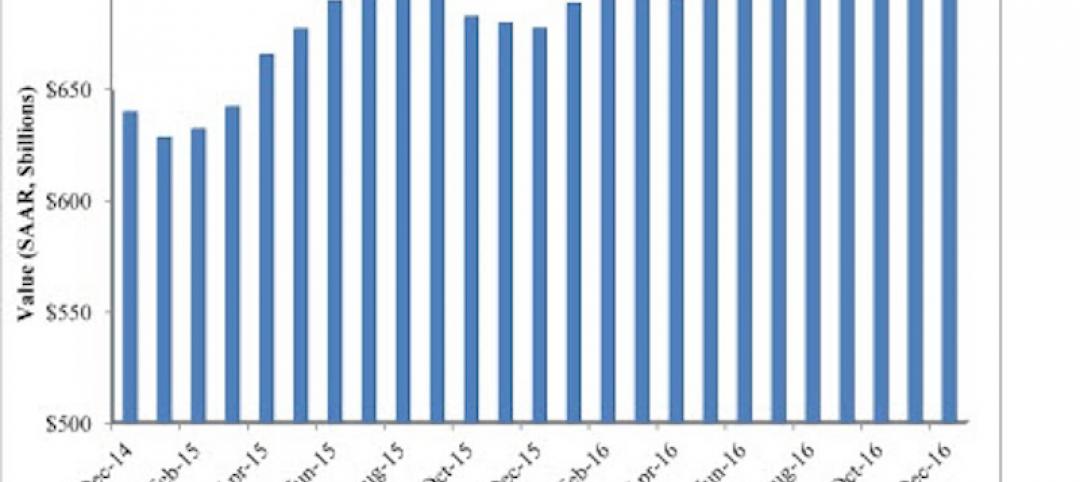

Nonresidential spending falters slightly to end 2016

Nonresidential spending decreased from $713.1 billion in November to $708.2 billion in December.

High-rise Construction | Jan 23, 2017

Growth spurt: A record-breaking 128 buildings of 200 meters or taller were completed in 2016

This marks the third consecutive record-breaking year for building completions over 200 meters.

Market Data | Jan 18, 2017

Fraud and risk incidents on the rise for construction, engineering, and infrastructure businesses

Seven of the 10 executives in the sector surveyed in the report said their company fell victim to fraud in the past year.

Market Data | Jan 18, 2017

Architecture Billings Index ends year on positive note

Architecture firms close 2016 with the strongest performance of the year.

Industry Research | Jan 12, 2017

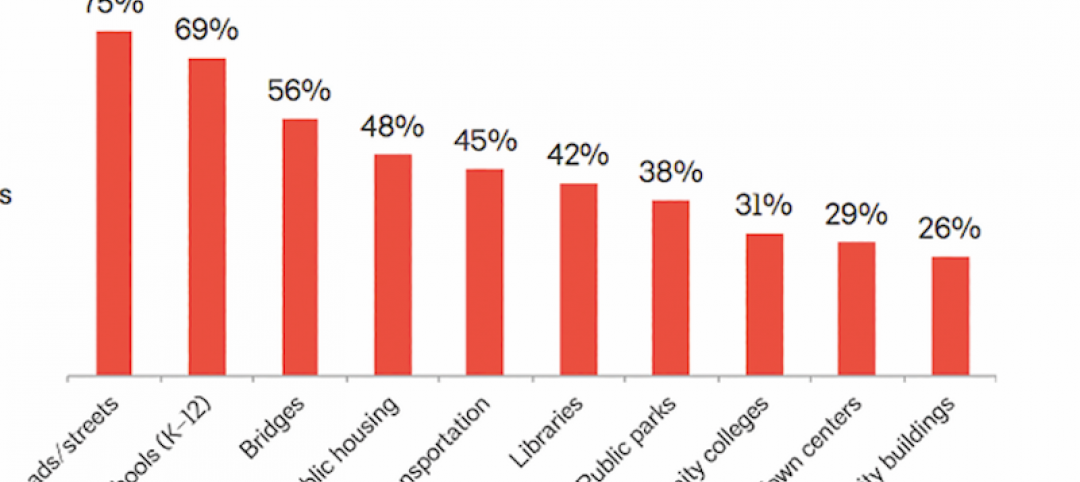

Are public buildings considered infrastructure?

A survey, conducted in October by The Harris Poll on behalf of AIA, asked 2,108 U.S. adults if they considered public buildings part of their community’s infrastructure.