The relatively steep slowdown in the growth in construction spending in recent years might suggest that this year might result in a decline in overall spending. However, quite the contrary, the AIA Consensus Construction Forecast panel is projecting a modest pick-up in the growth rate, and another solid performance in 2019. There appear to be several factors behind this optimism:

1. Rebuilding and repairs from natural disasters: The National Oceanographic and Atmospheric Administration recently reported its 2017 estimate of losses from major natural disasters like hurricanes, wildfires, and flooding. At $306 billion, it easily shattered the previous record of $215 billion (adjusted for inflation) set in 2005 from the impacts of Katrina, Rita, Wilma, and Dennis. While the totality of these loss figures won’t be directly translated into rebuilding and repair activity, they will produce significant opportunities for the construction sector. Existing research suggests that the duration of rebuilding activity after natural disasters is significant, with the peak in spending generally occurring two to three years after the event.

2. Tax reform implications for construction: The recently enacted tax reform package dramatically reduced the nominal tax rates for businesses, and some of these savings will likely be reinvested back into the businesses. With capital expenditures able to be expensed rather than depreciated under the tax act, businesses have even more incentive to invest in their businesses. The impact of tax reform on business profitability will vary by industry, with more capital intensive industries (e.g. utilities, real estate, and transportation) and those with higher effective tax rates (e.g. agriculture, financial services) potentially benefiting the most. In contrast, the single-family housing market recovery is likely to be slowed by the tax package. The lower limits for the deductibility of mortgage interest, as well as the cap set on state and local tax deductions (including property taxes) reduce the tax preferences for homeownership, and likely will moderate growth in house prices, particularly for upper-end homes in areas with high state and local tax rates.

3. Possibility of an infrastructure package: A priority of the Trump administration has been an infrastructure investment program. There have been several versions floated, with the current iteration calling for a $200-billion federal investment over the coming decade leveraging and additional $800 billion in state, local, and private investment. The details of such a program, and the likelihood of its being implemented, should unfold over the coming weeks.

4. Strong consumer and business confidence levels: Consumer sentiment—as measured by the University of Michigan consumer sentiment index—turned up in the latter part of 2017, with fourth-quarter figures at their highest levels in almost two decades. Likewise, business confidence levels in 2017, as measured by the Conference Board’s CEO business confidence survey, were at their highest point since before the last recession. These indicators suggest broad confidence in economic conditions across both households and businesses, and a willingness to spend and invest.

5. Leading economic indicators for the construction sector: While there are several “special circumstances” that may provide growth opportunities for the construction sector this year, there are other more basic indicators that point to growth. AIA’s ABI has been signaling growth in design activity for most of the past year, which would point to a comparable upturn in construction activity throughout 2018. Even more significant, the AIA’s index for new design projects coming into architecture firms saw an even sharper upturn than the overall ABI in 2017, demonstrating a growing pipeline for design activity. Additionally, both Dodge Data and Analytics and ConstructConnect reported strong gains in nonresidential building starts in 2017, demonstrating considerable building activity currently under way.

Related Stories

Giants 400 | Aug 31, 2023

Top 35 Engineering Architecture Firms for 2023

Jacobs, AECOM, Alfa Tech, Burns & McDonnell, and Ramboll top the rankings of the nation's largest engineering architecture (EA) firms for nonresidential buildings and multifamily buildings work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Aug 22, 2023

Top 115 Architecture Engineering Firms for 2023

Stantec, HDR, Page, HOK, and Arcadis North America top the rankings of the nation's largest architecture engineering (AE) firms for nonresidential building and multifamily housing work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Aug 22, 2023

2023 Giants 400 Report: Ranking the nation's largest architecture, engineering, and construction firms

A record 552 AEC firms submitted data for BD+C's 2023 Giants 400 Report. The final report includes 137 rankings across 25 building sectors and specialty categories.

Giants 400 | Aug 22, 2023

Top 175 Architecture Firms for 2023

Gensler, HKS, Perkins&Will, Corgan, and Perkins Eastman top the rankings of the nation's largest architecture firms for nonresidential building and multifamily housing work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Apartments | Aug 22, 2023

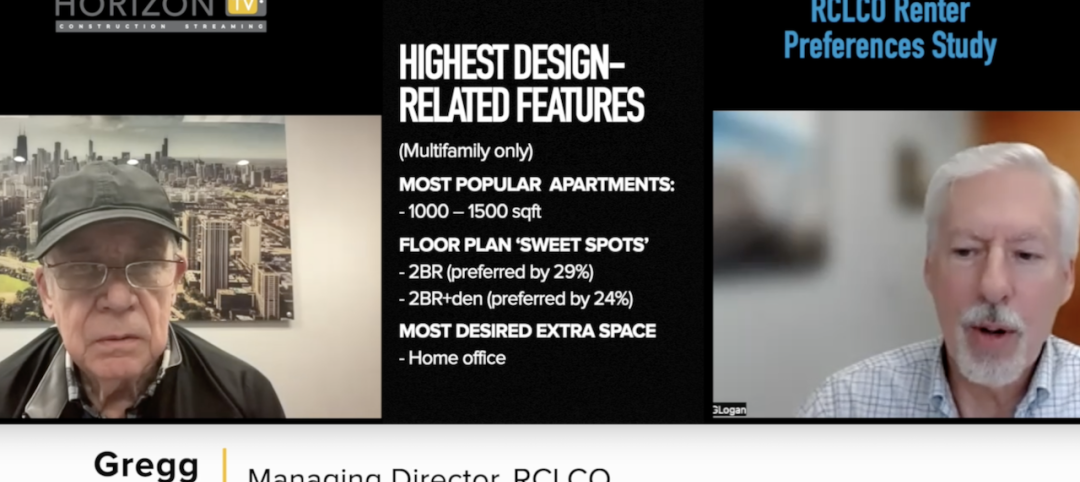

Key takeaways from RCLCO's 2023 apartment renter preferences study

Gregg Logan, Managing Director of real estate consulting firm RCLCO, reveals the highlights of RCLCO's new research study, “2023 Rental Consumer Preferences Report.” Logan speaks with BD+C's Robert Cassidy.

Apartments | Aug 14, 2023

Yardi Matrix updates near-term multifamily supply forecast

The multifamily housing supply could increase by up to nearly 7% by the end of 2023, states the latest Multifamily Supply Forecast from Yardi Matrix.

Sports and Recreational Facilities | Jul 26, 2023

10 ways public aquatic centers and recreation centers benefit community health

A new report from HMC Architects explores the critical role aquatic centers and recreation centers play in society and how they can make a lasting, positive impact on the people they serve.

Market Data | Jul 24, 2023

Leading economists call for 2% increase in building construction spending in 2024

Following a 19.7% surge in spending for commercial, institutional, and industrial buildings in 2023, leading construction industry economists expect spending growth to come back to earth in 2024, according to the July 2023 AIA Consensus Construction Forecast Panel.

Codes and Standards | Jul 17, 2023

Outdated federal rainfall analysis impacting infrastructure projects, flood insurance

Severe rainstorms, sometimes described as “atmospheric rivers” or “torrential thunderstorms,” are making the concept of a “1-in-100-year flood event” obsolete, according to a report from First Street Foundation, an organization focused on weather risk research.

Multifamily Housing | Jul 13, 2023

Walkable neighborhoods encourage stronger sense of community

Adults who live in walkable neighborhoods are more likely to interact with their neighbors and have a stronger sense of community than people who live in car-dependent communities, according to a report by the Herbert Wertheim School of Public Health and Human Longevity Science at University of California San Diego.