One year after the pandemic struck, construction firms are experiencing soaring materials costs, widespread supply-chain problems, and continuing project deferrals and cancellations, according to a new survey that the Associated General Contractors of America released today. Association officials urged Congress and the Biden administration to take steps to eliminate tariffs on key materials, address shipping backups and boost funding for new infrastructure to help the industry recovery.

“The survey results make it clear that the construction industry faces a variety of challenges that threaten to leave many firms and workers behind, even as some parts of the economy are recovering or even thriving,” said Ken Simonson, the association’s chief economist. “The pandemic has left the supply chain for a range of key construction components in tatters and undermined demand for a host of private-sector projects.”

Simonson noted that an overwhelming 93% of the survey’s respondents report the pandemic has driven up their costs. Four out of five are spending more on personal protective equipment, sanitizers, and other health-related expenses. More than half say that projects are taking longer than previously.

Costs and delayed deliveries of materials, parts, and supplies are vexing many contractors. Nearly 85% report those costs have increased over the past year. In addition, nearly three-fourths of the firms are currently experiencing project delays and disruptions, mainly due to shortages of materials, equipment or parts. Nine out of ten firms that are incurring such delays cite backlogs and shutdowns at domestic producers, such as factories, mills, and fabricators. Half of the firms also blame backlogs or shutdowns at foreign producers.

More than three-fourths of the firms report having projects canceled or postponed in the past year, including more than one out of five with a 2021 project that has been canceled or postponed. Meanwhile, only one-fifth of respondents say they have won new projects or add-ons to existing projects as a result of the pandemic.

In a sign that the pandemic has had very different effects on construction firms, about one-third of firms say business matches or exceeds year-ago levels, while another third say it will take more than six months to reach that mark, and one-fifth say they don’t know. Respondents in the Northeast are the most pessimistic about the outlook, followed by firms in the South. Firms from the Midwest are split along the same lines as the full survey, while respondents in the West are more optimistic, on balance.

Despite these differences in experience to date and the near-term outlook, contractors from all regions, project types, and firm sizes are almost equally bullish about their hiring expectations over the next 12 months. Across nearly all subgroups, roughly three out of five respondents expect to add employees over the coming 12 months. Only 10 to 15% of firms in any category expect to reduce their headcount.

“Contractors need Washington officials to cut tariffs and address the shipping and supply chain problems that are driving costs and contributing to project delays,” said Brian Turmail, the association’s spokesman. “They also expect the President will keep his word and get significant new infrastructure investments enacted as quickly as possible.”

View the survey results.

Related Stories

Market Data | Nov 29, 2016

It’s not just traditional infrastructure that requires investment

A national survey finds strong support for essential community buildings.

Industry Research | Nov 28, 2016

Building America: The Merit Shop Scorecard

ABC releases state rankings on policies affecting construction industry.

Multifamily Housing | Nov 28, 2016

Axiometrics predicts apartment deliveries will peak by mid 2017

New York is projected to lead the nation next year, thanks to construction delays in 2016

Market Data | Nov 22, 2016

Construction activity will slow next year: JLL

Risk, labor, and technology are impacting what gets built.

Market Data | Nov 17, 2016

Architecture Billings Index rebounds after two down months

Decline in new design contracts suggests volatility in design activity to persist.

Market Data | Nov 11, 2016

Brand marketing: Why the B2B world needs to embrace consumers

The relevance of brand recognition has always been debatable in the B2B universe. With notable exceptions like BASF, few manufacturers or industry groups see value in generating top-of-mind awareness for their products and services with consumers.

Industry Research | Nov 8, 2016

Austin, Texas wins ‘Top City’ in the Emerging Trends in Real Estate outlook

Austin was followed on the list by Dallas/Fort Worth, Texas and Portland, Ore.

Market Data | Nov 2, 2016

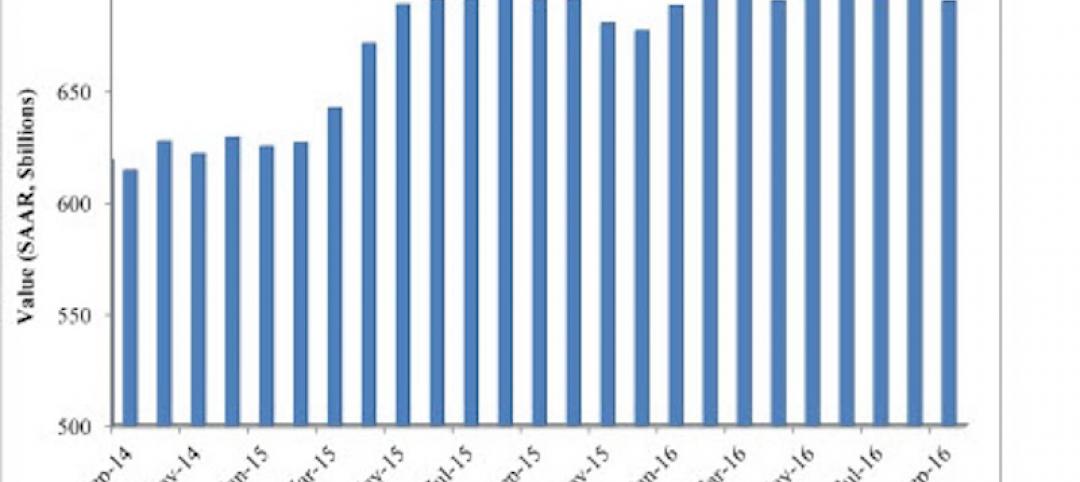

Nonresidential construction spending down in September, but August data upwardly revised

The government revised the August nonresidential construction spending estimate from $686.6 billion to $696.6 billion.

Market Data | Oct 31, 2016

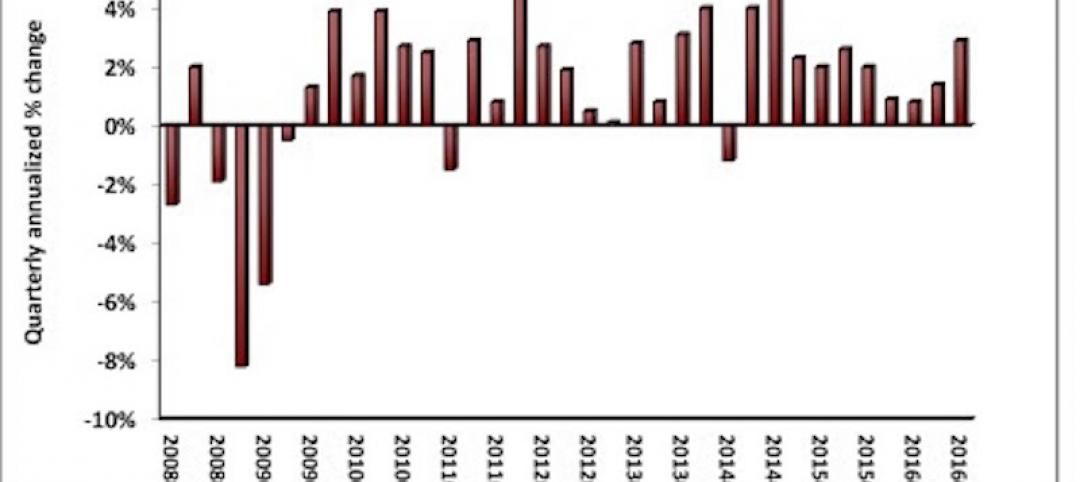

Nonresidential fixed investment expands again during solid third quarter

The acceleration in real GDP growth was driven by a combination of factors, including an upturn in exports, a smaller decrease in state and local government spending and an upturn in federal government spending, says ABC Chief Economist Anirban Basu.

Market Data | Oct 28, 2016

U.S. construction solid and stable in Q3 of 2016; Presidential election seen as influence on industry for 2017

Rider Levett Bucknall’s Third Quarter 2016 USA Construction Cost Report puts the complete spectrum of construction sectors and markets in perspective as it assesses the current state of the industry.