A recent survey of more than 200 subcontractors and suppliers in the Northeast found that respondents have been prefabricating 20% more than they did prior to the COVID-19 pandemic. And 71% said that they had seen an increase in requests for design-assist proposals, a strong sign that speed-to-market is a priority.

Consigli Construction’s Market Outlook Report for the first and second quarters of 2021 states that the pandemic has motivated subs and vendors to turn to technology in their shops and field processes. The survey’s respondents are also more receptive to cost-saving material management software, tool upgrades, and robotics that improve efficiency and give subs the flexibility they need to manage on-site workforces at a time when skilled labor is in short supply in some markets.

While 72% of the survey’s respondents say they aren’t concerned about staffing their projects this year, Consigli suggests they need to monitor their workforce resources for 2022, based on the amount of work in the pipeline.

PRICING AND SUPPLY ARE ISSUES FOR SEVERAL PRODUCT

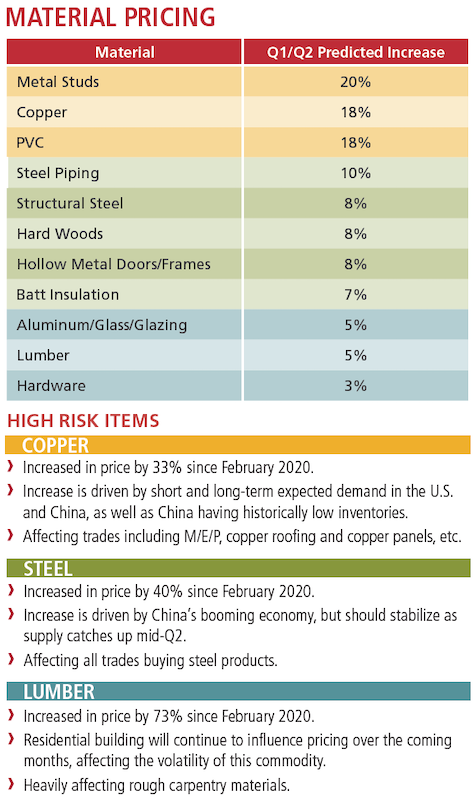

The Market Outlook expects copper and steel to manifest the greatest risk for price inflation. Chart: Consigli Construction

The Market Outlook Report also looks at materials price inflation in several product categories (see chart). Metal studs, copper, and PVC are the materials that the report expects to show the greatest price increases in the first half of the year. The report also suggests that lumber—whose pricing had jumped by 73% since February 2020—could be stabilizing, depending on residential demand.

(The Commerce Department reported last week that housing starts had surged to a nearly 15-year high in March.)

Consigli recommends that subs keep a close eye on high-risk materials, and lock in prices as soon as possible to avoid exposure to inflation. Subs should also watch for supply-chain disruptions, especially for products coming from overseas like flooring and cabinetry. Where possible, have access to alternate materials and delivery options.

Related Stories

Industry Research | Jan 30, 2018

AIA’s Kermit Baker: Five signs of an impending upturn in construction spending

Tax reform implications and rebuilding from natural disasters are among the reasons AIA’s Chief Economist is optimistic for 2018 and 2019.

Market Data | Jan 30, 2018

AIA Consensus Forecast: 4.0% growth for nonresidential construction spending in 2018

The commercial office and retail sectors will lead the way in 2018, with a strong bounce back for education and healthcare.

Market Data | Jan 29, 2018

Year-end data show economy expanded in 2017; Fixed investment surged in fourth quarter

The economy expanded at an annual rate of 2.6% during the fourth quarter of 2017.

Market Data | Jan 25, 2018

Renters are the majority in 42 U.S. cities

Over the past 10 years, the number of renters has increased by 23 million.

Market Data | Jan 24, 2018

HomeUnion names the most and least affordable rental housing markets

Chicago tops the list as the most affordable U.S. metro, while Oakland, Calif., is the most expensive rental market.

Market Data | Jan 12, 2018

Construction input prices inch down in December, Up YOY despite low inflation

Energy prices have been more volatile lately.

Market Data | Jan 4, 2018

Nonresidential construction spending ticks higher in November, down year-over-year

Despite the month-over-month expansion, nonresidential spending fell 1.3 percent from November 2016.

Contractors | Jan 4, 2018

Construction spending in a ‘mature’ period of incremental growth

Labor shortages are spiking wages. Materials costs are rising, too.

reported the November ABI score was 55.0, up from a score of 51.7 in the previous month. Photo: Pixabay")

Market Data | Dec 20, 2017

Architecture billings upturn shows broad strength

The American Institute of Architects (AIA) reported the November ABI score was 55.0, up from a score of 51.7 in the previous month.

Market Data | Dec 14, 2017

ABC chief economist predicts stable 2018 construction economy

There are risks to the 2018 outlook as a number of potential cost increases could come into play.