Coming off of a year when nonresidential building starts fell by an estimated 7.5%, the industry is expected to bounce back in 2016, especially during the second and third quarters when the annualized growth rate for starts could hit 15% before decelerating later in the year.

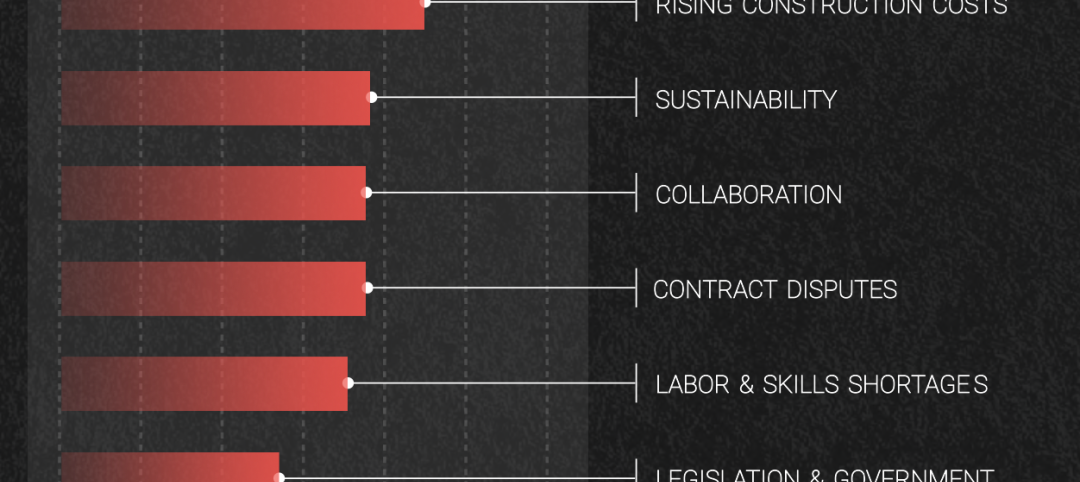

However, keeping projects on schedule and on budget will continue to be difficult if, as expected, worker shortages persist, leading to higher labor costs and, potentially, construction delays.

In Gilbane’s Winter 2015-2016 Market Conditions in Construction report, which can be downloaded from here, the giant contractor forecasts nonresidential building starts to increase by 8.5% this year to 222,764.

Gilbane expects spending on nonresidential buildings, which grew by 17.1% to $386.4 billion in 2015, to keep rising this year, by 13.7% to $439.2 billion. However, spending should taper off late this year, “leading to a considerably slower 2017.”

On the whole, nonresidential building sectors should enjoy good years, according to Gilbane’s report, whose spending projections for 2016 include:

•13.6% growth for Educational buildings

•A 13.8% rise for Healthcare construction

•22.5% growth for Amusement and Recreational buildings.

•A 6% spending increase for Retail space

•A retreat in spending for Office buildings, which after gains of 21.3% and 21.4% in the last two years, should increase by only 4.7% in 2016. “Although down 15% in 2015, starts have been strong and multiple months of large volume starts will help keep 2016 spending positive. Office spending is projected to grow again in 2017,” the report states.

•Spending for lodging, which grew by 31% last year, and by 90% during the 2012-2015 period, should increase by 10.8% this year, when starts are expected to be up 16%, “leading to continued spending growth in 2017.”

•Despite a nearly 30% decline in starts last year, manufacturing-related building still hit its second-highest starts level on record, and spending jumped 44.8%. Those starts should drive spending up another 10.8% in 2016.

On average, $1 billion of spending supports approximately 6,000 construction jobs, and generates up to 28,000 jobs in the economy. But Gilbane remains concerned about the ability of contractors to find skilled labor to meet the country’s escalating construction demands. It points out that while the total construction workforce is growing and is near 7.3 million, that is still about 1 million workers short of the 2006-2007 peak.

It cites the Bureau of Labor Statistics’ Job Openings and Labor Turnover Survey (JOLTS) for the construction industry, which showed 139,000 unfilled positions for October 2015. Gilbane notes that the openings rate has been trending upward since 2012. “A relatively high rate of openings … generally indicates high demand for labor and could lead to higher wage rates,” its report states.

Gilbane’s analyst Ed Zarenski expects construction job gains of between 500,000 and 600,000 through 2017. But Gilbane still foresees shortages of skilled workers over the next five years, as well as declining productivity, and rapidly increasing labor cost. “If you are in a location where a large volume of pent-up work starts all at once, you will experience these three issues.”

Related Stories

Contractors | Jul 13, 2023

Construction input prices remain unchanged in June, inflation slowing

Construction input prices remained unchanged in June compared to the previous month, according to an Associated Builders and Contractors analysis of U.S. Bureau of Labor Statistics Producer Price Index data released today. Nonresidential construction input prices were also unchanged for the month.

Contractors | Jul 11, 2023

The average U.S. contractor has 8.9 months worth of construction work in the pipeline, as of June 2023

Associated Builders and Contractors reported that its Construction Backlog Indicator remained unchanged at 8.9 months in June 2023, according to an ABC member survey conducted June 20 to July 5. The reading is unchanged from June 2022.

Market Data | Jul 5, 2023

Nonresidential construction spending decreased in May, its first drop in nearly a year

National nonresidential construction spending decreased 0.2% in May, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau. On a seasonally adjusted annualized basis, nonresidential spending totaled $1.06 trillion.

Apartments | Jun 27, 2023

Average U.S. apartment rent reached all-time high in May, at $1,716

Multifamily rents continued to increase through the first half of 2023, despite challenges for the sector and continuing economic uncertainty. But job growth has remained robust and new households keep forming, creating apartment demand and ongoing rent growth. The average U.S. apartment rent reached an all-time high of $1,716 in May.

Industry Research | Jun 15, 2023

Exurbs and emerging suburbs having fastest population growth, says Cushman & Wakefield

Recently released county and metro-level population growth data by the U.S. Census Bureau shows that the fastest growing areas are found in exurbs and emerging suburbs.

Contractors | Jun 13, 2023

The average U.S. contractor has 8.9 months worth of construction work in the pipeline, as of May 2023

Associated Builders and Contractors reported that its Construction Backlog Indicator remained unchanged at 8.9 months in May, according to an ABC member survey conducted May 20 to June 7. The reading is 0.1 months lower than in May 2022. Backlog in the infrastructure category ticked up again and has now returned to May 2022 levels. On a regional basis, backlog increased in every region but the Northeast.

Industry Research | Jun 13, 2023

Two new surveys track how the construction industry, in the U.S. and globally, is navigating market disruption and volatility

The surveys, conducted by XYZ Reality and KPMG International, found greater willingness to embrace technology, workplace diversity, and ESG precepts.

| Jun 5, 2023

Communication is the key to AEC firms’ mental health programs and training

The core of recent awareness efforts—and their greatest challenge—is getting workers to come forward and share stories.

Contractors | May 24, 2023

The average U.S. contractor has 8.9 months worth of construction work in the pipeline, as of April 2023

Contractor backlogs climbed slightly in April, from a seven-month low the previous month, according to Associated Builders and Contractors.

Multifamily Housing | May 23, 2023

One out of three office buildings in largest U.S. cities are suitable for residential conversion

Roughly one in three office buildings in the largest U.S. cities are well suited to be converted to multifamily residential properties, according to a study by global real estate firm Avison Young. Some 6,206 buildings across 10 U.S. cities present viable opportunities for conversion to residential use.