Construction firms are struggling to find enough qualified workers to hire even as they continue to be impacted by pandemic-induced project delays and supply chain disruptions, according to the results of a workforce survey conducted by the Associated General Contractors of America and Autodesk. The survey results underscore how the coronavirus pandemic has created constraints on the demand for work even as it limits the number of workers available to hire.

“Market conditions are nowhere near as robust as they were prior to the onset of the pandemic,” said Ken Simonson, the association’s chief economist. “At the same time, the pandemic and political responses to it are limiting the size of the workforce, leading to labor shortages that are as severe as they were in 2019 when demand for construction was more robust.”

Simonson noted that nearly nine out of ten firms (88%) are experiencing project delays. Among these firms, 75% cite delays due to longer lead times or shortages of materials, while 57% cite delivery delays. Sixty-one percent of firms said their projects are being delayed because of workforce shortages. And delays due to the lack of approvals or inspectors, or an owner’s directive to halt or redesign a project, were each cited by 30% of contractors.

An even higher percentage of firms, 93%, report that rising materials costs have affected their projects. These rising materials costs are undermining firms’ abilities to profit from the work they have, with 37 percent reporting they have been unsuccessful in passing those added costs onto project owners.

As a result of these supply chain challenges, more than half of firms report having projects canceled, postponed or scaled back due to increasing costs. Twenty-six percent of firms report their projects have been delayed or canceled because of lengthening or uncertain completion times and 22% say changing market conditions have led to project delays or cancellations.

These challenging market conditions are a key reason why 26% of respondents expect it will take more than six months for their firm’s revenue to match or exceed year-earlier levels. And 17% are unsure when to expect a return to previous demand levels.

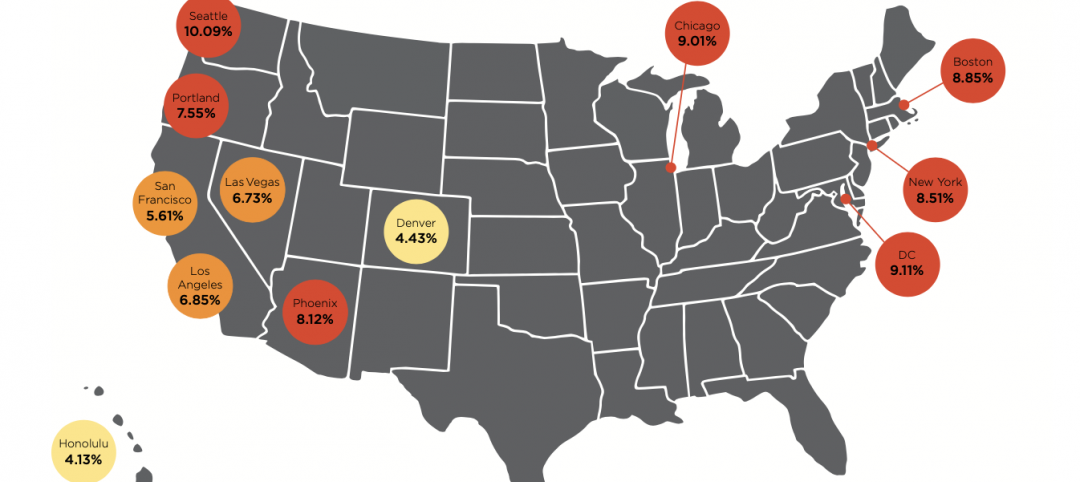

While the pandemic has led to project delays and cancellations nationwide, contractor expectations of recovery do vary by region. Forty percent of respondents in the Northeast expect it will take more than six months for their firm’s volume of business to return to normal, compared to only 12% of respondents in the Midwest, 22% in the West, and 34% in the South.

There are also some differences by project type and revenue size. For instance, 100% of building contractors and 97% of firms that work on federal government projects report at least some projects were canceled, postponed or scaled back, compared to 61% of utility infrastructure contractors and 56% of highway and transportation contractors. Two-thirds of the firms with revenues that exceeded $500 million increased their headcount in the past 12 months, compared to just over half (53%) of midsized firms—those with revenues of $50.1 million to $500 million—and slightly more than one-third (36%) of firms with revenues of $50 million or less.

Despite these challenges, contractors report as much difficulty filling positions as they experienced before the pandemic. Eighty-nine percent of firms that are seeking to fill hourly craft positions report having a hard time doing so. And 86% of firms seeking to fill salaried positions are also having a hard time hiring.

There are two main reasons so many firms report having trouble finding workers to hire. The first is that 72% of firms say available candidates are not qualified to work in the industry due to a lack of skills, failure to pass a drug test, etc. The lack of qualified candidates affects union and open-shop firms almost equally: 70% of firms that always use union craft workers exclusively and 74% of open-shop firms report a lack of qualified candidates. And 58% of respondents report that unemployment insurance supplements are keeping workers away.

As a result of these shortages, almost one-third of firms report they have increased spending on training and professional development. Most firms, 73%, report they have increased base pay rates during the past year. And just over one-third of firms have also provided hiring bonuses or incentives during the past year.

In addition, 37% of firms report engaging with career-building programs at the high school, collegiate or career and technical levels. Thirty-one percent have added online strategies – like Instagram Live – to better connect with younger applicants. And roughly one-in-four say they have partnered with government workforce development or unemployment agencies or used software to track job applications.

Many firms have turned to new technologies to become more efficient operators. Fifty-seven percent of respondents report the rate of technology adoption at their firms has increased over the last 12 months. And 60% said they anticipate the rate of technology adoption at their firms to increase within the next 12 months.

“Challenges often drive resolve, and we started to see this acutely in the construction industry last year” said Allison Scott, director of construction thought leadership and customer marketing at Autodesk. “The continued investments in hiring, training and technology highlighted in this year’s study show that even while dealing with ongoing challenges nearly two years into the pandemic, the industry remains committed to building better with a resilient workforce.”

Association officials called on Washington leaders to take steps to help address challenging market conditions and labor shortages. They urged House members to quickly pass a bipartisan infrastructure measure that already passed in the Senate. And they called on the Biden administration and Congress to work together to boost investments in career and technical education.

“The federal government currently spends only one dollar on career training for every six it puts into college prep, despite the fact only one-in-three jobs requires a college degree,” said Stephen E. Sandherr, the association’s chief executive officer. “Boosting federal investments in career and technical education will help attract and prepare more people into high-paying careers in construction.”

Association officials added that they were supporting members’ efforts to address labor shortages. This includes launching a targeted digital advertising campaign, “Construction is Essential,” and providing resources to help members establish or improve construction training programs. And the association’s “Culture of Care” program is designed to help firms retain newly hired workers.

The association and Autodesk conducted the Workforce Survey in late July and early August. Over 2,100 firms completed the survey from a broad cross-section of the construction industry, including union and open shop firms of all sizes. The 2021 Workforce Survey is the association’s ninth annual workforce-related survey.

Click here for survey materials including national, regional and state fact sheets, survey analysis and event remarks.

Related Stories

Market Data | Jan 31, 2022

Canada's hotel construction pipeline ends 2021 with 262 projects and 35,325 rooms

At the close of 2021, projects under construction stand at 62 projects/8,100 rooms.

Market Data | Jan 27, 2022

Record high counts for franchise companies in the early planning stage at the end of Q4'21

Through year-end 2021, Marriott, Hilton, and IHG branded hotels represented 585 new hotel openings with 73,415 rooms.

Market Data | Jan 27, 2022

Dallas leads as the top market by project count in the U.S. hotel construction pipeline at year-end 2021

The market with the greatest number of projects already in the ground, at the end of the fourth quarter, is New York with 90 projects/14,513 rooms.

Market Data | Jan 26, 2022

2022 construction forecast: Healthcare, retail, industrial sectors to lead ‘healthy rebound’ for nonresidential construction

A panel of construction industry economists forecasts 5.4 percent growth for the nonresidential building sector in 2022, and a 6.1 percent bump in 2023.

Market Data | Jan 24, 2022

U.S. hotel construction pipeline stands at 4,814 projects/581,953 rooms at year-end 2021

Projects scheduled to start construction in the next 12 months stand at 1,821 projects/210,890 rooms at the end of the fourth quarter.

Market Data | Jan 19, 2022

Architecture firms end 2021 on a strong note

December’s Architectural Billings Index (ABI) score of 52.0 was an increase from 51.0 in November.

Market Data | Jan 13, 2022

Materials prices soar 20% in 2021 despite moderating in December

Most contractors in association survey list costs as top concern in 2022.

Market Data | Jan 12, 2022

Construction firms forsee growing demand for most types of projects

Seventy-four percent of firms plan to hire in 2022 despite supply-chain and labor challenges.

Market Data | Jan 7, 2022

Construction adds 22,000 jobs in December

Jobless rate falls to 5% as ongoing nonresidential recovery offsets rare dip in residential total.

Market Data | Jan 6, 2022

Inflation tempers optimism about construction in North America

Rider Levett Bucknall’s latest report cites labor shortages and supply chain snags among causes for cost increases.