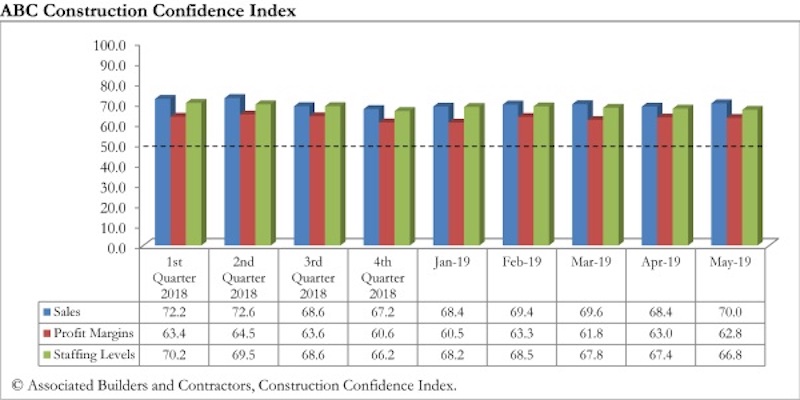

U.S. construction industry leaders remained upbeat regarding nonresidential construction’s near-term prospects in May 2019, according to the Construction Confidence Index released today by Associated Builders and Contractors.

While contractors were slightly less upbeat regarding profit margins and staffing levels compared to April, all three principal components measured by the survey—sales, profit margins and staffing levels—remain well above the diffusion index threshold of 50 in May. Nearly 73% of contractors expect sales to rise during the next six months and 68% expect staffing levels to increase further.

- The CCI for sales expectations increased from 68.4 to 70.0 in May.

- The CCI for profit margin expectations fell slightly from 63.0 to 62.8.

- The CCI for staffing levels fell from 67.4 to 66.8.

“While there continues to be considerable chatter regarding a slowing economy, the need for federal rate cuts and the damaging effects of ongoing trade disputes involving the United States, China, the European Union and India, among others, nonresidential firm leaders continue to expect further construction spending growth,” said ABC Chief Economist Anirban Basu. “Recent data regarding job growth and consumer spending indicate that any economic slowing to date has been mild and that the expansion is set to endure for the next few quarters.

“While profit margin expectations and staffing levels measures declined slightly in May, they remained well above the threshold level of 50,” said Basu. “More importantly, these CCI measures likely declined due to economic strength rather than weakness. Firms continue to scramble for talent in the context of an economy offering more job openings than jobseekers. As a result, staffing levels cannot rise rapidly even in the context of elevated demand for workers, and profit margins are negatively impacted by the accompanying rapid rise in compensation costs. However, far more industry leaders expect profit margins to rise than decline.

“As we reach the longest economic expansion in American history, recent construction spending data indicate that much of the momentum is coming from public projects,” said Basu. “Years of growth have helped to stabilize state and local government finances, resulting in more money available to fund transportation, water, public safety and other projects. While spending in certain private segments has been expanding less rapidly of late, this nascent weakness has been more than fully countervailed by the strength of investment in infrastructure.”

CCI is a diffusion index. Readings above 50 indicate growth, while readings below 50 are unfavorable.

.jpg%3Fver%3D2019-07-18-104421-307&I=20190718150919.0000053f0b67%40mail6-60-usnbn1&X=MHwxMDQ2NzU4OjVkMzA3OTVhZDdkNzRjY2IwYWNjM2ViYzs%3D&S=cVBNKOEoq6MUK-bwGgOO7KJ8uiyNh3t6BAKLaMNS0L0)

Related Stories

Market Data | May 2, 2017

Nonresidential Spending loses steam after strong start to year

Spending in the segment totaled $708.6 billion on a seasonally adjusted, annualized basis.

Market Data | May 1, 2017

Nonresidential Fixed Investment surges despite sluggish economic in first quarter

Real gross domestic product (GDP) expanded 0.7 percent on a seasonally adjusted annualized rate during the first three months of the year.

Industry Research | Apr 28, 2017

A/E Industry lacks planning, but still spending large on hiring

The average 200-person A/E Firm is spending $200,000 on hiring, and not budgeting at all.

Market Data | Apr 19, 2017

Architecture Billings Index continues to strengthen

Balanced growth results in billings gains in all regions.

Market Data | Apr 13, 2017

2016’s top 10 states for commercial development

Three new states creep into the top 10 while first and second place remain unchanged.

Market Data | Apr 6, 2017

Architecture marketing: 5 tools to measure success

We’ve identified five architecture marketing tools that will help your firm evaluate if it’s on the track to more leads, higher growth, and broader brand visibility.

Market Data | Apr 3, 2017

Public nonresidential construction spending rebounds; overall spending unchanged in February

The segment totaled $701.9 billion on a seasonally adjusted annualized rate for the month, marking the seventh consecutive month in which nonresidential spending sat above the $700 billion threshold.

Market Data | Mar 29, 2017

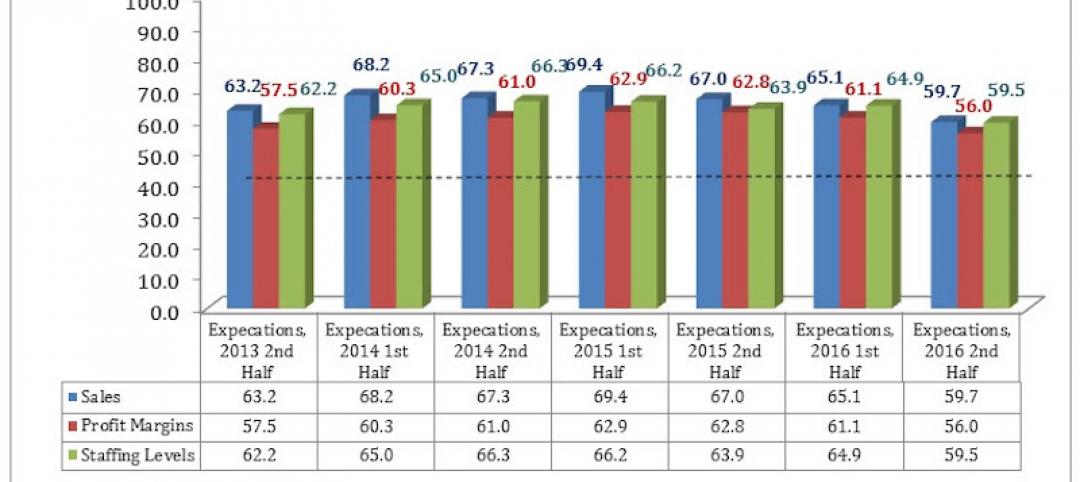

Contractor confidence ends 2016 down but still in positive territory

Although all three diffusion indices in the survey fell by more than five points they remain well above the threshold of 50, which signals that construction activity will continue to be one of the few significant drivers of economic growth.

Market Data | Mar 24, 2017

These are the most and least innovative states for 2017

Connecticut, Virginia, and Maryland are all in the top 10 most innovative states, but none of them were able to claim the number one spot.

Market Data | Mar 22, 2017

After a strong year, construction industry anxious about Washington’s proposed policy shifts

Impacts on labor and materials costs at issue, according to latest JLL report.