Contractors continue to face a shortage of building materials like lumber and steel, while cost fluctuations for the building products are having increasing impact on business, according to second quarter data from the U.S. Chamber of Commerce Commercial Construction (Index). This quarter, 84% of contractors are facing at least one material shortage. Almost half (46%) of contractors say less availability of building products has been a top concern lately, up from 33% who said the same last quarter.

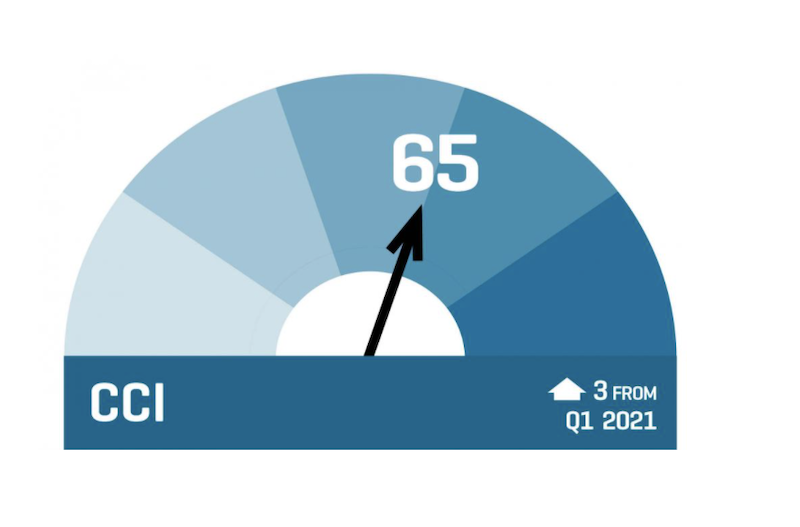

Despite the materials challenges, the overall Index score rose three points to 65 (its highest reading since a score of 74 in Q1 2020 ahead of the pandemic) and contractors are optimistic on outlook for revenue expectations, new business

— 89% of contractors report a moderate to high level of confidence in new business opportunities in the next 12 months, up from 86% in Q1. Those indicating a high level of confidence jumped 10 points to 34% from last quarter.

— Over half (52%) of contractors say they will hire more employees in the next six months, up from 46% in Q1.

— More contractors (39%) expect

— For the first time in a year, the percentage of contractors planning to spend more on tools and equipment in the next six months (44%) is higher than those who say they will not spend more (42%).

“Businesses are experiencing a great resurgence as vaccines allow the economy to fully reopen. Rising optimism from the commercial construction industry reflects what we’re seeing across the broader economy,” said U.S. Chamber of Commerce Executive Vice President and Chief Policy Officer Neil Bradley. “However, contractors continue to face challenges navigating materials shortages and

Materials Shortages Worsen

Most (84%) contractors say they face at least one material shortage, up from 71% in Q1. One in three (33%) are experiencing a shortage in wood/lumber, and 29% are seeing a shortage of steel. Of those contractors experiencing shortages, 46% say they are having a high impact on projects, up from 20% saying the same in Q1.

Additionally, almost all (94%) contractors say cost fluctuations are having a moderate to high impact on their business, up 12 percentage points from Q1 and up 35 points year-over-year. Wood/lumber and steel are the products of highest concern.

Contractors Face Worker Shortage Crisis

In the midst of a deepening workforce crisis, finding skilled labor continues to be a challenge for contractors. This quarter, 88% report moderate to high levels of difficulty finding skilled workers, of which, nearly half (45%) report a high level of difficulty. Of those who reported difficulty finding skilled labor, over a third (35%) have turned down work because of skilled labor shortages.

Most (87%) contractors also report a moderate to high level of concern about the cost of skilled labor. Of those who expressed concern, 64% say the cost has increased over the past six months, and more than three-quarters (77%) expect it to continue to increase over the next year.

Trade and Tariff Concerns are Up

This quarter, contractors expressed increasing concern about the potential effect of tariffs and trade wars on access to materials over the next three years.

More (45%) say steel and aluminum tariffs will have a high to very-high degree of impact, up from 35% in Q1. Forty percent now say new construction material and equipment tariffs will have a high to very-high degree of impact, up from 29% in Q1. And 30% expect high impacts from trade conflicts with other countries, up from 19% in Q1.

About the Index

The U.S. Chamber of Commerce Commercial Construction Index is a quarterly economic index designed to gauge the outlook for, and resulting confidence in, the commercial construction industry. The Index comprises three leading indicators to gauge confidence in the commercial construction industry, generating a composite Index on the scale of 0 to 100 that serves as an indicator of health of the contractor segment on a quarterly basis.

The Q2 2021 results from the three key drivers are:

— Revenue: Contractors’ revenue expectations over the next 12 months increased to 61 (up four points from Q1).

— New Business Confidence: The overall level of contractor confidence increased to 62 (up three points from Q1).

— Backlog: The ratio of average current to ideal backlog rose three points to 72 (up three points from Q1).

The research was developed with Dodge Data & Analytics (DD&A), the leading provider of insights and data for the construction industry, by surveying commercial and institutional contractors.

Visit www.

Related Stories

Market Data | Aug 13, 2018

First Half 2018 commercial and multifamily construction starts show mixed performance across top metropolitan areas

Gains reported in five of the top ten markets.

Market Data | Aug 10, 2018

Construction material prices inch down in July

Nonresidential construction input prices increased fell 0.3% in July but are up 9.6% year over year.

Market Data | Aug 9, 2018

Projections reveal nonresidential construction spending to grow

AIA releases latest Consensus Construction Forecast.

Market Data | Aug 7, 2018

New supply's impact illustrated in Yardi Matrix national self storage report for July

The metro with the most units under construction and planned as a percent of existing inventory in mid-July was Nashville, Tenn.

Market Data | Aug 3, 2018

U.S. multifamily rents reach new heights in July

Favorable economic conditions produce a sunny summer for the apartment sector.

Market Data | Aug 2, 2018

Nonresidential construction spending dips in June

“The hope is that June’s construction spending setback is merely a statistical aberration,” said ABC Chief Economist Anirban Basu.

Market Data | Aug 1, 2018

U.S. hotel construction pipeline continues moderate growth year-over-year

The hotel construction pipeline has been growing moderately and incrementally each quarter.

Market Data | Jul 30, 2018

Nonresidential fixed investment surges in second quarter

Nonresidential fixed investment represented an especially important element of second quarter strength in the advance estimate.

Market Data | Jul 11, 2018

Construction material prices increase steadily in June

June represents the latest month associated with rapidly rising construction input prices.

Market Data | Jun 26, 2018

Yardi Matrix examines potential regional multifamily supply overload

Outsize development activity in some major metros could increase vacancy rates and stagnate rent growth.