As architecture firms ended 2021 on a high note with strong business conditions, staff recruitment is becoming a growing concern among firms.

December’s Architectural Billings Index (ABI) score of 52.0 was an increase from 51.0 in November (any score over 50 indicates billings growth). Despite a variety of concerns related to the omicron variant, labor shortages, and rising prices as well as limited availability of construction materials, firms continued to report a robust supply of work in the pipeline. Inquiries into new work and the value of new design contracts both remained strong, and backlogs, at an average of 6.5 months, remained near their highest levels since the AIA began tracking this metric in 2010.

“Since demand for design projects has been healthy over the last year, recruiting architectural staff to keep up with project workloads has been a growing concern for firms,” said AIA Chief Economist, Kermit Baker, Hon. AIA, PhD. “Architecture is one of the few industries where payrolls have already surpassed their pre-pandemic high, so meeting future staffing needs is a challenge that most firms will need to confront.

Key ABI highlights for December include:

• Regional averages: South (56.4); Midwest (51.0); West (47.5); Northeast (45.3)

• Sector index breakdown: mixed practice (60.6); multi-family residential (49.2); commercial/industrial (49.2); institutional (47.6)

The regional and sector categories are calculated as a three-month moving average, whereas the national index, design contracts and inquiries are monthly numbers.

Visit AIA’s website for more ABI information.

Related Stories

Engineers | May 3, 2017

At first buoyed by Trump election, U.S. engineers now less optimistic about markets, new survey shows

The first quarter 2017 (Q1/17) of ACEC’s Engineering Business Index (EBI) dipped slightly (0.5 points) to 66.0.

Market Data | May 2, 2017

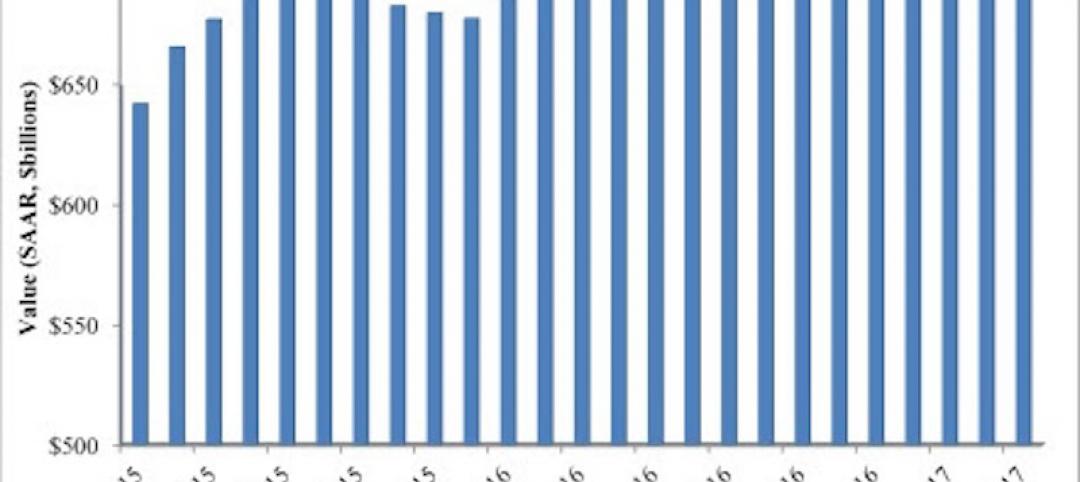

Nonresidential Spending loses steam after strong start to year

Spending in the segment totaled $708.6 billion on a seasonally adjusted, annualized basis.

Market Data | May 1, 2017

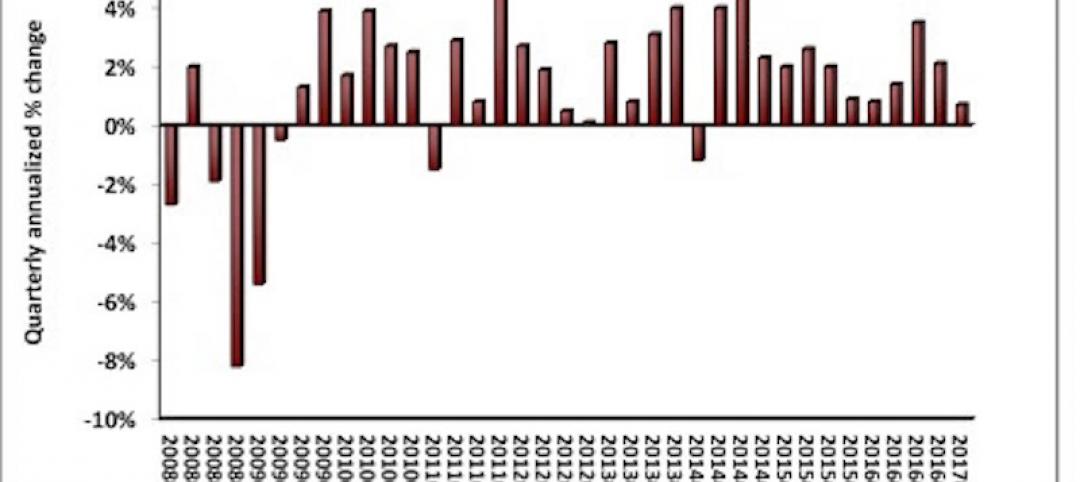

Nonresidential Fixed Investment surges despite sluggish economic in first quarter

Real gross domestic product (GDP) expanded 0.7 percent on a seasonally adjusted annualized rate during the first three months of the year.

Industry Research | Apr 28, 2017

A/E Industry lacks planning, but still spending large on hiring

The average 200-person A/E Firm is spending $200,000 on hiring, and not budgeting at all.

Market Data | Apr 19, 2017

Architecture Billings Index continues to strengthen

Balanced growth results in billings gains in all regions.

Market Data | Apr 13, 2017

2016’s top 10 states for commercial development

Three new states creep into the top 10 while first and second place remain unchanged.

Market Data | Apr 6, 2017

Architecture marketing: 5 tools to measure success

We’ve identified five architecture marketing tools that will help your firm evaluate if it’s on the track to more leads, higher growth, and broader brand visibility.

Market Data | Apr 3, 2017

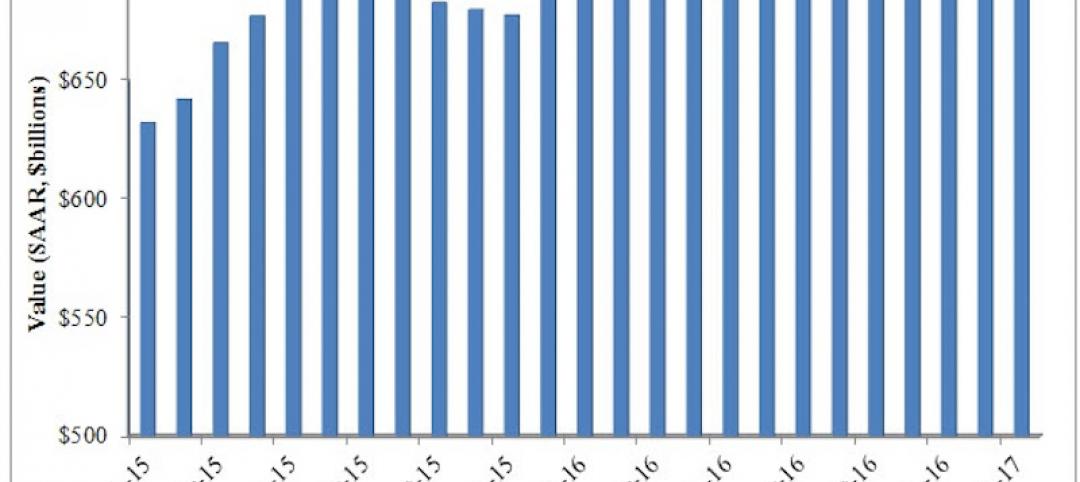

Public nonresidential construction spending rebounds; overall spending unchanged in February

The segment totaled $701.9 billion on a seasonally adjusted annualized rate for the month, marking the seventh consecutive month in which nonresidential spending sat above the $700 billion threshold.

Market Data | Mar 29, 2017

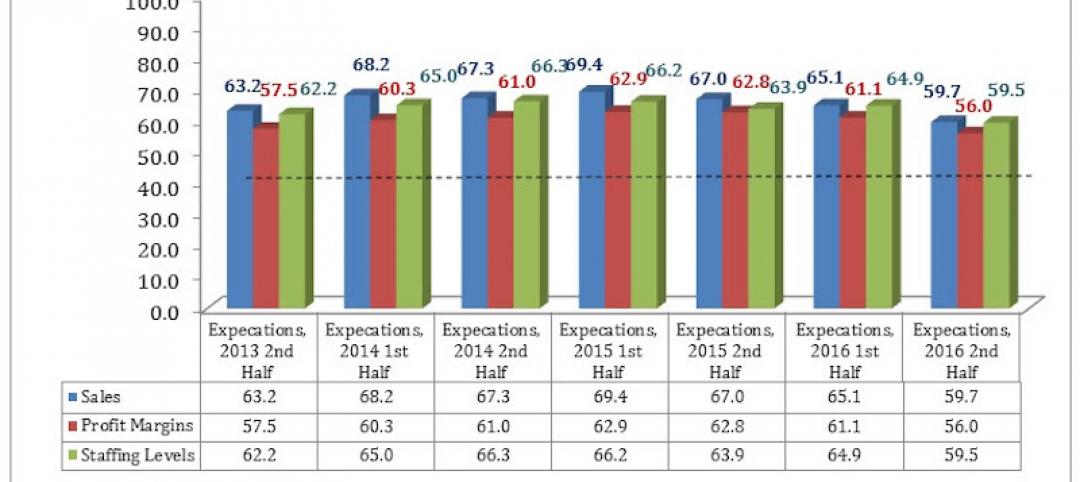

Contractor confidence ends 2016 down but still in positive territory

Although all three diffusion indices in the survey fell by more than five points they remain well above the threshold of 50, which signals that construction activity will continue to be one of the few significant drivers of economic growth.

Market Data | Mar 24, 2017

These are the most and least innovative states for 2017

Connecticut, Virginia, and Maryland are all in the top 10 most innovative states, but none of them were able to claim the number one spot.