The Architecture Billings Index (ABI), produced by the AIA Economics & Market Research Group, is a leading economic indicator that provides an approximately nine- to twelve-month glimpse into the future of nonresidential construction spending activity. The diffusion indexes contained in the full report are derived from a monthly “work-on-the-boards” survey that is sent to a panel of AIA member-owned firms.

Participants are asked whether their billings increased, decreased, or stayed the same in the month that just ended as compared to the prior month, and the results are then compiled into the ABI. These monthly results are also seasonally adjusted to allow for comparison to prior months. The monthly ABI index scores are centered around 50, with scores above 50 indicating an aggregate increase in billings, and scores below 50 indicating a decline.

Following a generally positive performance in 2015, the Architecture Billings Index has begun this year modestly dipping back into negative terrain. The AIA reported the January ABI score was 49.6, down slightly from the mark of 51.3 in the previous month. This score reflects a minor decrease in design services (any score above 50 indicates an increase in billings). The new projects inquiry index was 55.3, down from a reading of 60.5 the previous month.

“The fundamentals are mostly sound in the nonresidential design and construction market,” said AIA Chief Economist, Kermit Baker, Hon. AIA, PhD. “January was a rocky month throughout the economy, with falling oil prices, international economic concerns, and with steep declines in stock market valuations in the U.S. and elsewhere. Some of the fallout of this uncertainty may have affected progress on design projects.”

Key January* ABI highlights:

- Regional averages: West (50.8), Northeast (50.4), South (50.3), Midwest (48.9),

- Sector index breakdown: multifamily residential (51.9), commercial / industrial (50.5), institutional (49.9), mixed practice (49.0)

- Project inquiries index: 55.3

- Design contracts index: 50.9

The regional and sector categories are calculated as a 3-month moving average, whereas the national index, design contracts and inquiries are monthly numbers.

* Every January the AIA research department updates the seasonal factors used to calculate the ABI, resulting in a revision of recent ABI values.

Related Stories

Market Data | May 23, 2018

Architecture firm billings strengthen in April

Firms report solid growth for seven straight months.

Market Data | May 22, 2018

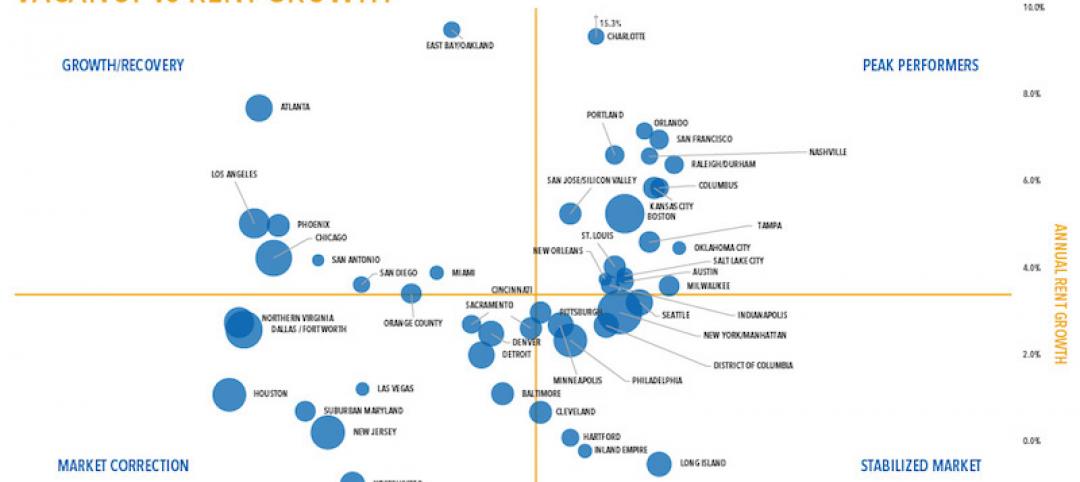

Vacancies stable, rents rising, and pipeline receding, according to Transwestern’s 1Q US Office Market report

The Big Apple still leads the new construction charge.

Market Data | May 18, 2018

Construction employment rises in 38 states and D.C. from April 2017 to April 2018

California & West Virginia have biggest annual job gains, North Dakota has largest decline; California & Louisiana have largest monthly pickup, Indiana & North Dakota lead monthly drops.

High-rise Construction | May 18, 2018

The 100 tallest buildings ever conventionally demolished

The list comes from a recent CTBUH study.

Resiliency | May 17, 2018

Architects brief lawmakers and policy-makers on disaster recovery as hurricane season approaches

Urge senate passage of disaster recovery reform act; Relationship-building with local communities.

Market Data | May 17, 2018

These 25 cities have the highest urban infill development potential

The results stem from a COMMERCIALCafé study.

Market Data | May 10, 2018

Construction costs surge in April as new tariffs and other trade measures lead to significant increases in materials prices

Association officials warn that the new tariffs and resulting price spikes have the potential to undermine benefits of tax and regulatory reform, urge administration to reconsider.

Market Data | May 7, 2018

Construction employers add 17,000 jobs in April and 257,000 for the year

Unemployment rate for construction increases slightly compared to year earlier as higher pay levels appears to be attracting people with recent construction experience back into the workforce.

Market Data | May 2, 2018

Construction employment increases in 245 metro areas between March 2017 & 2018, as trade fights & infrastructure funding shortfalls loom

Houston-The Woodlands-Sugar Land, Texas and Weirton-Steubenville, W.Va.-Ohio experience largest year-over-year gains; Baton Rouge, La. and Auburn-Opelika, Ala. have biggest annual declines.

Market Data | May 2, 2018

Nonresidential Construction down in March, private sector falters, public sector unchanged

February’s spending estimate was revised roughly $10 billion higher.