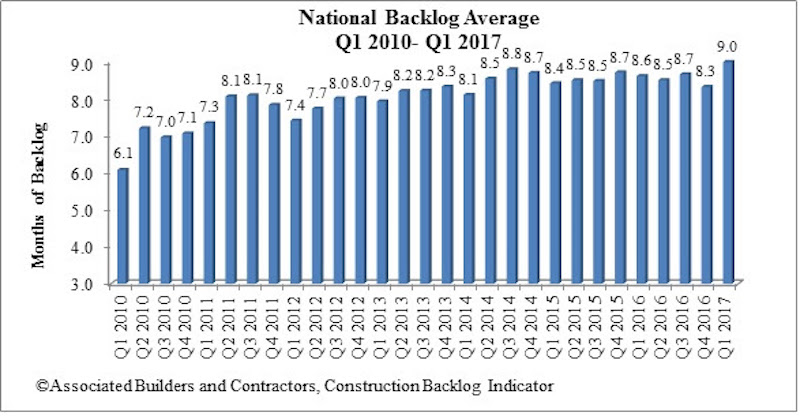

Associated Builders and Contractors (ABC) recently reported that its Construction Backlog Indicator (CBI) rose to 9 months during the first quarter of 2017, up 8.1 percent from the fourth quarter of 2016. CBI is up by 0.4 months, or 4 percent, on a year-over-year basis.

“This was a terrific report,” said ABC Chief Economist Anirban Basu. “For the first time in the series’ history, every category—firm size, industry and region—registered quarterly growth in CBI. Among the big winners were firms in the western United States and those with annual revenues between $30 million and $50 million per annum"

Highlights by Region

- Surging financial markets helped support activity in financial centers like New York, Philadelphia and Boston. Expanding cyber-security and life sciences activity supported markets as geographically diverse as Washington/Baltimore; Austin, Texas; Silicon Valley, Calif., and Seattle.

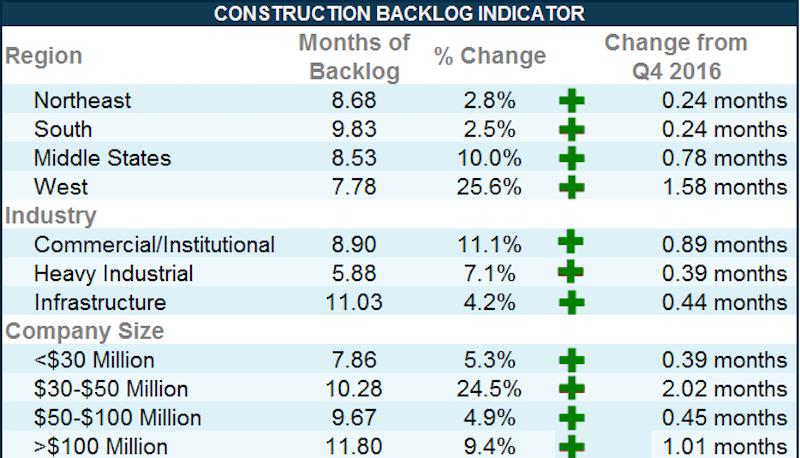

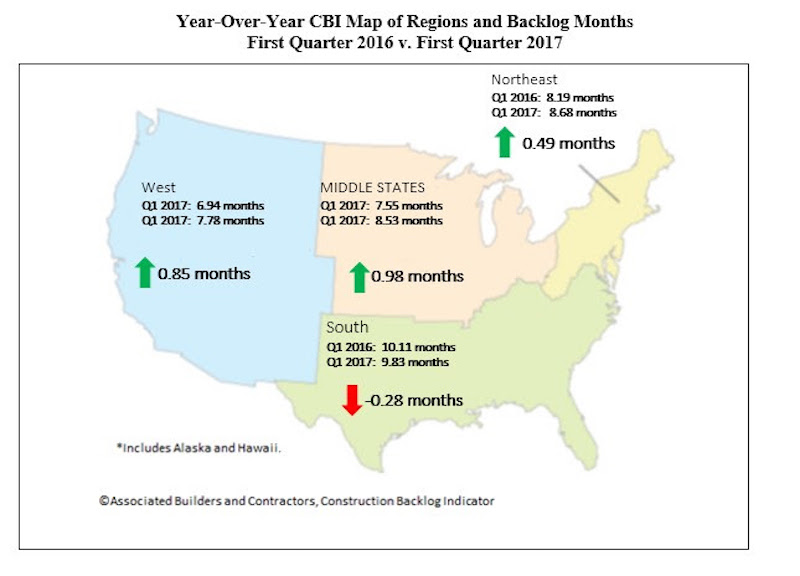

- Though backlog is slightly lower in the South on a year-over-year basis, it continues to report the lengthiest backlog, at 9.8 months. A number of markets remain extraordinarily active with respect to commercial construction, including Atlanta and Miami and Tampa, Fla. Distribution center construction also continues to be active due to a combination of busier seaports and the ongoing online retail boom.

- Backlog in the West was up by a remarkable 26 percent during the quarter. Part of this was due to statistical payback after a surprisingly weak fourth quarter. However, this is also a reflection of the rapid commercial growth in Seattle, Denver, Silicon Valley, San Diego, Phoenix and other population growth hotspots.

- Higher oil and natural gas prices helped to drive CBI higher in the Middle States. Backlog in the region expanded by a more-than-respectable 10 percent during the first quarter, and now stands at a healthy 8.5 months. Chicago continues to be a weak spot, however, registering slow job growth relative to other major U.S. metropolitan areas in recent quarters.

- Backlog in the Northeast rose to 8.7 months during the first quarter. Backlog is up by almost precisely half a month over the past year. The New York and Boston metropolitan areas remain particularly active.

Highlights by Industry

- Backlog in the commercial/institutional segment rose by more than 11 percent during the first quarter, and now stands at nearly 9 months. Backlog also expanded in the heavy industrial and infrastructure categories during the first three months of the year.

- Average backlog in the heavy industrial category rose to 5.88 months, but remains well below levels registered during much of the history of the series. Excluding the fourth quarter of 2016, this represents the lowest reading since the fourth quarter of 2014. There are many forces at work, including slowing auto sales, downward pressure on prices in a number of key manufacturing segments and soft exports.

- Backlog in the infrastructure category expanded during the first quarter and remains above historic levels. Actual infrastructure spending has been unimpressive in many categories recently, including wastewater, water supply, dams/levies and highway/street. Available survey data hint at a bit of a pickup in activity during the quarters ahead.

- Commercial/institutional backlog expanded to 8.9 months, matching its highest level since the third quarter of 2014. Though there are growing concerns regarding overbuilding in a number of metropolitan areas, and retail stores continue to close in large numbers, increases in office and hotel construction are helping to propel this category forward.

Highlights by Company Size

- Backlog for each of the four company size categories increased to start the year. Firms with revenues of $30 million to $50 million, many of which are in the commercial/institutional segments, were the clear outperformers in terms of expanding backlog during the first quarter of 2017. Backlog for this group of firms expanded by more than two months, indicating growing confidence among developers and other purchasers of construction services

- Backlog among firms with annual revenues of less than $30 million increased by 5.3 percent during the quarter. Over the course of time, the nonresidential construction recovery has broadened enough to encompass many of the smallest firms.

- The largest firms, those with annual revenues above $100 million and which are disproportionately represented in the infrastructure category, report the lengthiest backlog at 11.8 months. This was up by more than 9 percent during the quarter. Backlog for this group is approaching the one-year mark, which is considered to be a sign of significant health.

Related Stories

Industry Research | Apr 4, 2024

Expenses per multifamily unit reach $8,950 nationally

Overall expenses per multifamily unit rose to $8,950, a 7.1% increase year-over-year (YOY) as of January 2024, according to an examination of more than 20,000 properties analyzed by Yardi Matrix.

Student Housing | Mar 27, 2024

March student housing preleasing in line with last year

Preleasing is still increasing at a historically fast pace, surpassing 61% in February 2024 and marking a 4.5% increase year-over-year.

K-12 Schools | Mar 18, 2024

New study shows connections between K-12 school modernizations, improved test scores, graduation rates

Conducted by Drexel University in conjunction with Perkins Eastman, the research study reveals K-12 school modernizations significantly impact key educational indicators, including test scores, graduation rates, and enrollment over time.

MFPRO+ News | Mar 16, 2024

Multifamily rents stable heading into spring 2024

National asking multifamily rents posted their first increase in over seven months in February. The average U.S. asking rent rose $1 to $1,713 in February 2024, up 0.6% year-over-year.

MFPRO+ News | Mar 12, 2024

Multifamily housing starts and permitting activity drop 10% year-over-year

The past year saw over 1.4 million new homes added to the national housing inventory. Despite the 4% growth in units, both the number of new homes under construction and the number of permits dropped year-over-year.

Multifamily Housing | Mar 4, 2024

Single-family rentals continue to grow in BTR communities

Single-family rentals are continuing to grow in built-to-rent communities. Both rent and occupancy growth have been strong in recent months while remaining a financially viable option for renters.

MFPRO+ News | Mar 2, 2024

Job gains boost Yardi Matrix National Rent Forecast for 2024

Multifamily asking rents broke the five-month streak of sequential average declines in January, rising 0.07 percent, shows a new special report from Yardi Matrix.

K-12 Schools | Feb 29, 2024

Average age of U.S. school buildings is just under 50 years

The average age of a main instructional school building in the United States is 49 years, according to a survey by the National Center for Education Statistics (NCES). About 38% of schools were built before 1970. Roughly half of the schools surveyed have undergone a major building renovation or addition.

MFPRO+ Research | Feb 28, 2024

New download: BD+C's 2023 Multifamily Amenities report

New research from Building Design+Construction and Multifamily Pro+ highlights the 127 top amenities that developers, property owners, architects, contractors, and builders are providing in today’s apartment, condominium, student housing, and senior living communities.

MFPRO+ Research | Feb 27, 2024

Most competitive rental markets of early 2024

The U.S. rental market in early 2024 is moderately competitive, with apartments taking an average of 41 days to find tenants, according to the latest RentCafe Market Competitivity Report.