In markets where labor continues to be in short supply, contractors that can attract and retain workers are capable of accepting projects that other manpower-deficient competitors might be turning away.

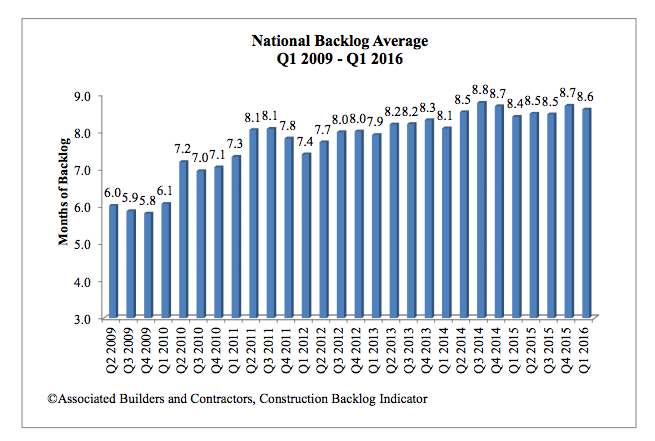

Labor availability is an important distinction in a construction market that “has stabilized at a comfortable level.” The backlog for the nation’s largest contractors stands at a record 12 months, according to the latest estimates from Associated Builders and Contractors (ABC), a national trade association representing 70 chapters with nearly 21,000 members.

The group’s Construction Backlog Indicator, which has measured the national backlog average for every quarter since Q2 2009, stood at 8.6 months, compared to 8.7 months in Q4 2015 and 8.5 months for Q1 2015.

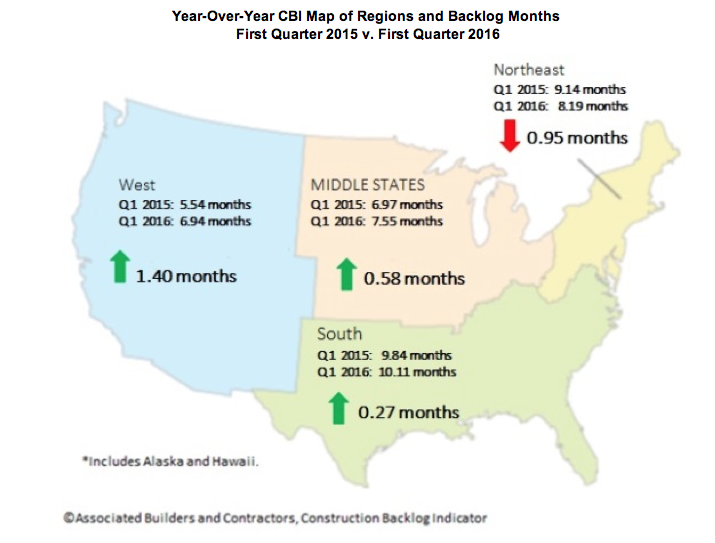

Where contractor backlogs in the Midwest increased by double digit percentages in the latest quarter measured, they fell in the Northeast, South, and West compared to the previous quarter.

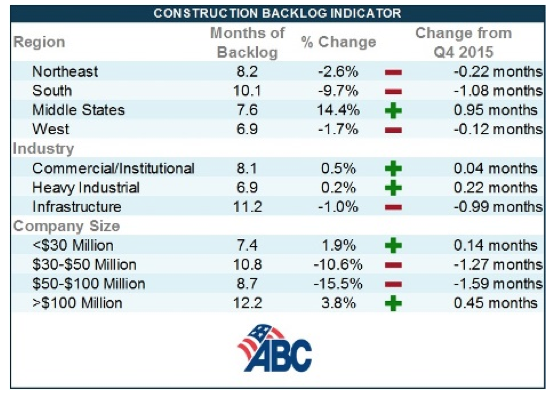

ABC's latest Construction Backlog Index shows that contractors in the Midwest saw the biggest change in their backlogs during the first quarter of this year, as did companies whose revenues range from $50 million to $100 million. Image: Associated Builders and Contractors.

However, contractors in the South have reported average backlogs in excess of 10 months for three consecutive quarters, which is unprecedented in the history of ABC’s series. And while the Northeast isn’t expanding, the region “continues to experience a considerable volume of activity related to commercial development,” including ecommerce fulfillment centers, said ABC.

Backlogs for Commercial/Institutional (which have exceeded eight months for 3½ years), and heavy industrial were up in the most recent quarter tracked, where infrastructure backlogs, while outpacing other sectors at 11.2 months, were down slightly. “The passage of the FAST Act and growing focus among many state and local government policymakers should allow backlog in the infrastructure category to remain elevated,” ABC stated.

Companies with more than $100 million in revenue reported an average 12.25 months of backlog, representing a 3.8% gain over the previous quarter, which itself had set the previous record.

Apparently, the largest firms have recently been taking market share primarily from companies in the $30 million to $100 million range, which reported backlog declines. Companies under $30 million in revenue, on the other hand, enjoyed a modest backlog increase, and have collectively reported backlogs in excess of seven months for 11 consecutive quarters.

“Most contractors continue to express satisfaction regarding the amount of work they have under contract. This is of course truer in certain parts of the nation than others,” said Anirban Basu, ABC’s Chief Economist.

Indeed, backlogs in the West slipped in the latest quarter, even as technology generates “profound levels of activity” in markets like San Jose, Seattle, and San Diego.

ABC's data track a steady increase in national average backlogs dating back to the second quarter of 2009. Image: Associated Builders and Contractors.

Related Stories

K-12 Schools | May 7, 2024

World's first K-12 school to achieve both LEED for Schools Platinum and WELL Platinum

A new K-12 school in Washington, D.C., is the first school in the world to achieve both LEED for Schools Platinum and WELL Platinum, according to its architect, Perkins Eastman. The John Lewis Elementary School is also the first school in the District of Columbia designed to achieve net-zero energy (NZE).

Healthcare Facilities | May 6, 2024

Hospital construction costs for 2024

Data from Gordian breaks down the average cost per square foot for a three-story hospital across 10 U.S. cities.

MFPRO+ Special Reports | May 6, 2024

Top 10 trends in affordable housing

Among affordable housing developers today, there’s one commonality tying projects together: uncertainty. AEC firms share their latest insights and philosophies on the future of affordable housing in BD+C's 2023 Multifamily Annual Report.

Retail Centers | May 3, 2024

Outside Las Vegas, two unused office buildings will be turned into an open-air retail development

In Henderson, Nev., a city roughly 15 miles southeast of Las Vegas, 100,000 sf of unused office space will be turned into an open-air retail development called The Cliff. The $30 million adaptive reuse development will convert the site’s two office buildings into a destination for retail stores, chef-driven restaurants, and community entertainment.

Codes and Standards | May 3, 2024

New York City considering bill to prevent building collapses

The New York City Council is considering a proposed law with the goal of preventing building collapses. The Billingsley Structural Integrity Act is a response to the collapse of 1915 Billingsley Terrace in the Bronx last December.

Student Housing | May 3, 2024

Student housing construction dips in the first quarter of 2024

Investment in college dorms dipped slightly in the first quarter of 2024, but remains higher than a year ago.

Contractors | May 1, 2024

Nonresidential construction spending rises 0.2% in March 2024 to $1.19 trillion

National nonresidential construction spending increased 0.2% in March, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau. On a seasonally adjusted annualized basis, nonresidential spending totaled $1.19 trillion.

K-12 Schools | Apr 30, 2024

Fully electric Oregon elementary school aims for resilience with microgrid design

The River Grove Elementary School in Oregon was designed for net-zero carbon and resiliency to seismic events, storms, and wildfire. The roughly 82,000-sf school in a Portland suburb will feature a microgrid—a small-scale power grid that operates independently from the area’s electric grid.

AEC Tech | Apr 30, 2024

Lack of organizational readiness is biggest hurdle to artificial intelligence adoption

Managers of companies in the industrial sector, including construction, have bought the hype of artificial intelligence (AI) as a transformative technology, but their organizations are not ready to realize its promise, according to research from IFS, a global cloud enterprise software company. An IFS survey of 1,700 senior decision-makers found that 84% of executives anticipate massive organizational benefits from AI.

Codes and Standards | Apr 30, 2024

Updated document details methods of testing fenestration for exterior walls

The Fenestration and Glazing Industry Alliance (FGIA) updated a document serving a recommended practice for determining test methodology for laboratory and field testing of exterior wall systems. The document pertains to products covered by an AAMA standard such as curtain walls, storefronts, window walls, and sloped glazing. AAMA 501-24, Methods of Test for Exterior Walls was last updated in 2015.