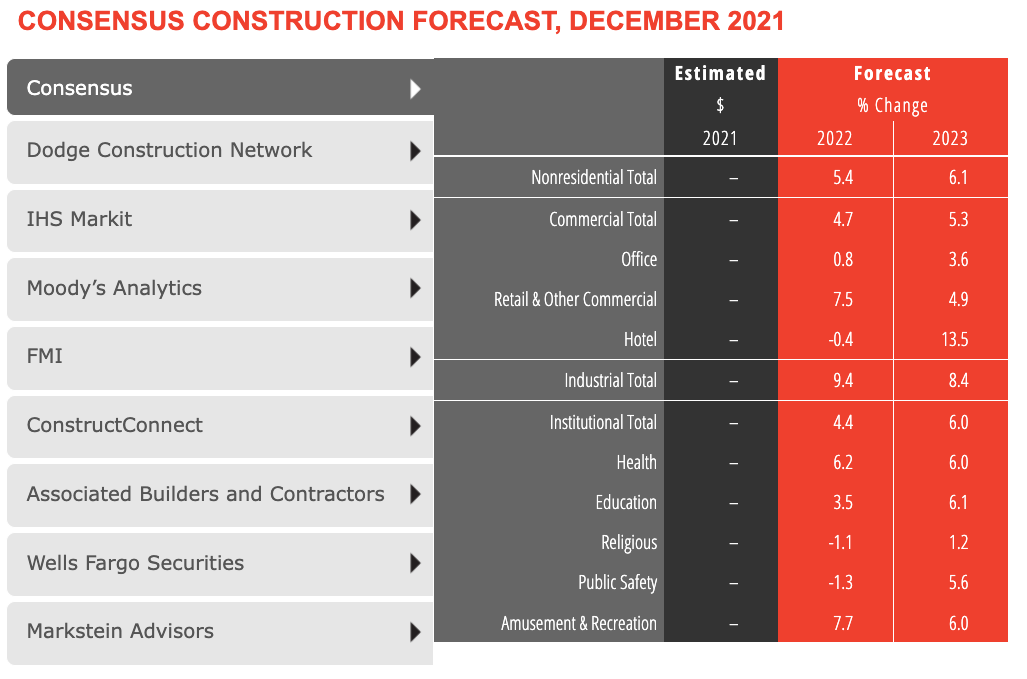

According to a new report from the American Institute of Architects, the nonresidential building sector is expected to see a healthy rebound through next year after failing to recover with the broader economy last year.

The AIA’s Consensus Construction Forecast panel—comprising leading economic forecasters—expects spending on nonresidential building construction to increase by 5.4 percent in 2022, and accelerate to an additional 6.1 percent increase in 2023. With a five percent decline in construction spending on buildings last year, only retail and other commercial, industrial, and health care facilities managed spending increases.

This year, only the hotel, religious, and public safety sectors are expected to continue to decline. By 2023, all the major commercial, industrial, and institutional categories are projected to see at least reasonably healthy gains.

“The pandemic, supply chain disruptions, growing inflation, labor shortages, and the potential passage of all or part of the Build Back Better legislation could have a dramatic impact on the construction sector this year,” said AIA Chief Economist Kermit Baker, Hon. AIA, PhD. “Challenges to the economy and the construction industry notwithstanding, the outlook for the nonresidential building market looks promising for this year and next.”

CLICK HERE TO VIEW INTERACTIVE CHART

More from AIA:

- The recovery in the broader economy in 2021 didn’t carry over to the nonresidential building sector. Spending on the construction of these facilities declined about 5%, on top of the 2% decline in 2020.

- The broader economy has seen a solid recovery since the depths of the pandemic-induced recession. It grew by about 5% last year and now has fully recovered from the past recession. There were almost 4 million net new payroll positions added last year, bringing national employment almost back to the level it was at in February 2020 prior to the pandemic. The national unemployment rate was 3.9% at the end of last year, just above the 3.5% rate in February 2020.

- In spite of these positive economic indicators, there are several headwinds to future economic growth. The uncertainty surrounding combatting Covid and its variants have added tremendous uncertainty to future building needs. The Biden Administration’s Build Back Better program was slated to add significant support to the construction sector, but its funding is very much in doubt at present (January 2022). Supply chain disruptions are likely to continue slow economic growth well into this year. Inflation accelerated during the second half of last year to its highest rate in almost four decades, which is expected to put upward pressure on interest rates. Finally, the already-serious labor shortages look to become even more severe this year and next.

- Industries throughout the economy are finding it challenging to retain their current employees and are having difficulty recruiting new ones. Most workers feel that jobs are plentiful, and therefore are increasingly comfortable leaving their current job in favor of searching for a better one. A recent survey of architecture firm leaders found that more than four in ten feel that recruiting architectural staff is a serious problem at present, and that it may create difficulties for the firm over the coming months given anticipated project workloads.

Related Stories

Market Data | Feb 28, 2017

Leopardo’s 2017 Construction Economics Report shows year-over-year construction spending increase of 4.2%

The pace of growth was slower than in 2015, however.

Market Data | Feb 23, 2017

Entering 2017, architecture billings slip modestly

Despite minor slowdown in overall billings, commercial/ industrial and institutional sectors post strongest gains in over 12 months.

Market Data | Feb 16, 2017

How does your hospital stack up? Grumman/Butkus Associates 2016 Hospital Benchmarking Survey

Report examines electricity, fossil fuel, water/sewer, and carbon footprint.

Market Data | Feb 1, 2017

Nonresidential spending falters slightly to end 2016

Nonresidential spending decreased from $713.1 billion in November to $708.2 billion in December.

Market Data | Jan 31, 2017

AIA foresees nonres building spending increasing, but at a slower pace than in 2016

Expects another double-digit growth year for office construction, but a more modest uptick for health-related building.

High-rise Construction | Jan 23, 2017

Growth spurt: A record-breaking 128 buildings of 200 meters or taller were completed in 2016

This marks the third consecutive record-breaking year for building completions over 200 meters.

Market Data | Jan 18, 2017

Fraud and risk incidents on the rise for construction, engineering, and infrastructure businesses

Seven of the 10 executives in the sector surveyed in the report said their company fell victim to fraud in the past year.

Market Data | Jan 18, 2017

Architecture Billings Index ends year on positive note

Architecture firms close 2016 with the strongest performance of the year.

Market Data | Jan 12, 2017

73% of construction firms plan to expand their payrolls in 2017

However, many firms remain worried about the availability of qualified workers.

Market Data | Jan 9, 2017

Trump market impact prompts surge in optimism for U.S. engineering firm leaders

The boost in firm leader optimism extends across almost the entire engineering marketplace.