According to a new report from the American Institute of Architects, the nonresidential building sector is expected to see a healthy rebound through next year after failing to recover with the broader economy last year.

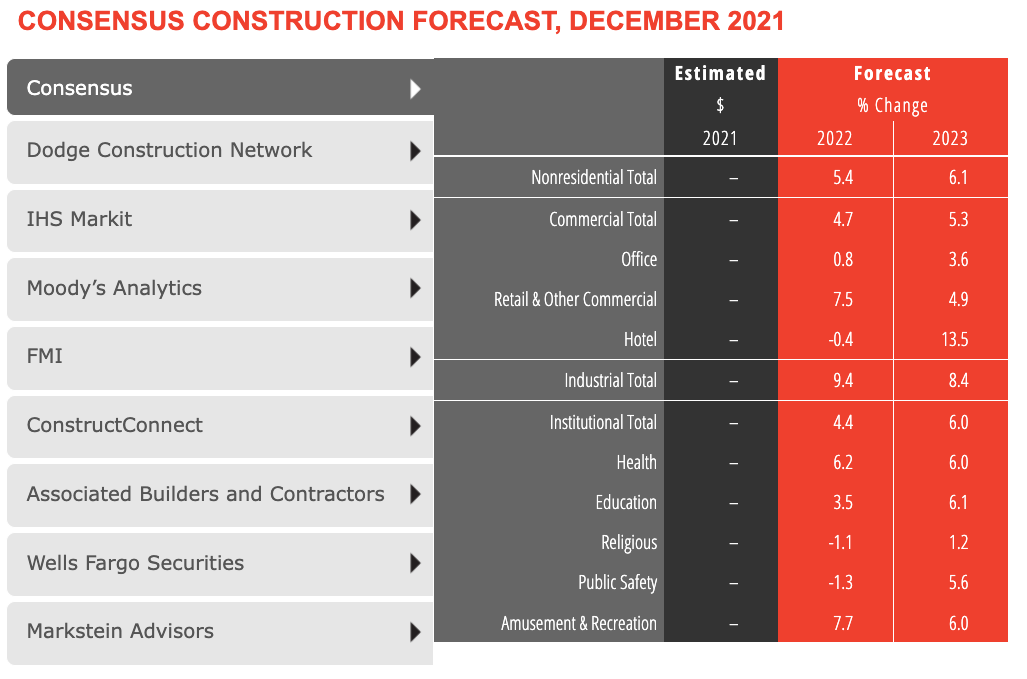

The AIA’s Consensus Construction Forecast panel—comprising leading economic forecasters—expects spending on nonresidential building construction to increase by 5.4 percent in 2022, and accelerate to an additional 6.1 percent increase in 2023. With a five percent decline in construction spending on buildings last year, only retail and other commercial, industrial, and health care facilities managed spending increases.

This year, only the hotel, religious, and public safety sectors are expected to continue to decline. By 2023, all the major commercial, industrial, and institutional categories are projected to see at least reasonably healthy gains.

“The pandemic, supply chain disruptions, growing inflation, labor shortages, and the potential passage of all or part of the Build Back Better legislation could have a dramatic impact on the construction sector this year,” said AIA Chief Economist Kermit Baker, Hon. AIA, PhD. “Challenges to the economy and the construction industry notwithstanding, the outlook for the nonresidential building market looks promising for this year and next.”

CLICK HERE TO VIEW INTERACTIVE CHART

More from AIA:

- The recovery in the broader economy in 2021 didn’t carry over to the nonresidential building sector. Spending on the construction of these facilities declined about 5%, on top of the 2% decline in 2020.

- The broader economy has seen a solid recovery since the depths of the pandemic-induced recession. It grew by about 5% last year and now has fully recovered from the past recession. There were almost 4 million net new payroll positions added last year, bringing national employment almost back to the level it was at in February 2020 prior to the pandemic. The national unemployment rate was 3.9% at the end of last year, just above the 3.5% rate in February 2020.

- In spite of these positive economic indicators, there are several headwinds to future economic growth. The uncertainty surrounding combatting Covid and its variants have added tremendous uncertainty to future building needs. The Biden Administration’s Build Back Better program was slated to add significant support to the construction sector, but its funding is very much in doubt at present (January 2022). Supply chain disruptions are likely to continue slow economic growth well into this year. Inflation accelerated during the second half of last year to its highest rate in almost four decades, which is expected to put upward pressure on interest rates. Finally, the already-serious labor shortages look to become even more severe this year and next.

- Industries throughout the economy are finding it challenging to retain their current employees and are having difficulty recruiting new ones. Most workers feel that jobs are plentiful, and therefore are increasingly comfortable leaving their current job in favor of searching for a better one. A recent survey of architecture firm leaders found that more than four in ten feel that recruiting architectural staff is a serious problem at present, and that it may create difficulties for the firm over the coming months given anticipated project workloads.

Related Stories

Market Data | Nov 30, 2021

Two-thirds of metro areas add construction jobs from October 2020 to October 2021

The pandemic and supply chain woes may limit gains.

Market Data | Nov 22, 2021

Only 16 states and D.C. added construction jobs since the pandemic began

Texas, Wyoming have worst job losses since February 2020, while Utah, South Dakota add the most.

Market Data | Nov 10, 2021

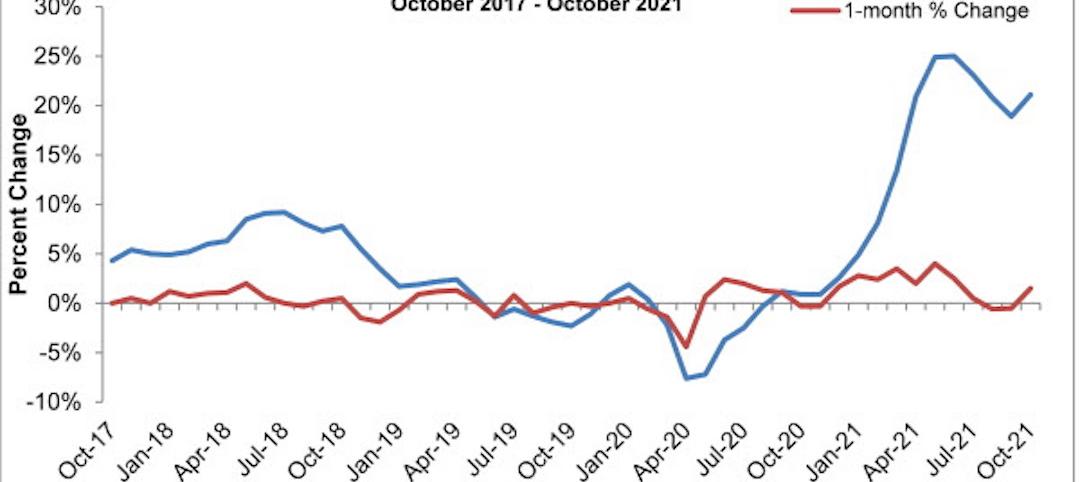

Construction input prices see largest monthly increase since June

Construction input prices are 21.1% higher than in October 2020.

Market Data | Nov 9, 2021

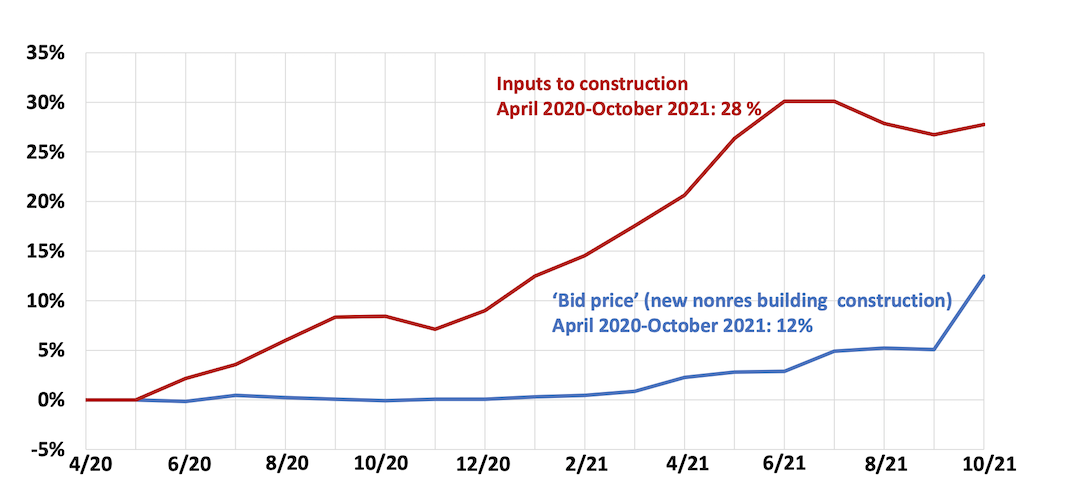

Continued increases in construction materials prices starting to drive up price of construction projects

Supply chain and labor woes continue.

Market Data | Nov 5, 2021

Construction firms add 44,000 jobs in October

Gain occurs even as firms struggle with supply chain challenges.

Market Data | Nov 3, 2021

One-fifth of metro areas lost construction jobs between September 2020 and 2021

Beaumont-Port Arthur, Texas and Sacramento--Roseville--Arden-Arcade Calif. top lists of gainers.

Market Data | Nov 2, 2021

Construction spending slumps in September

A drop in residential work projects adds to ongoing downturn in private and public nonresidential.

Hotel Facilities | Oct 28, 2021

Marriott leads with the largest U.S. hotel construction pipeline at Q3 2021 close

In the third quarter alone, Marriott opened 60 new hotels/7,882 rooms accounting for 30% of all new hotel rooms that opened in the U.S.

Hotel Facilities | Oct 28, 2021

At the end of Q3 2021, Dallas tops the U.S. hotel construction pipeline

The top 25 U.S. markets account for 33% of all pipeline projects and 37% of all rooms in the U.S. hotel construction pipeline.

Market Data | Oct 27, 2021

Only 14 states and D.C. added construction jobs since the pandemic began

Supply problems, lack of infrastructure bill undermine recovery.