Overcapacity in global iron ore production was a major factor in keeping construction costs low through the first four months of 2015. And for the first time in years, subcontractor labor costs showed signs of softening.

Those are two key findings in the latest assessment of current and future pricing from IHS, the Englewood, Colo.-based market analysis firm.

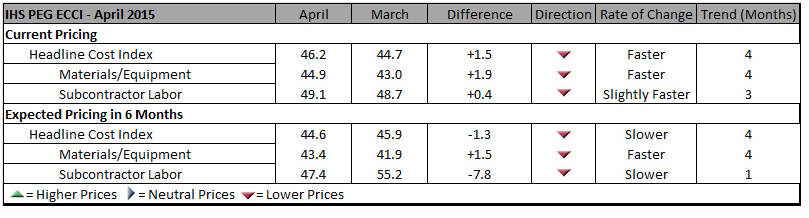

IHS derives its monthly Cost Index from information it receives from member procurement executives working for several of the world’s largest construction and engineering companies, including AECOM and Bechtel. It breaks down those data into current pricing trends and projections for six months forward.

In April, its Cost Index was 46.2, a bit higher than 44.7 in March, but still below what IHS would consider a “neutral” reading. Its sub index for Materials/Equipment costs in April was 44.9 compared to 43.0 in March. And the April sub index for Subcontractor Labor costs stood at 49.1, compared to 48.7 in March.

Procurement execs from some of the world's largest construction and engineering firms report that costs for materials and labor are still falling, and are unlikely to see much inflation for the next six months. Chart: IHS

Procurement execs from some of the world's largest construction and engineering firms report that costs for materials and labor are still falling, and are unlikely to see much inflation for the next six months. Chart: IHS

IHS notes that eight of 12 construction components it tracks registered falling prices in April, led by carbon steel pipe and fabricated structural steel. Both are victims of “bloated capacity, weak profit growth, and lackluster demand,” explains John Anton, IHS’s Director of Steel Services. Iron ore companies that, in response to demand from China’s steel industry, have initiated massive projects whose capacity, so far, “is far ahead of demand,” and is holding prices down.

Anton adds that while the iron ore market may have some ostensible similarities to the recent decline of crude oil prices, what’s different is that iron ore producers have shown no inclinations toward cutting production to match demand. (IHS points out that three quarters of China’s mines are losing money.)

IHS also notes that several global construction and engineering firms, particularly those in the oil and gas sectors, have been taking a “wait and see” approach to investing in larger capital projects. “The capex environment has yet to thaw,” asserts Mark Eisinger, IHS’s senior economist.

While some markets, like the U.S. South, are still experiencing shortages in skilled subcontractor labor, manpower costs have been receding. For the third consecutive month, the U.S. did not register higher month-to-month labor costs in April. And for the first time in this survey’s history, projections about labor costs over the next six months are below the neutral mark. The six-month cost index for subcontractor labor fell to 47.4 in April, compared to 55.2 in March.

The forward-looking index for materials and equipment, at 43.4 April, rose from March’s record low of 41.9, even as 10 of 12 components showed falling price expectations.

Related Stories

Giants 400 | Nov 9, 2022

Top 50 Data Center Contractors + CM Firms for 2022

Holder, Turner, DPR, and HITT Contracting head the ranking of the nation's largest data center contractors and construction management (CM) firms for 2022, as reported in Building Design+Construction's 2022 Giants 400 Report.

Giants 400 | Nov 8, 2022

Top 110 Sports Facility Architecture and AE Firms for 2022

Populous, HOK, Gensler, and Perkins and Will top the ranking of the nation's largest sports facility architecture and architecture/engineering (AE) firms for 2022, as reported in Building Design+Construction's 2022 Giants 400 Report.

Giants 400 | Nov 8, 2022

Top 60 Sports Facility Contractors and CM Firms for 2022

AECOM, Mortenson, Clark Group, and Turner Construction top the ranking of the nation's largest sports facility contractors and construction management (CM) firms for 2022, as reported in Building Design+Construction's 2022 Giants 400 Report.

Industry Research | Nov 8, 2022

U.S. metros take the lead in decarbonizing their built environments

A new JLL report evaluates the goals and actions of 18 cities.

Hotel Facilities | Nov 8, 2022

6 hotel design trends for 2022-2023

Personalization of the hotel guest experience shapes new construction and renovation, say architects and construction experts in this sector.

Green | Nov 8, 2022

USGBC and IWBI will develop dual certification pathways for LEED and WELL

The U.S. Green Building Council (USGBC) and the International WELL Building Institute (IWBI) will expand their strategic partnership to develop dual certification pathways for LEED and WELL.

Reconstruction & Renovation | Nov 8, 2022

Renovation work outpaces new construction for first time in two decades

Renovations of older buildings in U.S. cities recently hit a record high as reflected in architecture firm billings, according to the American Institute of Architects (AIA).

Sponsored | Steel Buildings | Nov 7, 2022

Steel structures offer faster path to climate benefits

Faster delivery of buildings isn’t always associated with sustainability benefits or long-term value, but things are changing. An instructive case is in the development of steel structures that not only allow speedier erection times, but also can reduce embodied carbon and create durable, highly resilient building approaches.

Building Team | Nov 7, 2022

U.S. commercial buildings decreased energy use intensity from 2012 to 2018

The recently released 2018 Commercial Buildings Energy Consumption Survey (CBECS) by the U.S. Energy Information Administration found that the total floorspace in commercial buildings has increased but energy consumption has not, compared with the last survey analyzing the landscape in 2012.

Sports and Recreational Facilities | Nov 7, 2022

Gilbane, Turner, Populous tapped to design and build new Buffalo Bills stadium

The joint venture of Gilbane Building Company and Turner Construction Company, in association with 34 Group, has been selected to provide construction management of the planned new NFL stadium for the Buffalo Bills in Orchard Park, N.Y. The project team also includes the project management firm, Legends Project Development, and Populous as the designer.