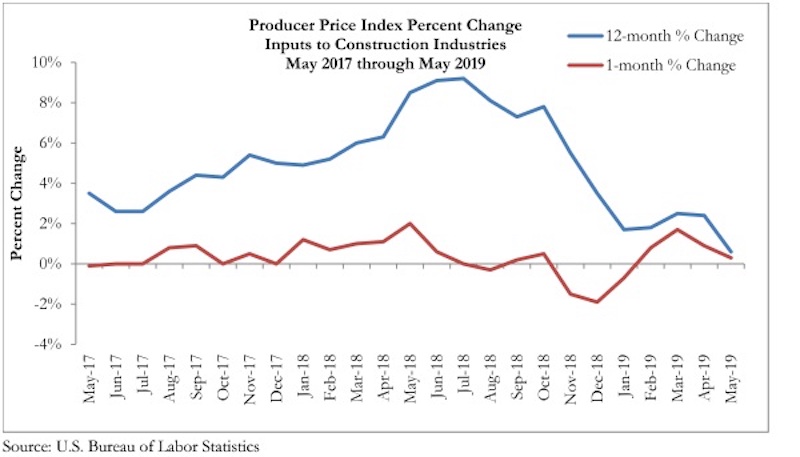

Construction input prices rose slightly by 0.3% in May on a monthly basis and are up 0.6% over the last 12 months, according to an Associated Builders and Contractors analysis of U.S. Bureau of Labor Statistics data released today. Nonresidential input prices were also up 0.3% compared to the previous month and are 1.1% higher than they were a year ago.

Among the 11 subcategories, six saw prices fall last month, with the largest decreases in natural gas (-15.2%), unprocessed energy materials (-8.2%) and crude petroleum (-6.2%). Of the remaining five subcategories, only two experienced price increases greater than 1%: nonferrous wire and cable (+1.2%) and prepared asphalt, tar roofing and siding products (+1.1%), which also had the largest year-over-year price increase at 6.3%.

“Based on a variety of factors, materials prices should be escalating in the United States, yet nonresidential construction materials prices remain relatively stable,” said ABC Chief Economist Anirban Basu. “First, demand for materials remains high in the context of ongoing growth in nonresidential construction spending. This is especially true for a number of construction material intensive segments like highway and street. Indeed, prepared asphalt is the only category of construction materials that this report monitors that experienced a price increase exceeding 6% over the past year.

“Second, there is the issue of tariffs, including those that have impacted steel and aluminum prices in recent months,” said Basu. “Despite those surcharges on imported goods, no related categories are associated with significant inflationary pressure, though the price of fabricated steel products is up by a somewhat-above-average 2.8% over the past year. Third, there have been active attempts by certain groups of suppliers, including OPEC members, to truncate supply in an effort to raise prices. In large measure, those efforts have failed, with a host of commodity prices, including oil prices, declining recently.

“There are many factors that have helped to limit materials price increases, including a weakening global economy and the emergence of goods-producing nations like Vietnam and Indonesia,” said Basu. "A strong U.S. dollar has also helped to limit the commodity price increases encountered by America’s construction firms.

“For contractors, this comes as good news,” said Basu. “While U.S. construction firms will continue to wrestle with rising compensation costs, materials prices are likely to remain well behaved over the near term. There is little evidence that the global economy is reaccelerating. Moreover, the Trump administration recently removed tariffs on steel and aluminum with respect to Canada and Mexico. Finally, while public construction spending growth has been robust of late, there is some evidence that spending growth has become less intense in a number of private construction segments, which would have the effect of limiting demand for certain materials, all things being equal.”

Related Stories

Giants 400 | Sep 5, 2023

Top 80 Construction Management Firms for 2023

Alfa Tech, CBRE Group, Skyline Construction, Hill International, and JLL top the rankings of the nation's largest construction management (as agent) and program/project management firms for nonresidential buildings and multifamily housing work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Sep 5, 2023

Top 150 Contractors for 2023

Turner Construction, STO Building Group, DPR Construction, Whiting-Turner Contracting Co., and Clark Group head the ranking of the nation's largest general contractors, CM at risk firms, and design-builders for nonresidential buildings and multifamily buildings work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Market Data | Sep 5, 2023

Nonresidential construction spending increased 0.1% in July 2023

National nonresidential construction spending grew 0.1% in July, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau. On a seasonally adjusted annualized basis, nonresidential spending totaled $1.08 trillion and is up 16.5% year over year.

Giants 400 | Aug 31, 2023

Top 35 Engineering Architecture Firms for 2023

Jacobs, AECOM, Alfa Tech, Burns & McDonnell, and Ramboll top the rankings of the nation's largest engineering architecture (EA) firms for nonresidential buildings and multifamily buildings work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Aug 22, 2023

Top 115 Architecture Engineering Firms for 2023

Stantec, HDR, Page, HOK, and Arcadis North America top the rankings of the nation's largest architecture engineering (AE) firms for nonresidential building and multifamily housing work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Aug 22, 2023

2023 Giants 400 Report: Ranking the nation's largest architecture, engineering, and construction firms

A record 552 AEC firms submitted data for BD+C's 2023 Giants 400 Report. The final report includes 137 rankings across 25 building sectors and specialty categories.

Giants 400 | Aug 22, 2023

Top 175 Architecture Firms for 2023

Gensler, HKS, Perkins&Will, Corgan, and Perkins Eastman top the rankings of the nation's largest architecture firms for nonresidential building and multifamily housing work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Apartments | Aug 22, 2023

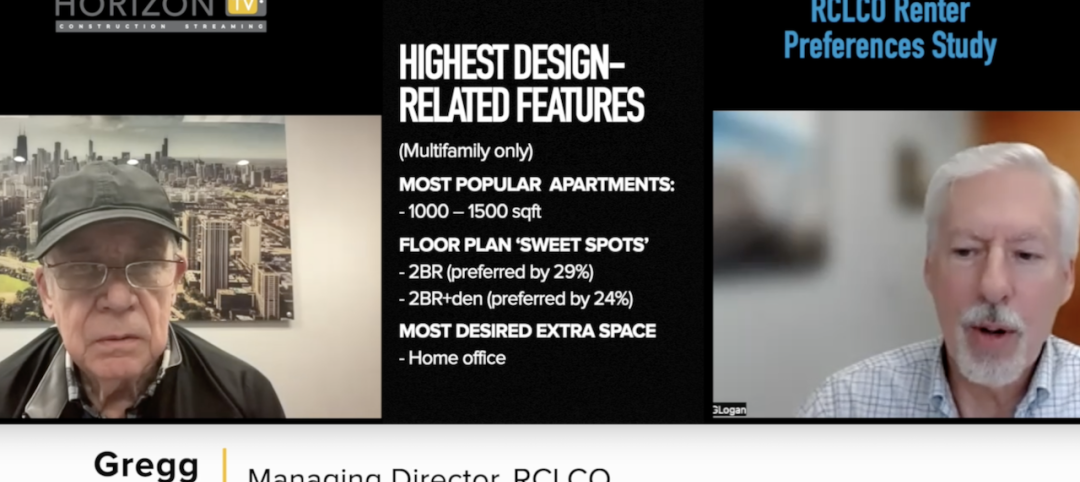

Key takeaways from RCLCO's 2023 apartment renter preferences study

Gregg Logan, Managing Director of real estate consulting firm RCLCO, reveals the highlights of RCLCO's new research study, “2023 Rental Consumer Preferences Report.” Logan speaks with BD+C's Robert Cassidy.

Market Data | Aug 18, 2023

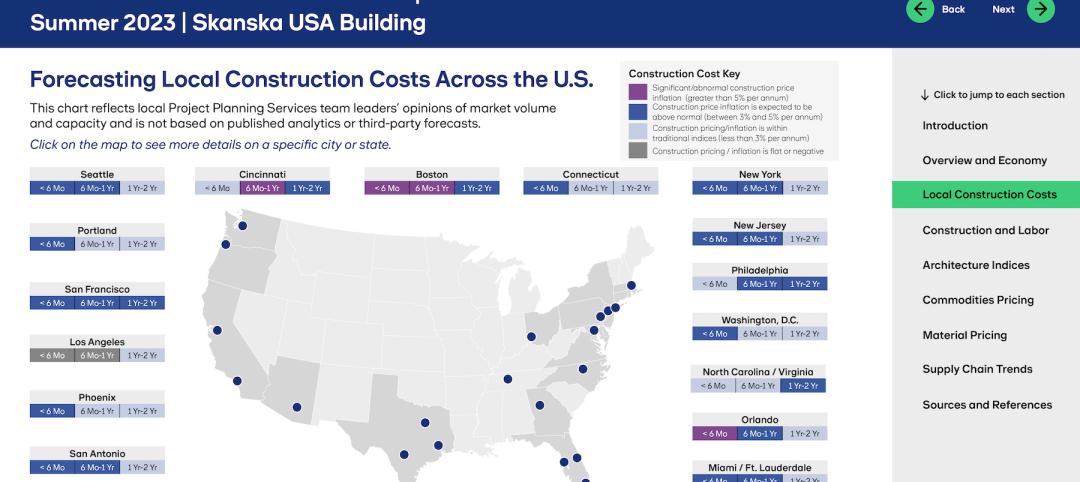

Construction soldiers on, despite rising materials and labor costs

Quarterly analyses from Skanska, Mortenson, and Gordian show nonresidential building still subject to materials and labor volatility, and regional disparities.

Apartments | Aug 14, 2023

Yardi Matrix updates near-term multifamily supply forecast

The multifamily housing supply could increase by up to nearly 7% by the end of 2023, states the latest Multifamily Supply Forecast from Yardi Matrix.