The Southeast and Texas offer the most favorable conditions for commercial construction, claiming seven of the top 10 markets in CBRE’s inaugural Development Opportunity Index. CBRE’s Index analyzes a spectrum of variables in the 50 largest U.S. markets to determine rate the highest for development opportunities across various asset classes.

U.S. construction activity is expected to bounce back in 2021, after a slowdown in 2020 due to challenges brought by COVID-19, including temporary work stoppages and difficulty sourcing various materials from abroad. Since the start of the pandemic, momentum has varied across commercial real estate sectors – development largely progressed in the multifamily and industrial & logistics sectors, but activity slowed—and in some cases stalled—for retail, hotels and speculative office development.

“We expect to see an uptick tenant fit-out projects in 2021 as employers redesign and reconfigure spaces to accommodate new standards in health, wellness and safety,” said Jim Dobleske, CBRE Global President of Project Management. “Costs, however, aren’t likely to change much; markets with high costs of land and labor won’t get much cheaper, if at all.”

CBRE’s Development Opportunity Index ranks markets based on development conditions including property performance across each of the major commercial real estate asset classes, construction costs, strength of supply, prior and forecast performance.

“Southern states continue to rate highly for development and construction conditions, though investors looking for development opportunities can find them in every market,” said James Millon, a Vice Chairman in CBRE’s Debt & Structured Finance practice. “Southern states often have job growth, in-migration and cost advantages that drive high volumes of construction activity.”

An overall top-10 ranking doesn’t necessarily mean that market is among the best for every asset class.

For example, CBRE’s analysts ranked San Jose as the best positioned market for office construction due to its supply growth and strong absorption. Phoenix – reflecting its shrinking vacancy and strong absorption -- and San Francisco – with strong rent growth – also are attractive office markets for development.

For industrial & logistics construction, Atlanta ranks highest due to its balance of strong inventory growth and net absorption. Also ranking well are Phoenix because of its affordable land and labor, and Dallas due to its relatively low costs and strong population growth.

Houston tops the index of ideal markets for retail construction due to that market’s strong consumer spending and sustained absorption of retail space. Next are Dallas and Atlanta, which both offer stable costs and good absorption of retail space.

For multifamily construction, the top markets are Orlando, Phoenix and Denver. Each offers strong population growth, job gains and relatively low costs.

To download the report, click here.

Related Stories

Market Data | Sep 22, 2016

Architecture Billings Index slips, overall outlook remains positive

Business conditions are slumping in the Northeast.

Market Data | Sep 20, 2016

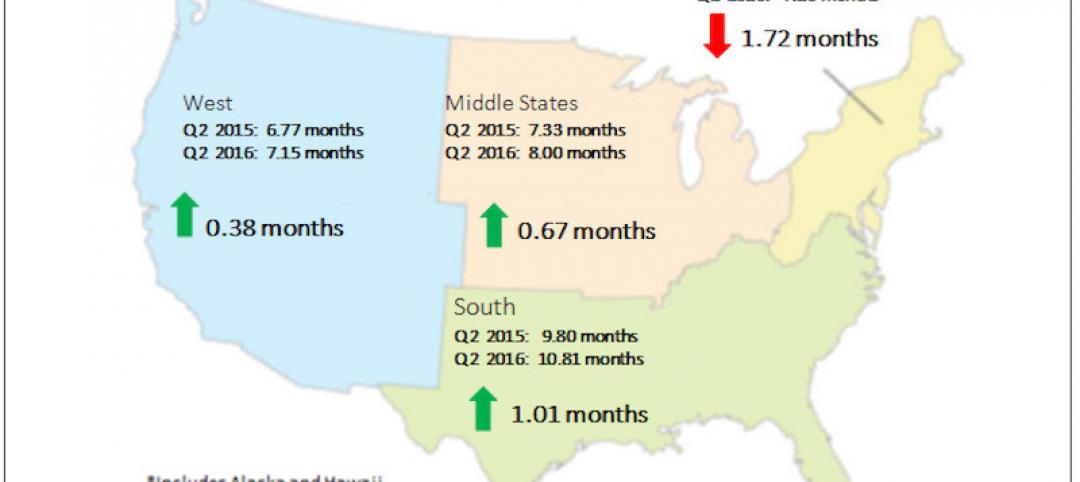

Backlog skyrockets for largest firms during second quarter, but falls to 8.5 months overall

While a handful of commercial construction segments continue to be associated with expanding volumes, for the most part, the average contractor is no longer getting busier, says ABC Chief Economist Anirban Basu.

Designers | Sep 13, 2016

5 trends propelling a new era of food halls

Food halls have not only become an economical solution for restauranteurs and chefs experiencing skyrocketing retail prices and rents in large cities, but they also tap into our increased interest in gourmet locally sourced food, writes Gensler's Toshi Kasai.

Building Team | Sep 6, 2016

Letting your resource take center stage: A guide to thoughtful site selection for interpretive centers

Thoughtful site selection is never about one factor, but rather a confluence of several components that ultimately present trade-offs for the owner.

Market Data | Sep 2, 2016

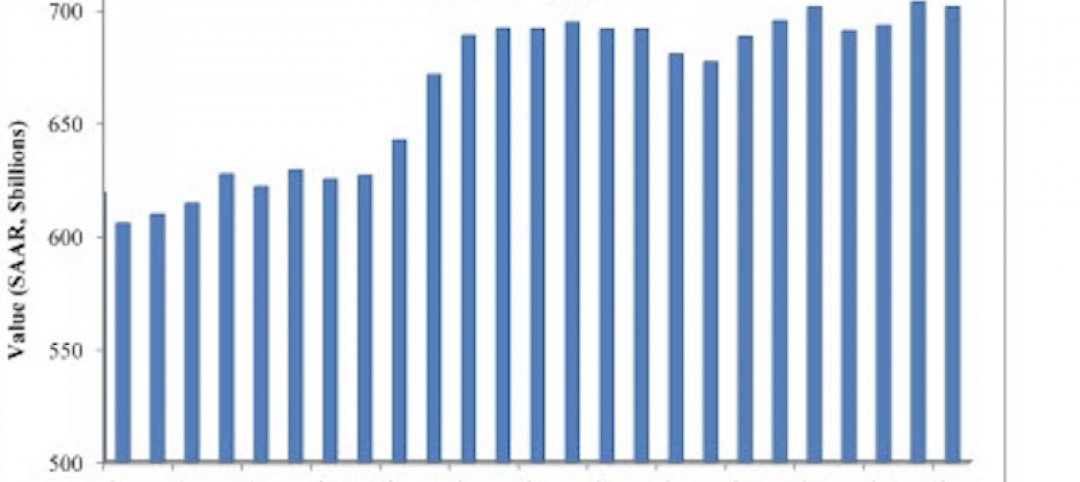

Nonresidential spending inches lower in July while June data is upwardly revised to eight-year record

Nonresidential construction spending has been suppressed over the last year or so with the primary factor being the lack of momentum in public spending.

Industry Research | Sep 1, 2016

CannonDesign releases infographic to better help universities obtain more R&D funding

CannonDesign releases infographic to better help universities obtain more R&D funding.

Industry Research | Aug 25, 2016

Building bonds: The role of 'trusted advisor' is earned not acquired

A trusted advisor acts as a guiding partner over the full course of a professional relationship.

Multifamily Housing | Aug 17, 2016

A new research platform launches for a data-deprived multifamily sector

The list of leading developers, owners, and property managers that are funding the NMHC Research Foundation speaks to the information gap it hopes to fill.

Hotel Facilities | Aug 17, 2016

Hotel construction continues to flourish in major cities

But concerns about overbuilding persist.

Market Data | Aug 16, 2016

Leading economists predict construction industry growth through 2017

The Chief Economists for ABC, AIA, and NAHB all see the construction industry continuing to expand over the next year and a half.