Construction Cost Insights and Industry Trends for Q1 2026

Key Highlights

- The costs of many core construction materials, including lumber and steel, slipped from Q4 2025 to Q1 2026.

- Zooming out, many year-over-year non-metal material costs are up, notably insulation, which has surged over 19% in that span.

- Labor costs comprise a higher portion of total construction costs than they have in four years but are still under pre-COVID levels.

Every quarter, Gordian lends its RSMeans Data construction costs and expert analysis to the Construction Cost Insights Report. Produced in partnership with Building Design+Construction, each report dives deep into the latest material cost movements and includes insider discussions of prevailing construction trends, straight from industry leaders. Packed with useful data, each report marries the macro with the micro, so readers can see what’s happening in their cities and place their experiences within the broader context of North American construction.

Given the recent publication of the Construction Cost Insights Report for Q1 2026, now is an appropriate time to highlight three points of interest worth keeping tabs on for the rest of the year.

The Movement of Core Materials

As it concerns the most prominent construction materials, 2025 was a mixed bag. Structural steel was largely stable, though it should be noted the costs started 2026 in a mild slump. That drop, however, is not precipitous enough to inspire a drastic response.

Raw copper prices, on the other hand, fluctuated throughout 2025, including a leap of nearly 20% from July to December, a spike attributed to supply interruptions among the world’s copper-producing countries. By later this year, copper cost increases will impact everyone — suppliers, contractors and consumers.

Lumber costs rose moderately between 2025 and 2026, including a modest dip to start this year. Around this time last year, costs bumped up due to shifts in demand, changes to trade policy and mill closures. However, demand has cooled and the supply of lumber is now outpacing demand. If demand shifts again, it is unlikely that production rate will have the power to keep pace. At least not without creating price volatility.

The Wild State of Non-Metals

We need to talk about what is going on with non-metals. It has been a ride. Take insulation as an example.

The costs of raw materials such as fiberglass have been on the rise for over a year, which has, in turn, created higher manufacturing costs. To start 2026, year-over-year insulation costs are up over 19%. That’s a massive increase. Here’s the good news: It does not appear likely that these manufacturing costs will increase any further, signaling that insulation costs will hold steady.

This is not an isolated experience. Concrete and earthwork costs are seeing double digit increases across all regions of North America.

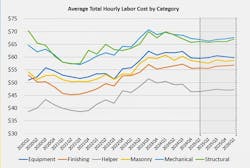

Labor as a Cost Driver

We’ve been discussing a construction labor shortage for so long that it’s difficult to remember when construction labor was plentiful. Wages have been steadily increasing since the days of the pandemic. As it stands, labor accounts for 34.9% of total construction costs. That’s the highest fraction in four years, but still lower than it was pre-COVID.

For more insights like these, plus current cost movements in your area, access our Construction Cost Insights Resource Hub.

About the Author

Adam Raimond, Program Manager, Gordian

Adam Raimond is a program manager at Gordian, overseeing the production of RSMeans Cost Indices, labor rate, equipment, and predictive cost products. He has spent the last eight years helping build data solutions and estimates for construction costs.