Life Sciences overshoots its expansion runway

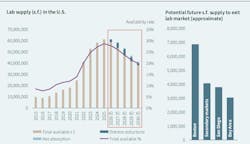

The creation of new lab space has slowed to a crawl, following aggressive building that, over the past four years, has tripled the space available for leasing in the U.S. to 61 million sf. Except for some submarkets, developers and owners should expect a long road to recovery in the lab sector’s demand.

In its report, “2025 Life Sciences Real Estate Perspective and Cluster Analysis,” released this month, JLL talks through the short-term market dynamics across the U.S., and highlights themes that could structurally change the way real estate is needed going forward.

JLL cites three key trends that are affecting market conditions:

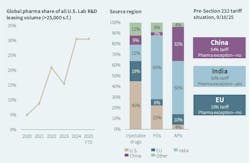

•The imposition of tariffs on pharmaceuticals with no U.S. manufacturing input has global providers reassessing their portfolios and optimizing their intellectual properties. Meanwhile, to date large pharma’s commitment to U.S.-based manufacturing exceeds $475 billion.

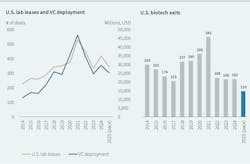

•There will continue to be a direct correlation between venture capital investments in science and startups, and lab leasing. And right now, “biotech remains out of favor in the venture community,” as AI venture investment crowds out other sectors, wrote JLL. Space demand shifts with the investment tides.

•The vacancy rate for lab buildings has gone from 6.6% in 2022 to 27% in 2025. Labs delivered from 2022 to 2024 carry a 48% vacancy rate, with 223 lab buildings fully vacant at the time of this report’s release. During this period, a new “tough tech” or “deep tech” tenant group has emerged. This group creates a potential new demand pool, but it is also cost conscious. “We’ve already seen 13 buildings pivot to or lease to other uses while we wait for demand to recover, with many more expected to follow suit,” wrote JLL.

China all in on biotech growth

The future trends that JLL looks at are already manifesting themselves. For example, AI-native biotechs have accounted for one-sixth of all biotech VC deals year-to-date. The physical space these companies need is beginning to show a departure from traditional biotechs in terms of lower lab-to-office ratios. On a per-employee basis, AI biotechs are leasing roughly one-third less space than traditional-sector benchmarks. Labs like these are allocating more space to compute power, robots, and sensors. And new technologies will drive reconsiderations of planning for leased space, as will lab automation, wrote JLL.

Another disruptive factor has been the rise in biomedical research in China. Chinese biotechs have accounted for four times the in-leasing deals for U.S. biopharma in 2025 as they did in 2021. Risk capital is now flowing eastward, further placing stress on U.S. tenants and weakening domestic demand.

Of the 205 million sf of total lab space in the U.S., 61 million sf is on the market available to lease. To return to a neutral leverage market, JLL estimates that 30 million sf must either be absorbed or leave the inventory pool entirely either by demolition or adaptive reuse. Using historic absorption rates as a guide, JLL estimates that it could take seven years to achieve equilibrium.

Across the U.S., JLL predicted that around 18.7 million sf of available space will likely shift uses by 2030, due to distress or otherwise. That scale of supply disruption coupled with below-average absorption would reduce the availability rate from 29% to 20% by 2030. “Unless demand materially changes for the better, it is unlikely the lab market returns to equilibrium by 2030 anywhere but in core markets,” JLL stated.

Ranking the top markets

Los Angeles, for example, breaks into JLL’s top five talent hubs, based on its employment base, emerging workforce, educational pipeline, and fundamentals like real estate availability. The Bay Area is No. 1 for its startup ecosystem with the highest venture capital deployment across AI/machine language, healthcare devices, and core biopharma sectors. The Bay Area also leads in its medical technology workforce expansion.

New Jersey is JLL’s top biomanufacturing hub, with the largest concentration of related professionals and contract development and manufacturing organization (CDMO) facilities.

JLL’s report also provides more detailed metrics on the Top 10 U.S. Life Sciences Hubs, including total and leasable inventory, rents, construction pipeline, and year-over-year absorption rate. Boston, for example, has 51.7 million sf of inventory, of which 33% is available for lease. Its Triple Net rent averages $81.45. It has 3.3 million sf of lab space in its pipeline, and its absorption rate is a negative 600,000 sf.

The report offers similar measurements for Canada’s four most-populous markets, and for five Latin American countries: Puerto Rico, Mexico, Brazil, Costa Rica, and Argentina.

About the Author

John Caulfield

John Caulfield is Senior Editor with Building Design + Construction Magazine.