Public institutions are embracing P3 delivery model

Key takeaways from JLL’s report on P3s:

•Financial uncertainty driving creative solutions

•Housing remains a strategic priority

•Expanding asset class diversification

•Record growth in transaction volume

•Macroeconomic factors accelerating adoption

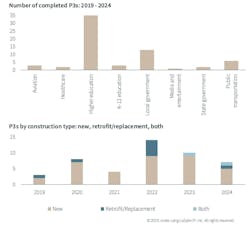

There was a notable acceleration in the implementation of public-private partnerships for building projects between 2022 and 2024. Forty-one social infrastructure P3s closed within that timeframe, more than double the 17 contracts signed during the previous three years.

The market research firm Jones Lang LaSalle (JLL) analyzed those 58 facility-focused transactions from 2019 to 2024 to gain insight about sector-specific trends. Its latest report, “Redefining Public Delivery One P3 at a Time,” released this month, finds that more public institutions are embracing P3s as flexible delivery structures that address critical housing needs while preserving strategic control over long-term planning. These partnerships have evolved to feature increasingly sophisticated risk-sharing arrangements requiring creative financial engineering to remain viable in today’s complex market.

In fact, many of the P3s that reached financial closure over the past year alone—during relatively high interest rates—were ones where the public sector entity took on more risk or provided guarantees for the project. This represents a stark contrast from the previous era of historically low interest rates, when financing P3 projects was easier because the private cost of capital was much closer to public borrowing rates.

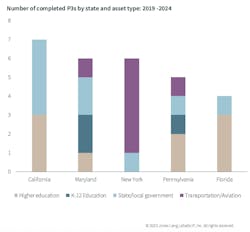

Higher Ed is P3 wheelhouse

Although public-private partnerships are done across the country, California, Maryland, New York, Pennsylvania and Florida lead the way in P3 deals completed since 2019. These states, which represent four of the five most populous states in the United States, demonstrate a strong correlation between population size and P3 engagement.

Asset types attracting the most investment vary by state, with higher education and state/local government projects dominating in California, while transportation and aviation initiatives take precedence in New York. Maryland, although the 19th most populated state, saw the second highest amount of completed P3s thanks to supportive legislation frameworks that foster partnerships with an emphasis on K-12 school districts and state/local governments as the primary procuring authorities in the state.

Higher education institutions, in fact, stand as particularly active adopters, accounting for over 50% of P3 projects since 2019, with new construction dominating 80% of implementations rather than renovations.

Purdue University’s housing initiative for its Fort Wayne, Ind., campus exemplifies strategic P3 implementation in practice. Facing enrollment growth that strained capacity, the university engaged JLL to guide the process from planning and demand assessment through financial close. The $82.3 million project delivers 602 new apartment-style beds through a tax-exempt 501c3 model, increasing affordable housing access while supporting the campus's transition from commuter to residential. The structuring of a 49% master lease helped achieve both financial sustainability and mission advancement.

Since 2019, 32 colleges and universities have completed projects through P3s, with 26 of those being done at public four-year institutions. The 26 public four-year institutions that completed P3 projects between 2019 and 2024 experienced an average 7% enrollment growth—contrasting with a national average decline of 1.3% across similar institutions during the same period.

P3s lead to growth

Local government agencies and public transportation authorities represent the next most active sectors to use P3 delivery, with increasingly specialized uses including media, entertainment, and healthcare beginning to explore the model. Out of the 13 completed P3s that were procured by local governments from 2019-2024, 10 were in markets that have experienced population growth since 2015.

Many municipalities that have procured and completed P3s are situated on the outskirts of expanding metropolitan areas. San Marcos and Pflugerville, both of which are rapidly growing suburbs of Austin, Texas, exemplify this trend. P3s are proving to be attractive tools for these suburban markets, particularly those that are struggling to keep pace with increasing migration and the resulting demand that comes with a growing population. Aging and undersized civic infrastructure are leading the demand for P3s in many of these secondary but growing markets

JLL forecasts continued growth in P3 implementation, particularly in core public infrastructure, energy resilience and affordable housing. P3s work most effectively when aligned with broader institutional planning that considers the full spectrum of public infrastructure delivery options. When implemented appropriately, these partnerships can help address specific challenges within public institutions' comprehensive facility strategies.

About the Author

John Caulfield

John Caulfield is Senior Editor with Building Design + Construction Magazine.