At the end of 2018, analysts at Lodging Econometrics (LE) reported that the total U.S. construction pipeline continued to trend upward with 5,530 projects/669,456 rooms, both up a strong 7% year-over-year (YOY). However, pipeline totals continue to trail the all-time high of 5,883 projects/785,547 rooms reached in the second quarter of 2008.

Project counts in the early planning stage continue to rise reaching an all-time high of 1,723 projects/199,326 rooms, up 14% by projects and 12% by rooms YOY. Projects scheduled to start construction in the next 12 months stand at 2,153 projects/255,083 rooms. Projects currently under construction are at 1,654 projects/215,047 rooms, the highest counts since early 2008.

Also noteworthy at year-end, the upscale, upper-midscale, and midscale categories are at record-highs, for both rooms and projects. Luxury room counts and upper-upscale project counts are also at record levels.

In 2018, the U.S. had 947 new hotels/112,050 rooms open, a 2% growth in new supply, bringing the total U.S. census to 56,909 hotels/5,381,090 rooms. The LE forecast for new hotel openings in 2019 anticipates a 2.2% supply growth rate with 1,022 new hotels/116,357 rooms expected to open. The pace for new hotel openings has slowed slightly because of construction delays largely caused by shortages in skilled labor.

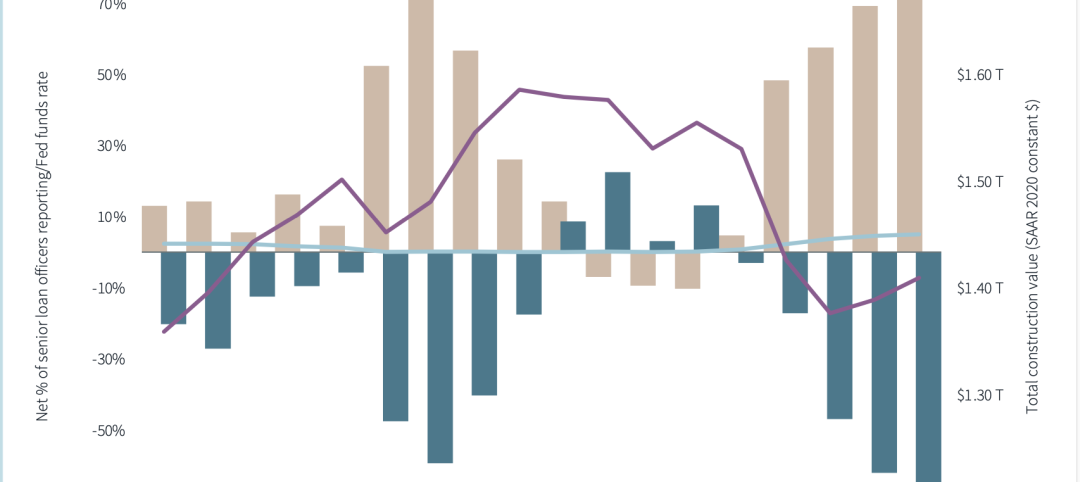

Lending at attractive rates is still accessible to developers, but lenders are growing more selective as we move deeper into the existing cycle.

The pipeline has completed its seventh consecutive year of growth. Moving forward the growth rate is expected to slow as the economies of most countries, including the United States, more firmly settle into the “new normal" marked by slow growth and low inflation.

While there are no visible signs of a recession on the horizon, the risks to the economy are not insignificant and include tariff conflicts, swings in the stock market, unforeseen geopolitical problems, any of which could send the economy lower.

Related Stories

Contractors | Nov 1, 2023

Nonresidential construction spending increases for the 16th straight month, in September 2023

National nonresidential construction spending increased 0.3% in September, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau. On a seasonally adjusted annualized basis, nonresidential spending totaled $1.1 trillion.

Market Data | Oct 23, 2023

New data finds that the majority of renters are cost-burdened

The most recent data derived from the 2022 Census American Community Survey reveals that the proportion of American renters facing housing cost burdens has reached its highest point since 2012, undoing the progress made in the ten years leading up to the pandemic.

Contractors | Oct 19, 2023

Crane Index indicates slowing private-sector construction

Private-sector construction in major North American cities is slowing, according to the latest RLB Crane Index. The number of tower cranes in use declined 10% since the first quarter of 2023. The index, compiled by consulting firm Rider Levett Bucknall (RLB), found that only two of 14 cities—Boston and Toronto—saw increased crane counts.

Market Data | Oct 2, 2023

Nonresidential construction spending rises 0.4% in August 2023, led by manufacturing and public works sectors

National nonresidential construction spending increased 0.4% in August, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau. On a seasonally adjusted annualized basis, nonresidential spending totaled $1.09 trillion.

Giants 400 | Sep 28, 2023

Top 100 University Building Construction Firms for 2023

Turner Construction, Whiting-Turner Contracting Co., STO Building Group, Suffolk Construction, and Skanska USA top BD+C's ranking of the nation's largest university sector contractors and construction management firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report. Note: This ranking includes revenue for all university/college-related buildings except student residence halls, sports/recreation facilities, laboratories, S+T-related buildings, parking facilities, and performing arts centers (revenue for those buildings are reported in their respective Giants 400 ranking).

Construction Costs | Sep 28, 2023

U.S. construction market moves toward building material price stabilization

The newly released Quarterly Construction Cost Insights Report for Q3 2023 from Gordian reveals material costs remain high compared to prior years, but there is a move towards price stabilization for building and construction materials after years of significant fluctuations. In this report, top industry experts from Gordian, as well as from Gilbane, McCarthy Building Companies, and DPR Construction weigh in on the overall trends seen for construction material costs, and offer innovative solutions to navigate this terrain.

Data Centers | Sep 21, 2023

North American data center construction rises 25% to record high in first half of 2023, driven by growth of artificial intelligence

CBRE’s latest North American Data Center Trends Report found there is 2,287.6 megawatts (MW) of data center supply currently under construction in primary markets, reaching a new all-time high with more than 70% already preleased.

Contractors | Sep 12, 2023

The average U.S. contractor has 9.2 months worth of construction work in the pipeline, as of August 2023

Associated Builders and Contractors' Construction Backlog Indicator declined to 9.2 months in August, down 0.1 month, according to an ABC member survey conducted from Aug. 21 to Sept. 6. The reading is 0.5 months above the August 2022 level.

Contractors | Sep 11, 2023

Construction industry skills shortage is contributing to project delays

Relatively few candidates looking for work in the construction industry have the necessary skills to do the job well, according to a survey of construction industry managers by the Associated General Contractors of America (AGC) and Autodesk.

Market Data | Sep 6, 2023

Far slower construction activity forecast in JLL’s Midyear update

The good news is that market data indicate total construction costs are leveling off.