ConstructConnect, a provider of construction information and technology solutions in North America, recently announced the release of its Q4 2017 Forecast Quarterly Report. The Winter 2017-18 starts forecast includes year-over-year estimates for 2017 that have become more upbeat than a quarter ago. Groundbreakings on several mega projects late this year have provided exceptional lift to the industrial and engineering type-of-structure categories.

“Out to 2021, residential will be the main driver of total construction starts, recording year-over-year increases of nearly +6.0% or more,” explained Chief Economist Alex Carrick. “Non-residential building will disappoint, with gains of only about +2.0% each year. Engineering will be strong in 2018 and 2019, as energy initiatives and infrastructure work are promoted by Washington, but will then moderate in 2020-21.”

The forecast which combines ConstructConnect's proprietary data with macroeconomic factors and Oxford Economics econometric expertise, shows some of the more robust 2018 starts forecasts:

- Single-family residential, +8.8%

- Warehouses, +4.7%

- Nursing homes, +5.9%

- Educational facilities, +4.2%

- Roads, +5.9%

- Bridges, +10.2%

- Miscellaneous civil (power, oil and gas), +13.8%

2017 total starts are now expected to be +7.9% (versus an earlier calculated +4.5%). Residential has been upgraded to +10.1% and engineering/civil to +23.1%. Non-residential building has been left essentially flat at -0.5%.

For 2018, the new forecasts shave a bit off what was previously expected. Total starts are now projected to be +4.8%, a little slower than the +5.9% of a quarter ago. Residential will be +6.7% in 2018; non-res building, +1.9%; and heavy engineering/civil, +6.6%.

In residential construction, the multi-family market has had its turn and it will be the single-family market that will expand more rapidly moving forward, aided by family-formations among the millennial generation.

The forecast reports that educational facilities will grow faster than hospitals in 2018, but beginning in 2019 their positions will reverse. Some other non-residential building type-of-structure categories with bullish outlooks include: courthouses and prisons; warehouses; and nursing homes. Airports and sports stadiums will also be stepping into the construction spotlight.

The report noted a few ongoing economic trends:

- A synchronous world expansion is underway, with North America, Japan, China and Europe all experiencing GDP growth

- Based on demographics, housing starts have fallen short of potential for almost a decade

- Office space demand will increasingly come from firms engaged in high-tech

- Prices for many internationally traded commodities are on the mend

To learn more about ConstructConnect or get a free copy of the Forecast Quarterly Report, visit constructconnect.com.

Related Stories

Industry Research | Apr 25, 2023

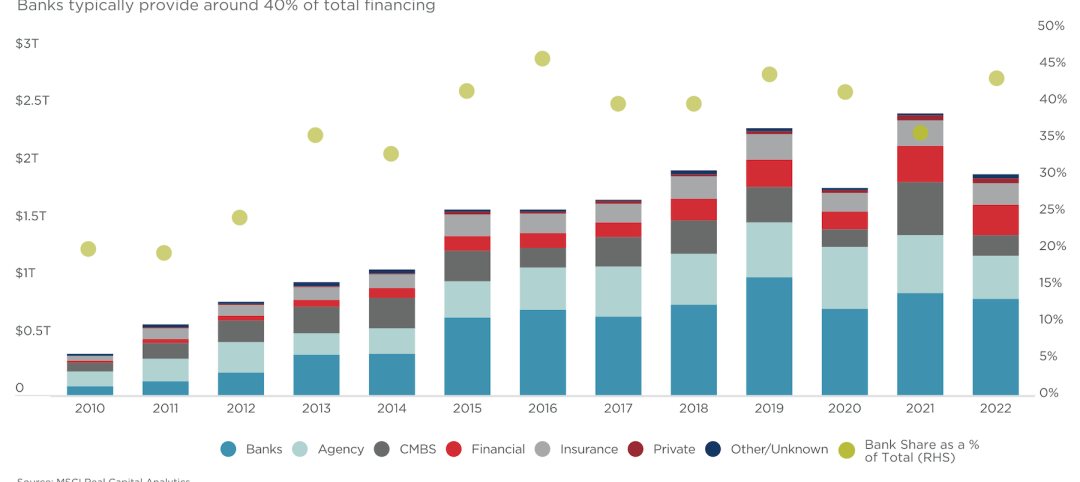

The commercial real estate sector shouldn’t panic (yet) about recent bank failures

A new Cushman & Wakefield report depicts a “well capitalized” banking industry that is responding assertively to isolated weaknesses, but is also tightening its lending.

Architects | Apr 21, 2023

Architecture billings improve slightly in March

Architecture firms reported a modest increase in March billings. This positive news was tempered by a slight decrease in new design contracts according to a new report released today from The American Institute of Architects (AIA). March was the first time since last September in which billings improved.

Contractors | Apr 19, 2023

Rising labor, material prices cost subcontractors $97 billion in unplanned expenses

Subcontractors continue to bear the brunt of rising input costs for materials and labor, according to a survey of nearly 900 commercial construction professionals.

Data Centers | Apr 14, 2023

JLL's data center outlook: Cloud computing, AI driving exponential growth for data center industry

According to JLL’s new Global Data Center Outlook, the mass adoption of cloud computing and artificial intelligence (AI) is driving exponential growth for the data center industry, with hyperscale and edge computing leading investor demand.

Healthcare Facilities | Apr 13, 2023

Healthcare construction costs for 2023

Data from Gordian breaks down the average cost per square foot for a three-story hospital across 10 U.S. cities.

Higher Education | Apr 13, 2023

Higher education construction costs for 2023

Fresh data from Gordian breaks down the average cost per square foot for a two-story college classroom building across 10 U.S. cities.

Market Data | Apr 13, 2023

Construction input prices down year-over-year for first time since August 2020

Construction input prices increased 0.2% in March, according to an Associated Builders and Contractors analysis of U.S. Bureau of Labor Statistics Producer Price Index data released today. Nonresidential construction input prices rose 0.4% for the month.

Market Data | Apr 11, 2023

Construction crane count reaches all-time high in Q1 2023

Toronto, Seattle, Los Angeles, and Denver top the list of U.S/Canadian cities with the greatest number of fixed cranes on construction sites, according to Rider Levett Bucknall's RLB Crane Index for North America for Q1 2023.

Contractors | Apr 11, 2023

The average U.S. contractor has 8.7 months worth of construction work in the pipeline, as of March 2023

Associated Builders and Contractors reported that its Construction Backlog Indicator declined to 8.7 months in March, according to an ABC member survey conducted March 20 to April 3. The reading is 0.4 months higher than in March 2022.

Market Data | Apr 6, 2023

JLL’s 2023 Construction Outlook foresees growth tempered by cost increases

The easing of supply chain snags for some product categories, and the dispensing with global COVID measures, have returned the North American construction sector to a sense of normal. However, that return is proving to be complicated, with the construction industry remaining exceptionally busy at a time when labor and materials cost inflation continues to put pricing pressure on projects, leading to caution in anticipation of a possible downturn. That’s the prognosis of JLL’s just-released 2023 U.S. and Canada Construction Outlook.