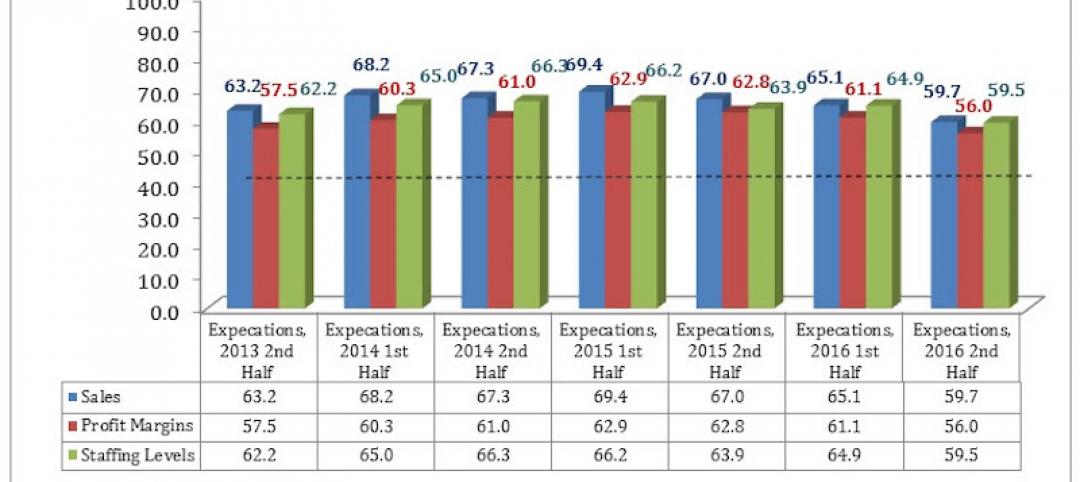

The Trump Administration’s plans for infrastructure investment, regulatory reform, and tax relief have ignited a burst of enthusiasm among U.S. engineering firm leaders, propelling the American Council of Engineering Companies’ Engineering Business Index (EBI) to its largest ever quarterly increase.

The 4th Quarter 2016 (Q4/2016) EBI surged 5.1 points to 66.5, up from the 61.4 score of Q3/2016. The previous largest increase was 1.5 points between the Q1/2014 and Q2/2014 surveys. Any score above 50 signifies that the market is growing The EBI is a leading indicator of America’s economic health based on the business performance and projections of engineering firms responsible for developing the nation’s transportation, water, energy, and industrial infrastructure. The Q4/2016 survey of 317 engineering firm leaders was conducted November 31 to December 20.

Survey results show firm leader market expectations for one year from today rose a hefty 8.8 points to 72.1, the largest quarter-over-quarter increase since the EBI’s inception in January 2014. Expectations for both short- and long-term profitability also climbed. Firm leader optimism for improved profitability over the next six months rose 3.6 points to 69.0; increased to 72.9 for one year from now; and climbed 2.9 points to 70.5 for three years from now.

“We finally have a president who understands business!” says one respondent. “We’re looking forward to some significant tax relief with the new Administration,” says another.

The boost in firm leader optimism extends across almost the entire engineering marketplace. In public markets, transportation showed the strongest increase, up an eye-catching 9.5 points to 73.7.

All other public market sectors rose: Water and Wastewater (up 7.5, to 70.5), Education (up 3.2 to 58.2) Health Care (up 0.3, to 56.1), and Environmental (up 1.1 to 55.4). A new public sector category, Buildings, debuted at 65.2. Among the private client markets, firm leaders were most bullish about the Industrial/Manufacturing sector, which leaped up 12.5 points to 70.7. Four key private sector markets also climbed: Energy and Power (up 8.8, to 69.2), Land Development (up 8.2, to 68.4.), Buildings (up 4.1 to 67.0), and Education (up 5.2, to 58.5).

For the complete Quarter 4, 2016 Engineering Business Index, go to www.acec.org.

Related Stories

Market Data | Apr 3, 2017

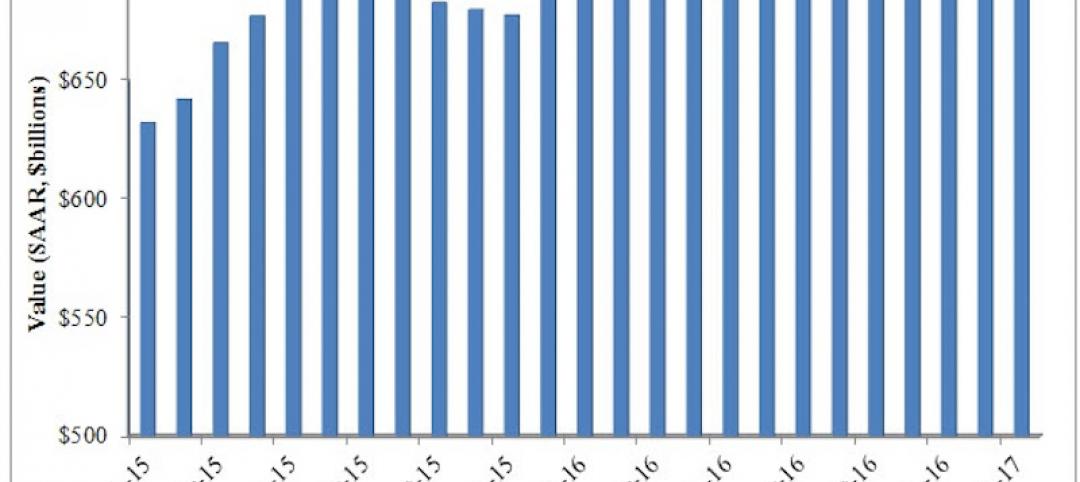

Public nonresidential construction spending rebounds; overall spending unchanged in February

The segment totaled $701.9 billion on a seasonally adjusted annualized rate for the month, marking the seventh consecutive month in which nonresidential spending sat above the $700 billion threshold.

Market Data | Mar 29, 2017

Contractor confidence ends 2016 down but still in positive territory

Although all three diffusion indices in the survey fell by more than five points they remain well above the threshold of 50, which signals that construction activity will continue to be one of the few significant drivers of economic growth.

Market Data | Mar 24, 2017

These are the most and least innovative states for 2017

Connecticut, Virginia, and Maryland are all in the top 10 most innovative states, but none of them were able to claim the number one spot.

Market Data | Mar 22, 2017

After a strong year, construction industry anxious about Washington’s proposed policy shifts

Impacts on labor and materials costs at issue, according to latest JLL report.

Market Data | Mar 22, 2017

Architecture Billings Index rebounds into positive territory

Business conditions projected to solidify moving into the spring and summer.

Market Data | Mar 15, 2017

ABC's Construction Backlog Indicator fell to end 2016

Contractors in each segment surveyed all saw lower backlog during the fourth quarter, with firms in the heavy industrial segment experiencing the largest drop.

Market Data | Feb 28, 2017

Leopardo’s 2017 Construction Economics Report shows year-over-year construction spending increase of 4.2%

The pace of growth was slower than in 2015, however.

Market Data | Feb 23, 2017

Entering 2017, architecture billings slip modestly

Despite minor slowdown in overall billings, commercial/ industrial and institutional sectors post strongest gains in over 12 months.

Market Data | Feb 16, 2017

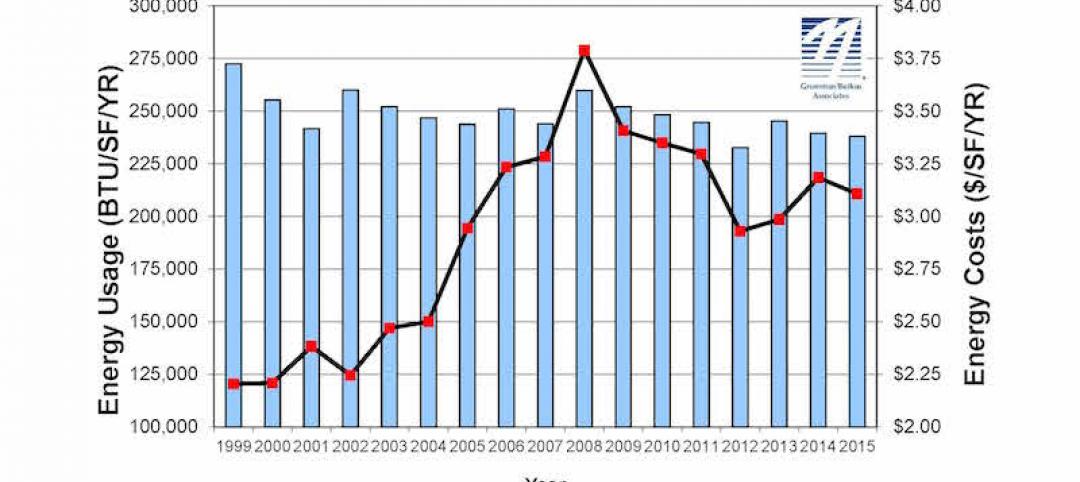

How does your hospital stack up? Grumman/Butkus Associates 2016 Hospital Benchmarking Survey

Report examines electricity, fossil fuel, water/sewer, and carbon footprint.

Market Data | Feb 1, 2017

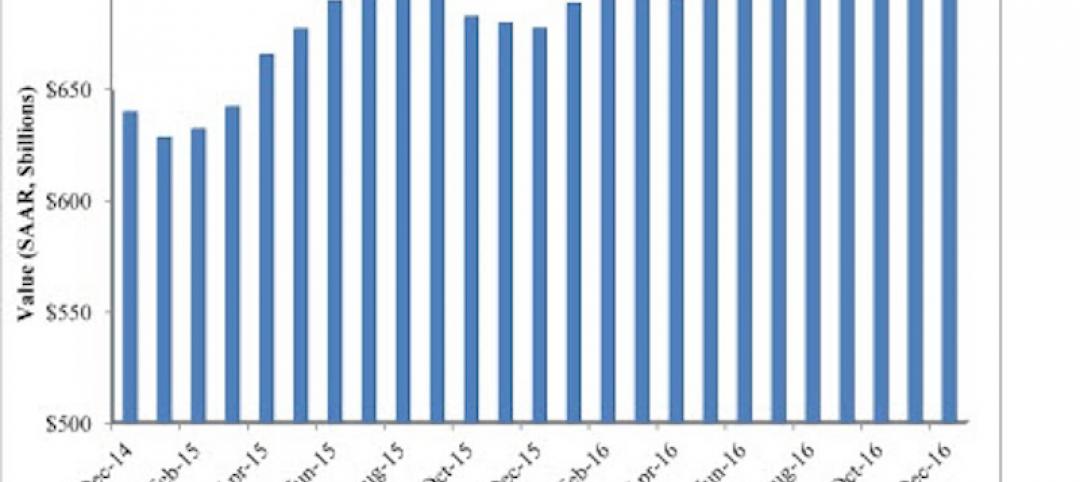

Nonresidential spending falters slightly to end 2016

Nonresidential spending decreased from $713.1 billion in November to $708.2 billion in December.