More than 10 years after the end of the most severe financial crisis since the Great Depression, the U.S. economy is again making history by continuing its longest-ever expansion. Nevertheless, emerging weakness in business investment has been hinting at softening outlays, giving commercial and industrial construction contractors cause for concern, according to a mid-year economic outlook by Anirban Basu, chief economist of Associated Builders and Contractors.

“Given that every expansion in U.S. history has ended in recession, leaders of construction firms are rightly wondering when the record-setting expansion will end,” said Basu. “Looking at conditions on the ground, it likely won’t be in 2019, but 2020 could be problematic for the broader economy and 2021 for a significant number of contractors.”

Basu cites numerous vulnerabilities that could trigger a recession in 2020, including:

— Trade wars

— Softening corporate earnings

— Slowing job growth

— Elevated levels of household, corporate and government debt

— Election 2020

But there are plenty of reasons to remain optimistic. “For the most part, the economy has held up better than anticipated,” said Basu. “During the first quarter of 2019, gross domestic product expanded at a smart 3.1% annualized rate. The U.S. Bureau of Economic Analysis’ initial estimate suggests that the economy slowed to 2.1% growth during the second quarter, but that neatly beat economists’ expectation that that growth had fallen below 2%.”

“The economy could continue to prove resilient,” says Basu. “To date, the economy has navigated ongoing trade disputes and associated tariffs with aplomb. It has also withstood serial interest rate hikes, the longest federal government shutdown in history, extreme weather, shifting immigration policy, ongoing labor market shortages and a lengthy investigation regarding foreign influence in U.S. elections.”

To read the full economic outlook story, visit ConstructionExec.com.

Related Stories

Market Data | Aug 2, 2017

Nonresidential Construction Spending falls in June, driven by public sector

June’s weak construction spending report can be largely attributed to the public sector.

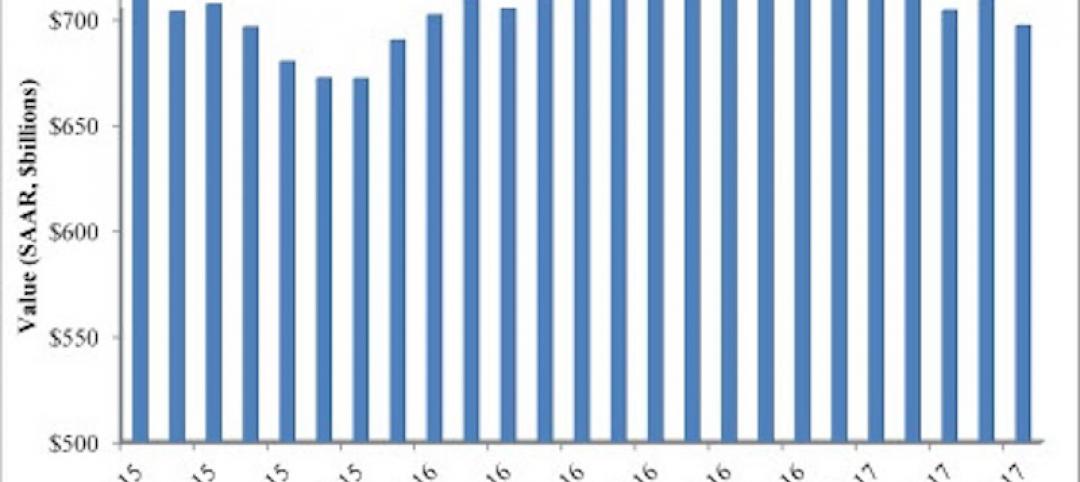

Market Data | Jul 31, 2017

U.S. economic growth accelerates in second quarter; Nonresidential fixed investment maintains momentum

Nonresidential fixed investment, a category of GDP embodying nonresidential construction activity, expanded at a 5.2% seasonally adjusted annual rate.

Multifamily Housing | Jul 27, 2017

Apartment market index: Business conditions soften, but still solid

Despite some softness at the high end of the apartment market, demand for apartments will continue to be substantial for years to come, according to the National Multifamily Housing Council.

Market Data | Jul 25, 2017

What's your employer value proposition?

Hiring and retaining talent is one of the top challenges faced by most professional services firms.

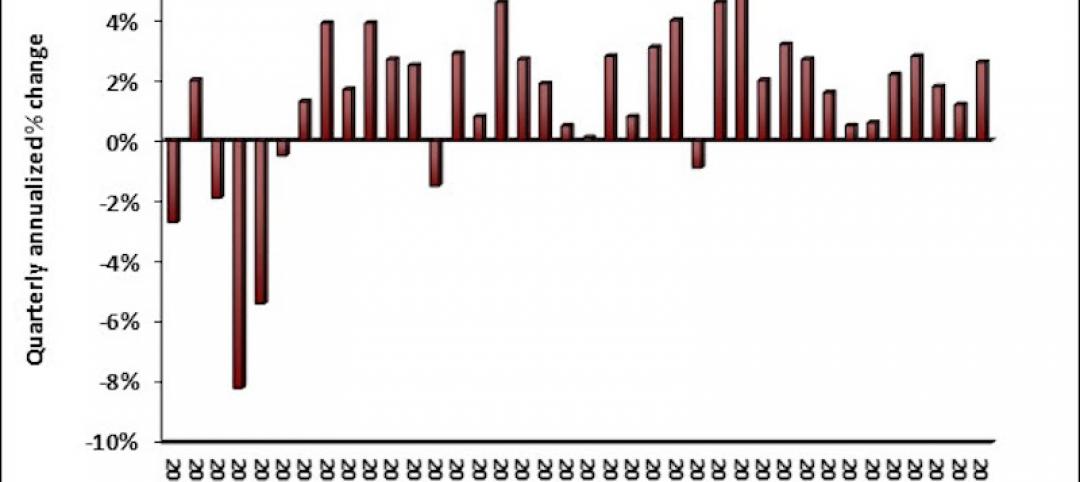

Market Data | Jul 25, 2017

Moderating economic growth triggers construction forecast downgrade for 2017 and 2018

Prospects for the construction industry have weakened with developments over the first half of the year.

Industry Research | Jul 6, 2017

The four types of strategic real estate amenities

From swimming pools to pirate ships, amenities (even crazy ones) aren’t just perks, but assets to enhance performance.

Market Data | Jun 29, 2017

Silicon Valley, Long Island among the priciest places for office fitouts

Coming out on top as the most expensive market to build out an office is Silicon Valley, Calif., with an out-of-pocket cost of $199.22.

Market Data | Jun 26, 2017

Construction disputes were slightly less contentious last year

But poorly written and administered contracts are still problems, says latest Arcadis report.

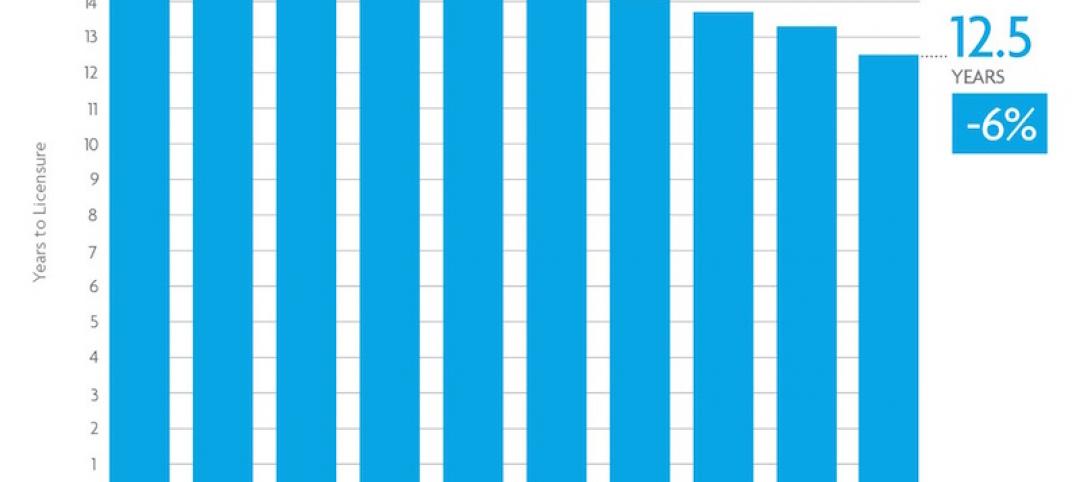

Industry Research | Jun 26, 2017

Time to earn an architecture license continues to drop

This trend is driven by candidates completing the experience and examination programs concurrently and more quickly.

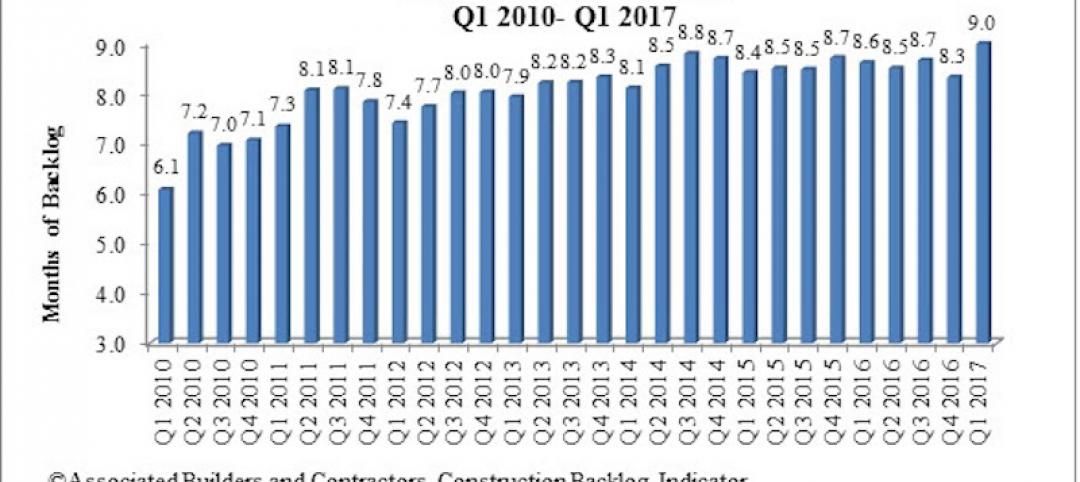

Industry Research | Jun 22, 2017

ABC's Construction Backlog Indicator rebounds in 2017

The first quarter showed gains in all categories.