In the second quarter of 2021, analysts at Lodging Econometrics (LE) report that the top franchise companies with the largest construction pipelines are: Marriott International with 1,301 projects/170,847 rooms, Hilton Worldwide with 1,216 projects/139,172 rooms, and InterContinental Hotels Group (IHG) with 777 projects/78,929 rooms. Development projects with these three franchise companies comprise 69% of all projects in the total construction pipeline.

The largest brands for each of these companies are Marriott’s Fairfield Inn with 257 projects/25,051 rooms, Hilton’s Home2 Suites by Hilton, with 379 projects/39,584 rooms and IHG’s Holiday Inn Express with 303 projects/29,055 rooms. These three brands make up 20% of the total construction pipeline rooms in the U.S.

Other high-volume brands in the pipeline for each of these franchises are Marriott’s TownePlace Suites with 198 projects/19,422 rooms and Residence Inn with 189 projects/23,493 rooms; Hilton’s Hampton by Hilton with 269 projects/28,071 rooms and Tru by Hilton with 235 projects/22,521 rooms; and IHG’s Avid Hotel with 157 projects/13,842 rooms and Staybridge Suites with 122 projects/12,607 rooms.

In the second quarter of 2021, LE recorded 583 conversion projects/63,807 rooms. Of these conversion totals, Best Western leads with 116 conversion projects/10,289 rooms, accounting for 20% of the conversion pipeline by projects. Following Best Western is Choice Hotels, Marriott International, and Hilton Worldwide. Best Western and these three franchise companies combined account for 61% of all the rooms in the conversion pipeline across the United States.

472 new hotels with 59,034 rooms opened across the United States during the first half of 2021. Marriott, Hilton, and IHG collectively opened 74% of the hotels. Marriott opened 152 hotels with 20,416 rooms, Hilton opened 125 hotels/16,970 rooms, and IHG opened 72 hotels/7,249 rooms.

Related Stories

Market Data | Apr 16, 2019

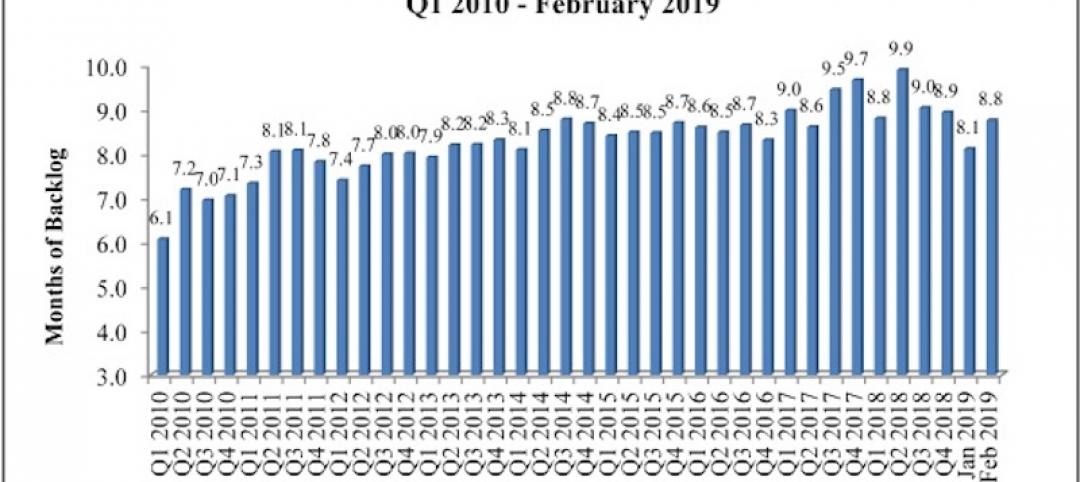

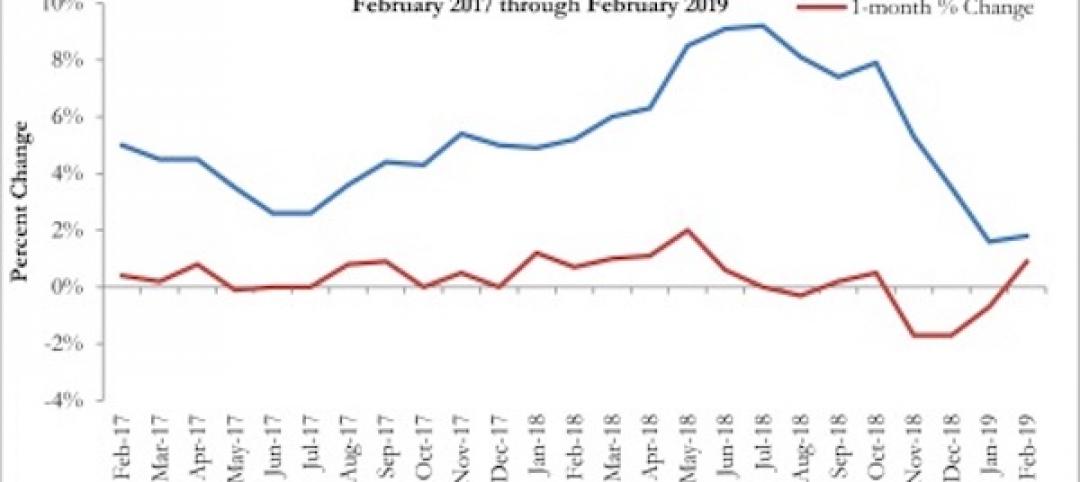

ABC’s Construction Backlog Indicator rebounds in February

ABC's Construction Backlog Indicator expanded to 8.8 months in February 2019.

Market Data | Apr 8, 2019

Engineering, construction spending to rise 3% in 2019: FMI outlook

Top-performing segments forecast in 2019 include transportation, public safety, and education.

Market Data | Apr 1, 2019

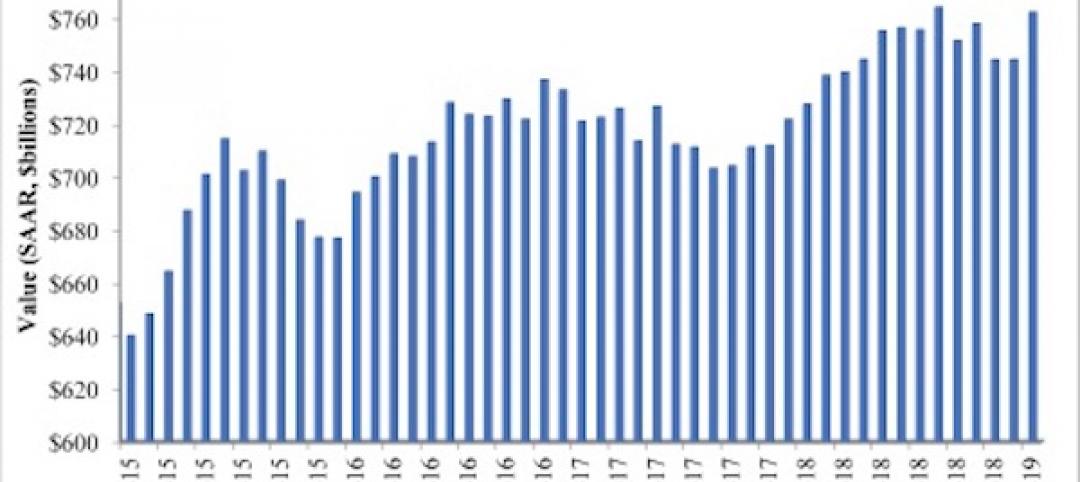

Nonresidential spending expands again in February

Private nonresidential spending fell 0.5% for the month and is only up 0.1% on a year-over-year basis.

Market Data | Mar 22, 2019

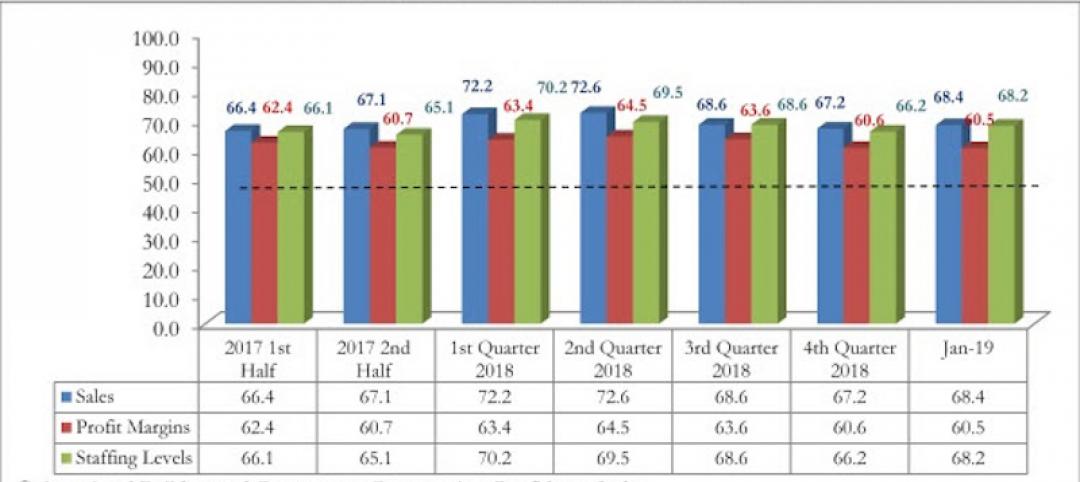

Construction contractors regain confidence in January 2019

Expectations for sales during the coming six-month period remained especially upbeat in January.

Market Data | Mar 21, 2019

Billings moderate in February following robust New Year

AIA’s Architecture Billings Index (ABI) score for February was 50.3, down from 55.3 in January.

Market Data | Mar 19, 2019

ABC’s Construction Backlog Indicator declines sharply in January 2019

The Construction Backlog Indicator contracted to 8.1 months during January 2019.

Market Data | Mar 15, 2019

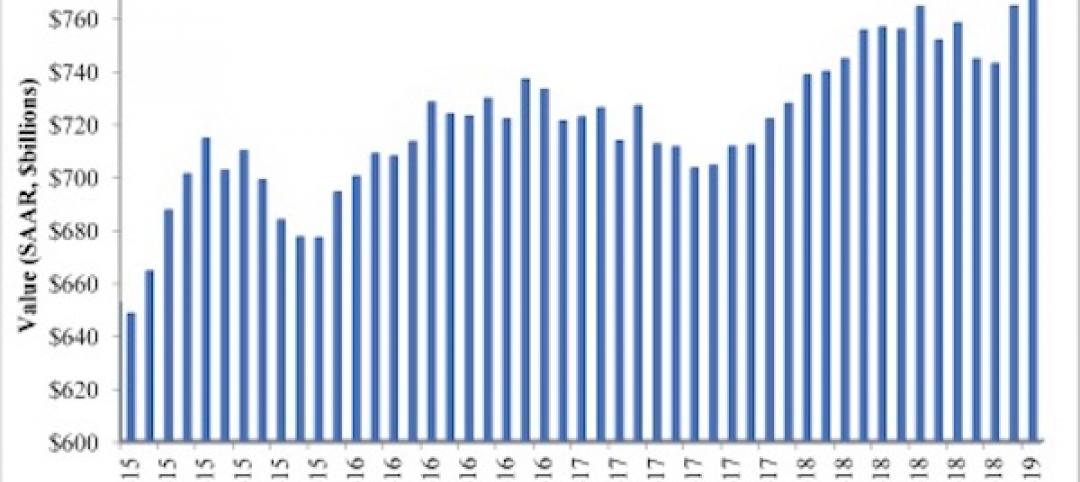

2019 starts off with expansion in nonresidential spending

At a seasonally adjusted annualized rate, nonresidential spending totaled $762.5 billion for the month.

Market Data | Mar 14, 2019

Construction input prices rise for first time since October

Of the 11 construction subcategories, seven experienced price declines for the month.

Market Data | Mar 6, 2019

Global hotel construction pipeline hits record high at 2018 year-end

There are a record-high 6,352 hotel projects and 1.17 million rooms currently under construction worldwide.

Market Data | Feb 28, 2019

U.S. economic growth softens in final quarter of 2018

Year-over-year GDP growth was 3.1%, while average growth for 2018 was 2.9%.