Strong construction momentum will easily carry through the first half of 2019, despite project margins facing pressure from all sides. JLL’s Construction Outlook finds robust U.S. economic fundamentals will drive further growth of the sector, which in 2018 recorded a 5.1% increase in total construction value and a 4.5% increase in employment.

Potential risks to the construction sector such as trade war escalation, deteriorating macroeconomic conditions and the worsening labor shortage, are largely balanced by potential boosts that include a large-scale federal infrastructure package, relief from tariffs and the continuation of 3.5% annual GDP growth.

“All forward indicators for construction are still flashing green,” said Todd Burns, President, Project and Development Services, JLL Americas. “However, a year with growth equal to that of 2018 would be considered a success, given concerns of a broader economic slowdown.”

Rising construction costs will sideline select projects

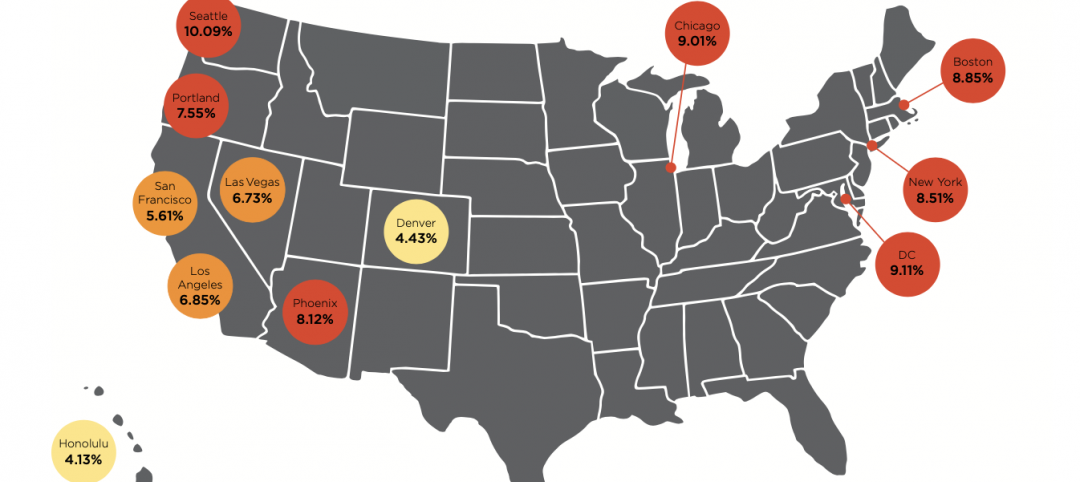

Total building costs, which includes labor, materials and equipment, grew by 3.4% in 2018, outpacing the U.S. inflation rate of 1.9%. The widening spread between cost growth and inflation is pushing borderline projects past the threshold of profitability. Building costs will continue to increase in 2019 but at a slower rate than 2018. This reflects an expected cooldown in material pricing but the surging cost of labor.

Growth in total construction employment has hovered between 3 and 6% over the past six years – a far cry from what’s required for labor supply to catch up with demand. With a tight national employment market, the situation is unlikely to improve anytime soon. Construction wage growth in 2019 will top the 3.4% increase seen last year.

Trade policy a powerful “swing” force

With a direct impact on commodity prices, tariffs represent a uniquely immediate threat to an industry that typically moves slowly. Given the well-established political willingness to impose tariffs and the widening trade deficit with China, a continuation of tariffs in 2019 is expected.

The biggest chance for relief from tariffs are international trade deals that would lift tariffs in exchange for other trade or economic concessions. Such a deal could represent a dramatic positive for construction and is a potential bright spot for the industry.

Construction tech in growth mode, presents opportunity for labor shortage relief

The buzz around construction technology has long eclipsed actual adoption in the industry. The past year, however, saw meaningful gains fueled by large general contracting firms racing to improve productivity and remain competitive. High levels of tech adoption will spread to smaller firms, and elements of construction tech will become the standard across the industry in 2019. Amid intense labor pressures, contractors’ most common reason for making technology investments is to increase labor productivity.

Modular construction is poised to have the biggest long-term impact on the industry. Proponents of the technology envision a future full of dedicated warehouses churning out modular components – from exterior wall segments to entire apartment units – for most new construction.

“Adopting modular construction is not always as simple as it sounds,” said Henry D’Esposito, Senior Research Analyst, Project and Development Services, JLL. “There is often a prolonged period during which the benefits are not fully realized, as firms take time to adjust to the new system. Despite some of the initial challenges, there has been no hesitation among contractors about whether modular will continue to grow.”

Growth of modular construction in 2019 will be centered around increased use by select sectors, including hospitality and healthcare, and an increase in use for one or two select elements within a broader array of projects.

Related Stories

Market Data | Jan 31, 2022

Canada's hotel construction pipeline ends 2021 with 262 projects and 35,325 rooms

At the close of 2021, projects under construction stand at 62 projects/8,100 rooms.

Market Data | Jan 27, 2022

Record high counts for franchise companies in the early planning stage at the end of Q4'21

Through year-end 2021, Marriott, Hilton, and IHG branded hotels represented 585 new hotel openings with 73,415 rooms.

Market Data | Jan 27, 2022

Dallas leads as the top market by project count in the U.S. hotel construction pipeline at year-end 2021

The market with the greatest number of projects already in the ground, at the end of the fourth quarter, is New York with 90 projects/14,513 rooms.

Market Data | Jan 26, 2022

2022 construction forecast: Healthcare, retail, industrial sectors to lead ‘healthy rebound’ for nonresidential construction

A panel of construction industry economists forecasts 5.4 percent growth for the nonresidential building sector in 2022, and a 6.1 percent bump in 2023.

Market Data | Jan 24, 2022

U.S. hotel construction pipeline stands at 4,814 projects/581,953 rooms at year-end 2021

Projects scheduled to start construction in the next 12 months stand at 1,821 projects/210,890 rooms at the end of the fourth quarter.

Market Data | Jan 19, 2022

Architecture firms end 2021 on a strong note

December’s Architectural Billings Index (ABI) score of 52.0 was an increase from 51.0 in November.

Market Data | Jan 13, 2022

Materials prices soar 20% in 2021 despite moderating in December

Most contractors in association survey list costs as top concern in 2022.

Market Data | Jan 12, 2022

Construction firms forsee growing demand for most types of projects

Seventy-four percent of firms plan to hire in 2022 despite supply-chain and labor challenges.

Market Data | Jan 7, 2022

Construction adds 22,000 jobs in December

Jobless rate falls to 5% as ongoing nonresidential recovery offsets rare dip in residential total.

Market Data | Jan 6, 2022

Inflation tempers optimism about construction in North America

Rider Levett Bucknall’s latest report cites labor shortages and supply chain snags among causes for cost increases.