Through September, spending on nonresidential construction was up 9.2%, to $883.9 billion, according to preliminary estimates by the Commerce Department’s Bureau of the Census. Sectors hard-hit by the coronavirus pandemic—including lodging, retail/commercial, and even office—were showing signs of life.

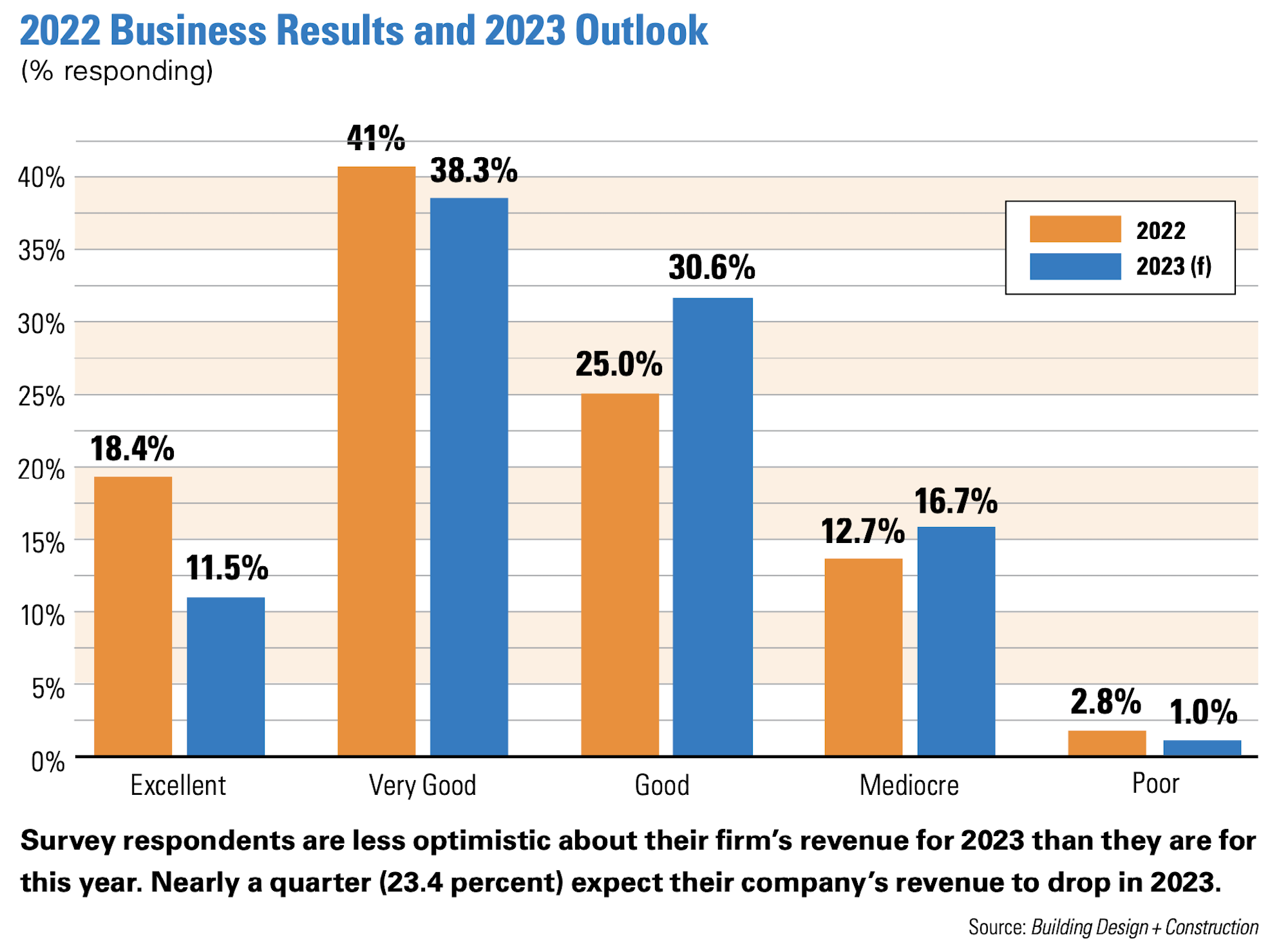

So it makes sense that a recent polling of 212 architects, engineers, contractors, and developer/owners found nearly three-fifths of respondents—59.4%—rating 2022 an “excellent” or “good” business year. Only 15.6% rated the year “mediocre” or “poor.”

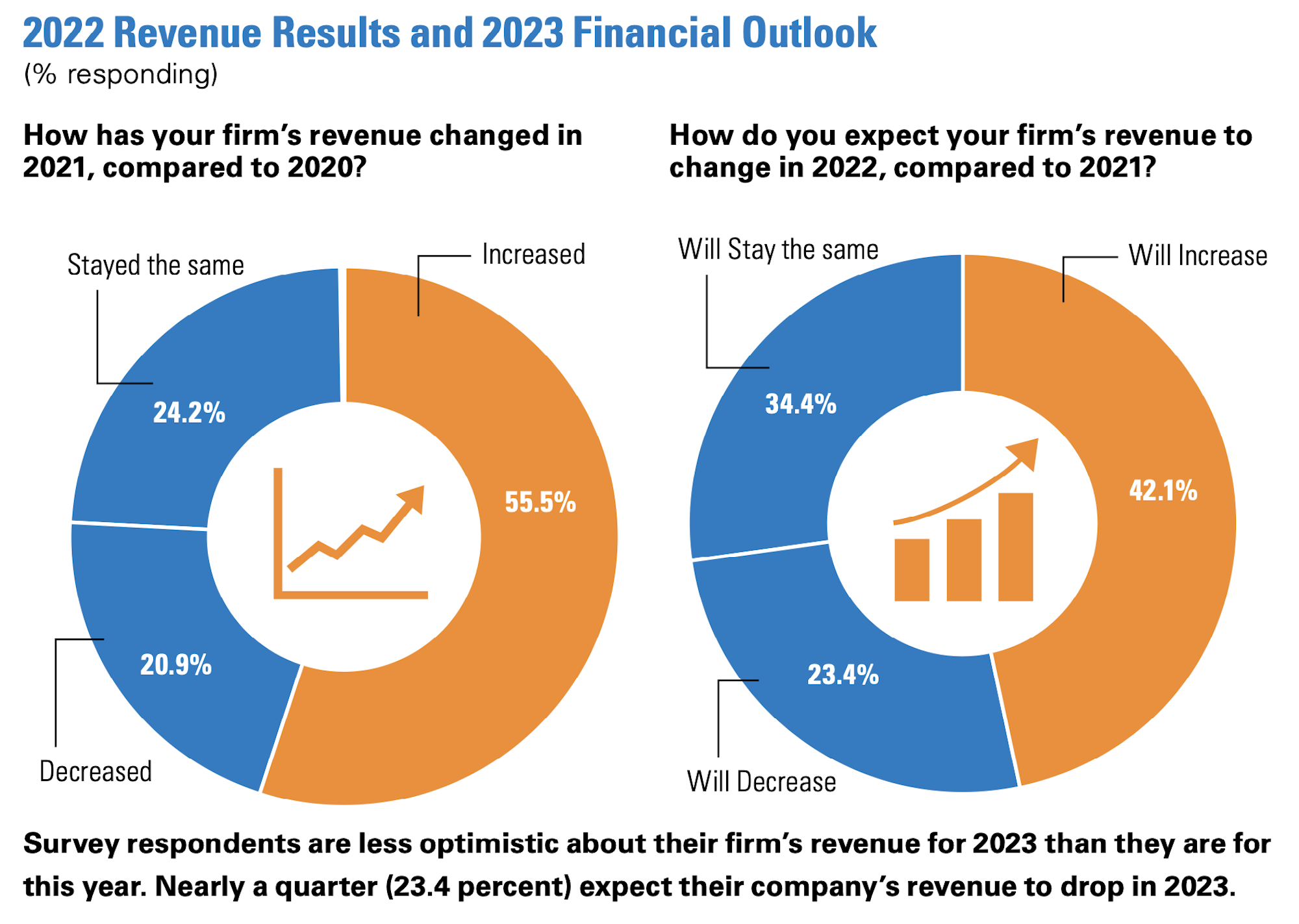

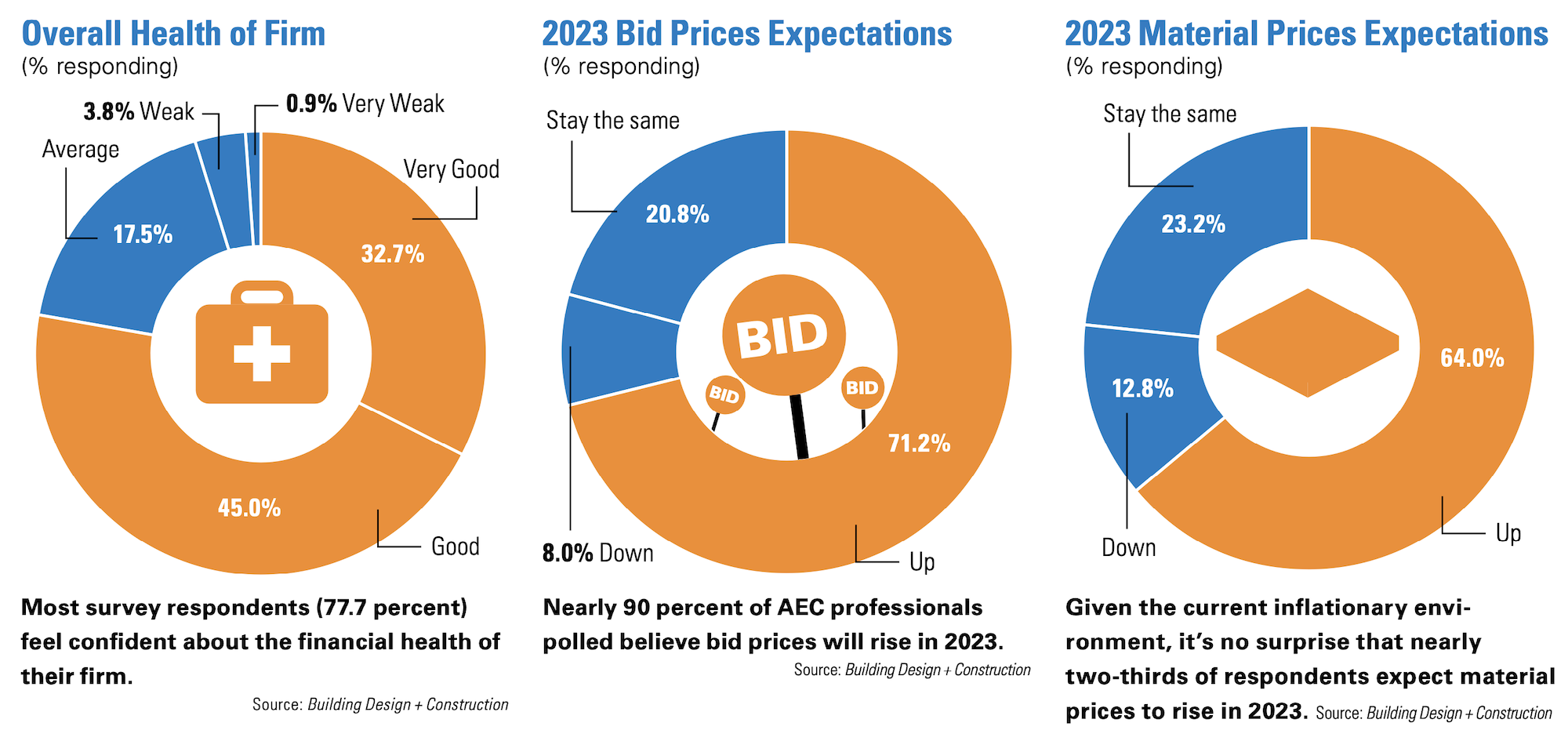

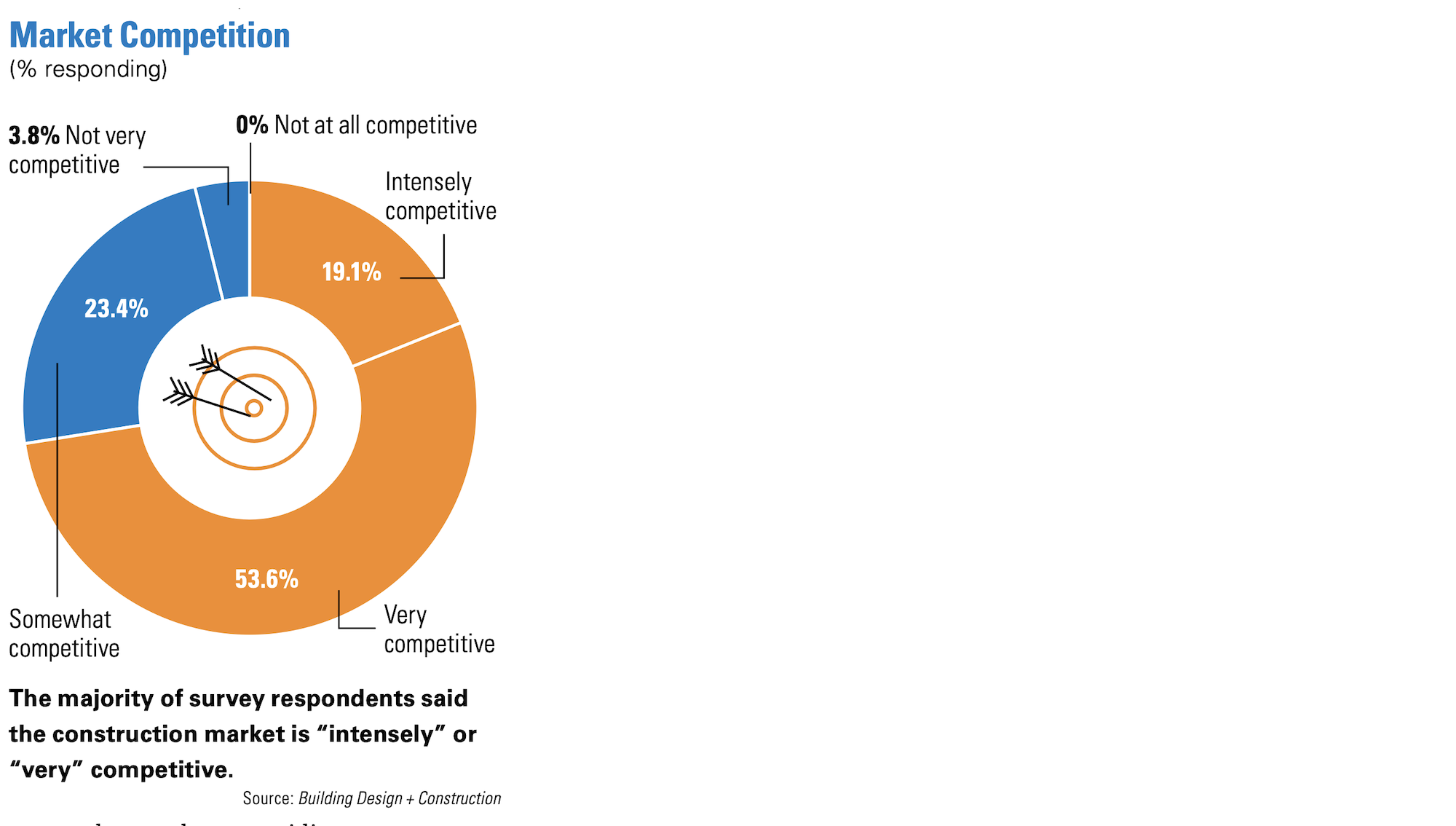

The vast majority of firms, 77.7%, rated their overall health “very good” or “good.” Conversely, only 4.7% saw their firms’ financial condition as either “weak” or “very weak.” Among the firms polled, 55% confirmed their revenue had increased, and another 20.9% said their revenue was level with last year’s. Gains were achieved despite nearly three-quarters of the firms surveyed characterizing the construction/materials market hobbled by supply-chain snags as “intensely” or “very” competitive.

Euphoria, though, might be short-lived, and firms are tempering their prognoses about the future. Nearly one-quarter—23.4%—expect their revenue to be down in 2023, and another 34.4% predict a flat year. Competition ranked third, behind general economic conditions and inflation, as the most important concern AEC firms believe they will face next year. Nearly two-thirds—64%—anticipate that materials prices will continue to rise in 2023. An even higher number, 71.2%, said they were girding for increases in bid prices for projects.

Our poll also found at least one-fifth of firms are concerned about the availability of capital funding for projects, regulations, cashflow management, and keeping their staffs motivated.

When asked about what business development strategies they planned to deploy next year, more than half—53.4%—said they would hire selectively to burnish their firms’ competitiveness, and 47.1% were planning to step up their staff training and education to enhance competitiveness.

Other business strategies these firms are plotting include increasing their marketing and public relations (25.3% of firms polled currently don’t use social media, and among that do LinkedIn is their preferred platform), investing more in technology, and creating new service or business opportunity.

U.S. design and construction firms pick their battles, sector by sector

Our survey asked AEC firms to assess their prospects in 18 construction sectors. Sizable percentages (at least 30%) were hopeful about business for airports, data centers, government/military buildings, healthcare, industrial/warehouse, multifamily and senior living residential, science + technology, and university. At least 20% of respondents saw their prospects as “average” for performing arts centers, hospitality, K-12 education, and sports and recreations. AEC firms placed offices and interior fitouts, religious, and retail/commercial in the “weak” or “very weak” categories.

Here's a closer look at their responses. Keep in mind that these firms aren’t active in every sector, so the numbers providing ratings were smaller than the total in each category. It’s also worth noting that nearly one-third of the AEC firms polled generate between 25% and 74% of their annual business from reconstruction projects:

• Healthcare appears to hold out the greatest opportunities for next year. More than 45% of respondents rated their prospects in this sector as excellent or good. Multifamily received those ratings from 43.1% or AEC firms polled, industrial/warehouse from 39.7%, and data centers from 37.8%.

• Through September, construction spending in the office sector was up only 0.7%, according to Census Bureau estimates. The AEC firms that responded to our survey aren’t anticipating a rebound in this sector any time soon: 41.3% rated their prospects weak or very week. Another 23.5% gave the same ratings to office interiors and fitouts.

Even though Census estimates that the commercial sector (which encompasses retail) was up 22.4% through September, our survey’s respondents are still taking a wait-and-see approach, as 33.3% saw their prospects in retail next year as weak or very weak.

• 29% of respondents said their firms don’t build in the retail sector. And even with the uptick in firms that have expanded their practices and services, only around 10% of our survey’s respondents see mergers or acquisitions in their immediate futures. Our survey reveals an industry whose firms, in many cases, focus on a limited array of typologies and clients, and leave other sectors to specialists.

It was not surprising that 53.2% of respondent firms aren’t building airports and 41.2% aren’t active in the religious sector. Only about half of respondent firms—46.2%—engage performing arts center projects, and 44.3% keep their distances from data centers. But even some of the broader sectors, notably education, find between 30% and 33% of respondent firms absent. Nearly two-fifths aren’t active in science + technology construction, either, and more than two-fifths don’t build in the multifamily sector.

Related Stories

Hotel Facilities | Oct 31, 2022

These three hoteliers make up two-thirds of all new hotel development in the U.S.

With a combined 3,523 projects and 400,490 rooms in the pipeline, Marriott, Hilton, and InterContinental dominate the U.S. hotel construction sector.

Laboratories | Oct 5, 2022

Bigger is better for a maturing life sciences sector

CRB's latest report predicts more diversification and vertical integration in research and production.

Multifamily Housing | May 11, 2022

Kitchen+Bath AMENITIES – Take the survey for a chance at a $50 gift card

MULTIFAMILY DESIGN + CONSTRUCTION is conducting a research study on the use of kitchen and bath products in the $106 billion multifamily construction sector.

Market Data | Apr 14, 2022

FMI 2022 construction spending forecast: 7% growth despite economic turmoil

Growth will be offset by inflation, supply chain snarls, a shortage of workers, project delays, and economic turmoil caused by international events such as the Russia-Ukraine war.

Industrial Facilities | Apr 14, 2022

JLL's take on the race for industrial space

In the previous decade, the inventory of industrial space couldn’t keep up with demand that was driven by the dual surges of the coronavirus and online shopping. Vacancies declined and rents rose. JLL has just published a research report on this sector called “The Race for Industrial Space.” Mehtab Randhawa, JLL’s Americas Head of Industrial Research, shares the highlights of a new report on the industrial sector's growth.

Codes and Standards | Apr 4, 2022

Construction of industrial space continues robust growth

Construction and development of new industrial space in the U.S. remains robust, with all signs pointing to another big year in this market segment

Industry Research | Apr 4, 2022

Nonresidential Construction Spending Drops Slightly in February, Says ABC

National nonresidential construction spending was down 0.1% in February, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau

Reconstruction & Renovation | Mar 28, 2022

Is your firm a reconstruction sector giant?

Is your firm active in the U.S. building reconstruction, renovation, historic preservation, and adaptive reuse markets? We invite you to participate in BD+C's inaugural Reconstruction Market Research Report.

Industry Research | Mar 28, 2022

ABC Construction Backlog Indicator unchanged in February

Associated Builders and Contractors reported today that its Construction Backlog Indicator remained unchanged at 8.0 months in February, according to an ABC member survey conducted Feb. 21 to March 8.

Industry Research | Mar 23, 2022

Architecture Billings Index (ABI) shows the demand for design service continues to grow

Demand for design services in February grew slightly since January, according to a new report today from The American Institute of Architects (AIA).