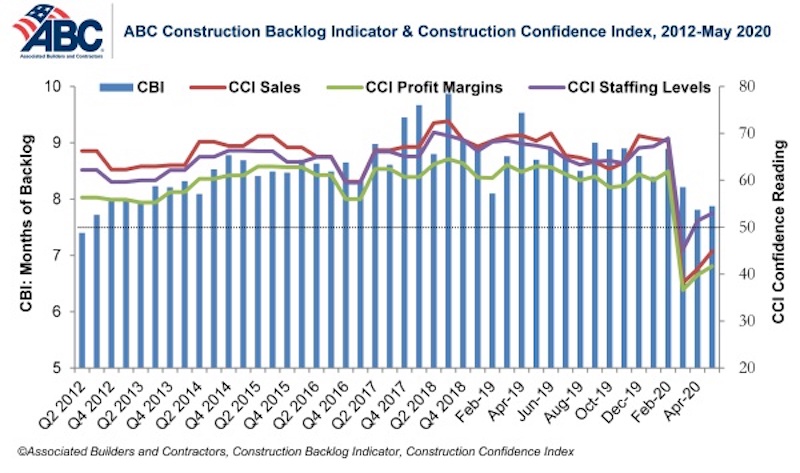

Construction Backlog Indicator rose to 7.9 months in May, an increase of less than 0.1 months from April’s reading. Furthermore, based on an ABC member survey conducted May 20-June 3, results indicate that confidence among U.S. construction industry leaders continued to rebound from the historically low levels observed in the March survey.

Nonresidential construction backlog is down 0.8 months compared to May 2019 and declined year over year in every industry, classification and region. Backlog in the heavy industrial category, however, increased by nearly one month in May after reaching its lowest level in the history of the series in April.

ABC’s Construction Confidence Index readings for sales, profit margins and staffing levels expectations all increased in May, although sales and profit margin expectations remain below the threshold of 50, indicating ongoing anticipation of contraction. The staffing level index remained above that threshold, with more than 38% of contractors expecting to expand their staff during the next six months.

More than 45% of contractors expect their sales to decline during the next six months while 35% expect sales to increase. More than 48% of contractors expect their profit margins to decrease over the next two quarters.

- The CCI for sales expectations increased from 41.1 to 44.9 in May.

- The CCI for profit margin expectations increased from 39.8 to 41.7.

- The CCI for staffing levels increased from 51.4 to 53.

“Given the depth of the economic downturn and myriad other issues facing America today, backlog and contractor confidence data have held up better than one might have anticipated,” said ABC Chief Economist Anirban Basu. “But the marketplace is still tilted toward pessimism. For instance, more contractors expect sales and profit margins to decline than increase over the next six months, which is consistent with anecdotal information suggesting that many project owners are considering postponing projects and possibly rebidding them.

“After falling meaningfully in April, backlog remained relatively unchanged in May, hinting at a stable nonresidential construction marketplace,” said Basu. “However, the underlying survey received fewer responses compared to earlier months in the COVID-19 crisis, perhaps suggesting that some contractors are no longer operating at previous capacity, inducing available work to move toward better-positioned contractors. To the extent that these stronger contractors are reflected in the survey, this would tend to bolster average backlog even in the context of a subdued marketplace.

“Contractors still expect to boost staffing levels over the next six months,” said Basu. “But this may simply be a function of jobsites reopening as construction shutdowns end. Almost 70% of respondents had jobsites shut down due to government mandates and other reasons, and with labor shortages in place before the pandemic, contractors may have residual staffing needs. It remains to be seen whether expected employment growth going forward coincides with speedy recovery in overall contractor confidence and backlog.”

Note: The reference months for the Construction Backlog Indicator and Construction Confidence Index data series were revised on May 12 to better reflect the survey period. CBI quantifies the previous month’s work under contract based on the latest financials available, while CCI measures contractors’ outlook for the next six months.

Related Stories

Contractors | Feb 14, 2023

The average U.S. contractor has nine months worth of construction work in the pipeline

Associated Builders and Contractors reports today that its Construction Backlog Indicator declined 0.2 months to 9.0 in January, according to an ABC member survey conducted Jan. 20 to Feb. 3. The reading is 1.0 month higher than in January 2022.

Office Buildings | Feb 9, 2023

Post-Covid Manhattan office market rebound gaining momentum

Office workers in Manhattan continue to return to their workplaces in sufficient numbers for many of their employers to maintain or expand their footprint in the city, according to a survey of more than 140 major Manhattan office employers conducted in January by The Partnership for New York City.

Giants 400 | Feb 9, 2023

New Giants 400 download: Get the complete at-a-glance 2022 Giants 400 rankings in Excel

See how your architecture, engineering, or construction firm stacks up against the nation's AEC Giants. For more than 45 years, the editors of Building Design+Construction have surveyed the largest AEC firms in the U.S./Canada to create the annual Giants 400 report. This year, a record 519 firms participated in the Giants 400 report. The final report includes 137 rankings across 25 building sectors and specialty categories.

Multifamily Housing | Feb 7, 2023

Multifamily housing rents flat in January, developers remain optimistic

Multifamily rents were flat in January 2023 as a strong jobs report indicated that fears of a significant economic recession may be overblown. U.S. asking rents averaged $1,701, unchanged from the prior month, according to the latest Yardi Matrix National Multifamily Report.

Market Data | Feb 6, 2023

Nonresidential construction spending dips 0.5% in December 2022

National nonresidential construction spending decreased by 0.5% in December, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau. On a seasonally adjusted annualized basis, nonresidential spending totaled $943.5 billion for the month.

Architects | Jan 23, 2023

PSMJ report: The fed’s wrecking ball is hitting the private construction sector

Inflation may be starting to show some signs of cooling, but the Fed isn’t backing down anytime soon and the impact is becoming more noticeable in the architecture, engineering, and construction (A/E/C) space. The overall A/E/C outlook continues a downward trend and this is driven largely by the freefall happening in key private-sector markets.

Hotel Facilities | Jan 23, 2023

U.S. hotel construction pipeline up 14% to close out 2022

At the end of 2022’s fourth quarter, the U.S. construction pipeline was up 14% by projects and 12% by rooms year-over-year, according to Lodging Econometrics.

Products and Materials | Jan 18, 2023

Is inflation easing? Construction input prices drop 2.7% in December 2022

Softwood lumber and steel mill products saw the biggest decline among building construction materials, according to the latest U.S. Bureau of Labor Statistics’ Producer Price Index.

Market Data | Jan 10, 2023

Construction backlogs at highest level since Q2 2019, says ABC

Associated Builders and Contractors reports today that its Construction Backlog Indicator remained unchanged at 9.2 months in December 2022, according to an ABC member survey conducted Dec. 20, 2022, to Jan. 5, 2023. The reading is one month higher than in December 2021.

Market Data | Jan 6, 2023

Nonresidential construction spending rises in November 2022

Spending on nonresidential construction work in the U.S. was up 0.9% in November versus the previous month, and 11.8% versus the previous year, according to the U.S. Census Bureau.