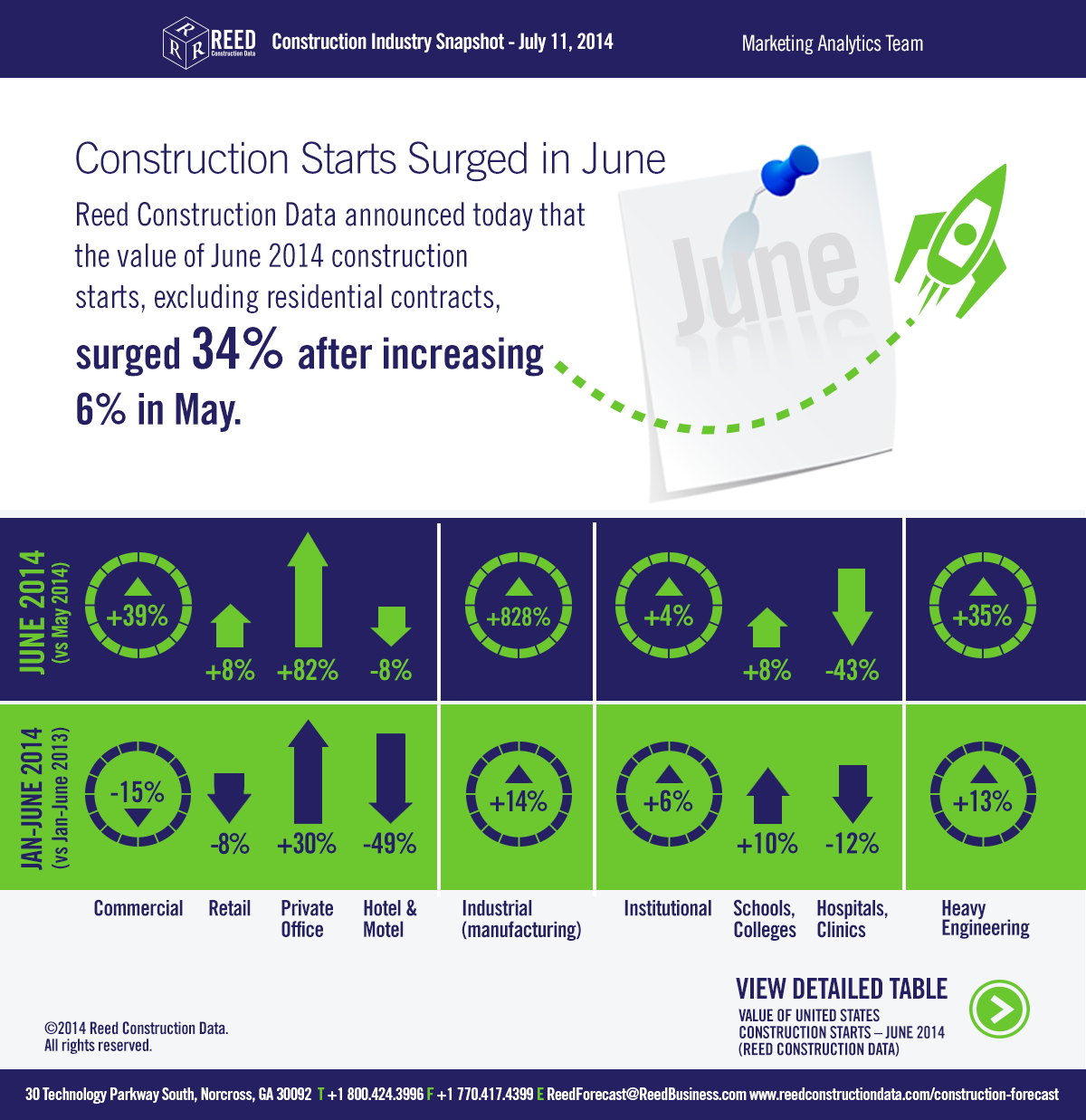

Reed Construction Data has announced that the dollar value of construction starts in June, excluding residential activity, surged 34% versus May. The figures are in "current" dollars, meaning they are not adjusted for inflation.

The individual month of June, at $32.0 billion, was one of the strongest in Reed's entire database. To find a similarly high volume, one has to look back at June 2008, just before the Great Recession really took hold.

The one-third increase was an outsized gain, even after taking into account seasonality. Reed's long-term average May-to-June increase has been 4.5%. By comparison, May's month-to-month percentage change was +6.2% and April's -4.5%.

June starts this year compared with June of last year were +14.4%. The year-to-date level of total nonresidential construction starts, at $138 billion, was +2.4% when compared with the same January to June period of 2013.

Nonresidential construction accounts for a considerably larger share than of the total than residential work. The former's proportion of total put-in-place construction in the Census Bureau's May report was 62% versus the latter's 38%.

Reed's construction starts are leading indicators for the Census Bureau's capital investment or put-in-place series.

After a shockingly harsh winter, during which GDP contracted, the U.S. economy is back on an expansionary path with stock market indices near record highs and the unemployment rate close to the nation's 20-year average of 6.0%. Firms in the private sector are feeling more pressure to build new facilities.

The month-to-month leaders among major nonresidential construction categories were commercial +39%, and heavy engineering +34.7%. Institutional work was also up +3.6%, but to a much lesser degree. Industrial starts recorded a large percentage gain, but it came on top of a smaller dollar volume than the other three.

Commercial starts this June were even more impressive, +48.5%, when compared with June of last year. Engineering starts this June versus the same month last year were +13.7%. Institutional starts were -8.1%.

Year to date, heavy engineering (+13%) is out front, followed by institutional (+5.9%). Commercial starts (-14.5%) are still down from last year. Industrial work is 13.5%.

In commercial construction's two largest sub-categories, retail starts were +8.3% month to month, but -8.1% year to date, while private office building starts were +81.6% month to month and +29.6 year to date.

In the institutional category of work, school and college starts were +7.5% month to month and +9.7% year over year. Hospital/clinic starts moved in the opposite direction, -43.2% month to month and -12.3% year to date.

With the exception of dam/marine work, all the sub-categories of heavy engineering construction were ahead both month to month and year to date, with water and sewage work especially strong versus May, +40.2.

Institutional and heavy engineering work have especially close ties to government finances. Washington's deficit is diminishing, although the debt load remains high. At the state and local levels, the ongoing improvement in the overall economy is providing budgetary payoffs.

The nonresidential construction sector will derive benefits from taxes that are increasing naturally. Stronger employment and higher incomes lift income tax revenues; advances in consumer spending yield more sales taxes; and rising home prices translate into improved property taxes.

The value of construction starts each month is summarized from Reed's database of all active construction projects in the U.S. Missing project values are estimated with the help of RSMeans' building cost models.

See Reed Construction Data's full Construction Industry Snapshot here.

Related Stories

75 Top Building Products | Apr 22, 2024

Enter today! BD+C's 75 Top Building Products for 2024

BD+C editors are now accepting submissions for the annual 75 Top Building Products awards. The winners will be featured in the November/December 2024 issue of Building Design+Construction.

Laboratories | Apr 22, 2024

Why lab designers should aim to ‘speak the language’ of scientists

Learning more about the scientific work being done in the lab gives designers of those spaces an edge, according to Adrian Walters, AIA, LEED AP BD+C, Principal and Director of SMMA's Science & Technology team.

Resiliency | Apr 22, 2024

Controversy erupts in Florida over how homes are being rebuilt after Hurricane Ian

The Federal Emergency Management Agency recently sent a letter to officials in Lee County, Florida alleging that hundreds of homes were rebuilt in violation of the agency’s rules following Hurricane Ian. The letter provoked a sharp backlash as homeowners struggle to rebuild following the devastating 2022 storm that destroyed a large swath of the county.

Mass Timber | Apr 22, 2024

British Columbia changing building code to allow mass timber structures of up to 18 stories

The Canadian Province of British Columbia is updating its building code to expand the use of mass timber in building construction. The code will allow for encapsulated mass-timber construction (EMTC) buildings as tall as 18 stories for residential and office buildings, an increase from the previous 12-story limit.

Standards | Apr 22, 2024

Design guide offers details on rain loads and ponding on roofs

The American Institute of Steel Construction and the Steel Joist Institute recently released a comprehensive roof design guide addressing rain loads and ponding. Design Guide 40, Rain Loads and Ponding provides guidance for designing roof systems to avoid or resist water accumulation and any resulting instability.

Building Materials | Apr 22, 2024

Tacoma, Wash., investigating policy to reuse and recycle building materials

Tacoma, Wash., recently initiated a study to find ways to increase building material reuse through deconstruction and salvage. The city council unanimously voted to direct the city manager to investigate deconstruction options and estimate costs.

Student Housing | Apr 19, 2024

Cal State Long Beach student housing project will add 424 beds

A new $115 million project recently broke ground at California State University, Long Beach (CSULB) that will add housing for 424 students at below-market rates. The 108,000 sf La Playa Residence Hall, funded by the State of California’s Higher Education Student Housing Grant Program, will consist of three five-story structures connected by bridges.

Construction Costs | Apr 18, 2024

New download: BD+C's April 2024 Market Intelligence Report

Building Design+Construction's monthly Market Intelligence Report offers a snapshot of the health of the U.S. building construction industry, including the commercial, multifamily, institutional, and industrial building sectors. This report tracks the latest metrics related to construction spending, demand for design services, contractor backlogs, and material price trends.

MFPRO+ New Projects | Apr 16, 2024

Marvel-designed Gowanus Green will offer 955 affordable rental units in Brooklyn

The community consists of approximately 955 units of 100% affordable housing, 28,000 sf of neighborhood service retail and community space, a site for a new public school, and a new 1.5-acre public park.

Construction Costs | Apr 16, 2024

How the new prevailing wage calculation will impact construction labor costs

Looking ahead to 2024 and beyond, two pivotal changes in federal construction labor dynamics are likely to exacerbate increasing construction labor costs, according to Gordian's Samuel Giffin.