The chief executive officer of the Associated General Contractors of America, Stephen E. Sandherr, issued the following statement in reaction to release today of House Democrats’ Proposed Coronavirus Recovery Measure:

“It is encouraging to see House Democrats moving quickly on legislation intended to help the economy recover from the coronavirus. Their proposal includes measures that will help construction firms that have been hard-hit by declining demand and uncertainty about future market conditions. But the proposal’s authors missed an opportunity to address some of the most significant challenges facing the industry.

“On the positive side, the measure includes some needed relief for state highway programs that have been hammered by declining gas tax revenue amid broad economic lockdown measures. The measure also includes an expansion of the employee retention tax credit that will benefit construction firms that have worked to retain employees. It authorizes composite retirement plans, which hold great potential to address the challenges facing multiemployer retirement plans in which many construction firms participate and provides other needed pension relief. And it includes measures to help construction firms working on federal projects cope with schedule delays and other impacts related to the coronavirus.

“The measure, however, fails to include any safe harbor language to protect firms that are safeguarding workers and the public from the coronavirus from limitless litigation. Meanwhile, the proposed repeal of the net operating loss carryback provision will punish firms, especially family-owned businesses, that suffered losses of $250,000 or more this year. This will make it even harder for these firms to retain staff. And the proposed expansion of the unemployment supplement through January 31 will make it more challenging for firms to rehire employees once demand begins to rebound.

“We appreciate that this measure advances a much-needed debate about the best way to re-start the economy. That is why we will continue to work with members of both parties to craft measures, including liability protections, new infrastructure investments and pension relief, that will help the construction industry recover and rebuild.”

Related Stories

Market Data | Apr 19, 2017

Architecture Billings Index continues to strengthen

Balanced growth results in billings gains in all regions.

Market Data | Apr 13, 2017

2016’s top 10 states for commercial development

Three new states creep into the top 10 while first and second place remain unchanged.

Market Data | Apr 6, 2017

Architecture marketing: 5 tools to measure success

We’ve identified five architecture marketing tools that will help your firm evaluate if it’s on the track to more leads, higher growth, and broader brand visibility.

Market Data | Apr 3, 2017

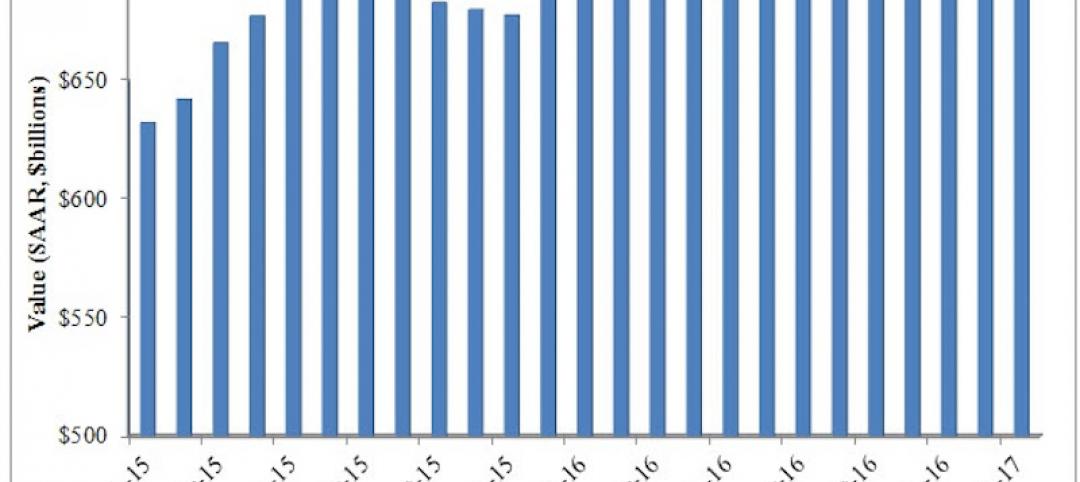

Public nonresidential construction spending rebounds; overall spending unchanged in February

The segment totaled $701.9 billion on a seasonally adjusted annualized rate for the month, marking the seventh consecutive month in which nonresidential spending sat above the $700 billion threshold.

Market Data | Mar 29, 2017

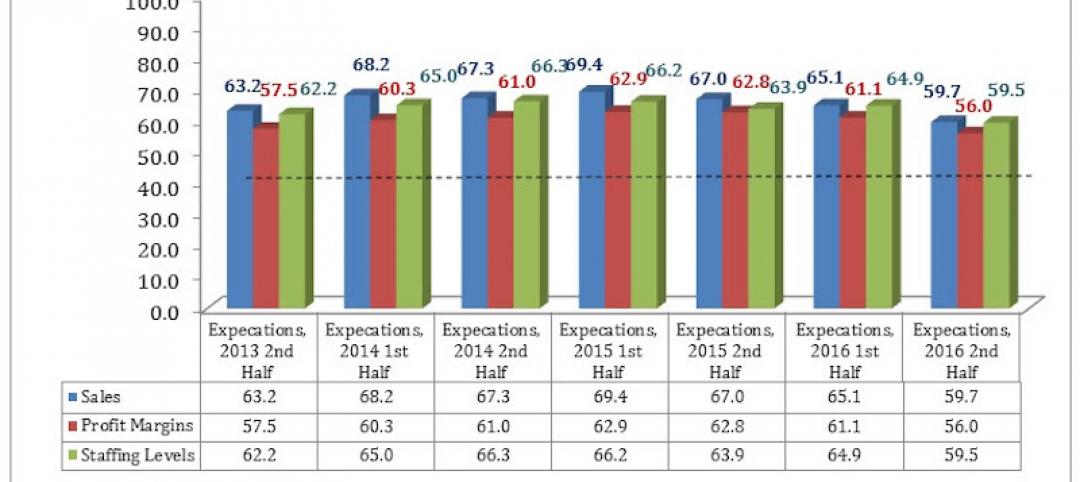

Contractor confidence ends 2016 down but still in positive territory

Although all three diffusion indices in the survey fell by more than five points they remain well above the threshold of 50, which signals that construction activity will continue to be one of the few significant drivers of economic growth.

Market Data | Mar 24, 2017

These are the most and least innovative states for 2017

Connecticut, Virginia, and Maryland are all in the top 10 most innovative states, but none of them were able to claim the number one spot.

Market Data | Mar 22, 2017

After a strong year, construction industry anxious about Washington’s proposed policy shifts

Impacts on labor and materials costs at issue, according to latest JLL report.

Market Data | Mar 22, 2017

Architecture Billings Index rebounds into positive territory

Business conditions projected to solidify moving into the spring and summer.

Market Data | Mar 15, 2017

ABC's Construction Backlog Indicator fell to end 2016

Contractors in each segment surveyed all saw lower backlog during the fourth quarter, with firms in the heavy industrial segment experiencing the largest drop.

Market Data | Feb 28, 2017

Leopardo’s 2017 Construction Economics Report shows year-over-year construction spending increase of 4.2%

The pace of growth was slower than in 2015, however.