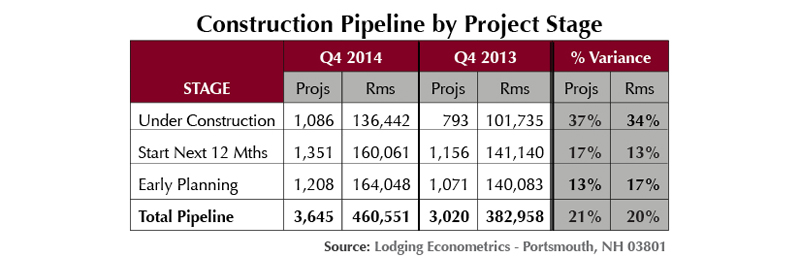

Lodging Econometrics reports that with 3,645 projects (totaling 460,551 rooms), the 2014 total U.S. lodging construction pipeline stands at its highest level in six years.

After a three-year bottoming formation, the pipeline has now posted five consecutive quarters of double-digit year-over-year (YOY) growth. In both the third and fourth quarters, increases were particularly impressive, exceeding 20%.

Although the breakout might appear robust, pipeline totals are still a long way from the peak of 5,438 projects/718,387 rooms set in 2007.

Projects under construction, the most important predictor of near-term supply growth, has catapulted forward to 1,086 projects/136,442 rooms—the highest level in more than five years. The number of units under construction is up 37% by projects and 34% by rooms (YOY).

Projects scheduled to start construction in the next 12 months have risen strongly, to 1,351 projects/160,061 rooms, up 17% and 13% YOY, respectively.

The growing number of projects in early planning is only just beginning. The cyclical bottom for projects in early planning just occurred in the second quarter of 2014. It bounced back smartly in the second half of the year, adding 221 projects, and ended 2014 at 1,208 projects/164,048 rooms.

Projects in early planning directly influence the number of hotels that will open three to five years outward. Projects that enter the pipeline in early planning are generally larger hotels in downtown or resort locations. Most are upscale select-service projects, while others are upper upscale and luxury full-service hotels that are frequently part of mixed-use developments.

Planning and permitting these larger, more complex projects is typically more protracted and also comes with longer construction periods. These projects generally open near the end of a real estate cycle, often times after the cycle has already peaked and begun to decline.

Project counts in early planning are expected to spurt forward over the next two to three years and make significant additions to new supply towards the end of the decade.

Related Stories

Hotel Facilities | Apr 24, 2024

The U.S. hotel construction market sees record highs in the first quarter of 2024

As seen in the Q1 2024 U.S. Hotel Construction Pipeline Trend Report from Lodging Econometrics (LE), at the end of the first quarter, there are 6,065 projects with 702,990 rooms in the pipeline. This new all-time high represents a 9% year-over-year (YOY) increase in projects and a 7% YOY increase in rooms compared to last year.

Hotel Facilities | Apr 17, 2024

Will the surge in hotel construction carry resorts with it?

The resort corner of the hospitality sector has been a bit slower to expand than the whole for the past few years. But don’t tell that to Bill Wilhelm, President of R.D. Olson Construction.

Hotel Facilities | Jan 22, 2024

U.S. hotel construction is booming, with a record-high 5,964 projects in the pipeline

The hotel construction pipeline hit record project counts at Q4, with the addition of 260 projects and 21,287 rooms over last quarter, according to Lodging Econometrics.

Giants 400 | Jan 2, 2024

Top 80 Hotel Construction Firms for 2023

Suffolk Construction, STO Building Group, PCL Construction Enterprises, AECOM, and Brasfield & Gorrie top BD+C's ranking of the nation's largest hotel and resort general contractors and construction management (CM) firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Jan 2, 2024

Top 70 Hotel Engineering Firms for 2023

Jacobs, EXP, IMEG, Tetra Tech, and Langan top BD+C's ranking of the nation's largest hotel and resort engineering and engineering/architecture (EA) firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Jan 2, 2024

Top 120 Hotel Architecture Firms for 2023

Gensler, WATG, HKS, DLR Group, and HBG Design top BD+C's ranking of the nation's largest hotel and resort architecture and architecture/engineering (AE) firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report.

Engineers | Nov 27, 2023

Kimley-Horn eliminates the guesswork of electric vehicle charger site selection

Private businesses and governments can now choose their new electric vehicle (EV) charger locations with data-driven precision. Kimley-Horn, the national engineering, planning, and design consulting firm, today launched TREDLite EV, a cloud-based tool that helps organizations develop and optimize their EV charger deployment strategies based on the organization’s unique priorities.

Giants 400 | Sep 20, 2023

Top 80 Hospitality Facility Construction Firms for 2023

Suffolk Construction, The Yates Companies, STO Building Group, and PCL Construction Enterprises top BD+C's ranking of the nation's largest hospitality facilities sector contractors and construction management (CM) firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report. Note: This ranking includes revenue for all hospitality facilities work, including casinos, hotels, and resorts.

Giants 400 | Sep 20, 2023

Top 75 Hospitality Facility Engineering Firms for 2023

Jacobs, IMEG, EXP, and Tetra Tech top BD+C's ranking of the nation's largest hospitality facilities sector engineering and engineering/architecture (EA) firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report. Note: This ranking includes revenue for all hospitality facilities work, including casinos, hotels, and resorts.

Giants 400 | Sep 20, 2023

Top 130 Hospitality Facility Architecture Firms for 2023

Gensler, WATG, HKS, and JCJ Architecture top BD+C's ranking of the nation's largest hospitality facilities sector architecture and architecture/engineering (AE) firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report. Note: This ranking includes revenue for all hospitality facilities work, including casinos, hotels, and resorts.