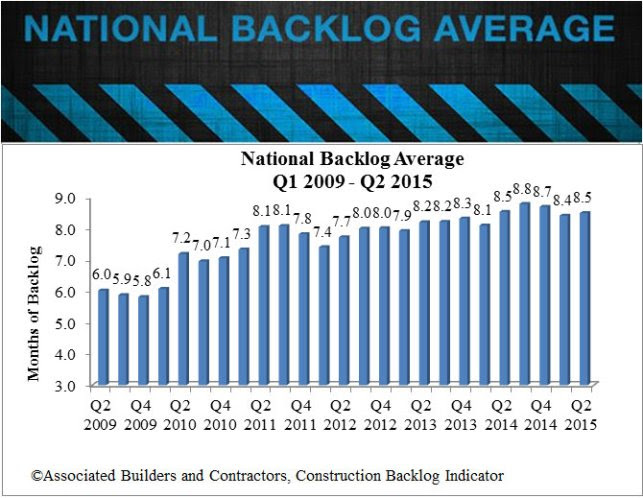

Associated Builders and Contractors' (ABC) Construction Backlog Indicator (CBI) expanded by 1% to 8.5 months during the 2nd quarter of 2015. Backlog declined 3% during the 1st quarter, which was punctuated by harsh winter weather and the lingering effects of the West Coast ports slowdown. CBI stands roughly where it did a year ago, indicative of an ongoing recovery in the nation's nonresidential construction industry.

"The nation's nonresidential construction industry is now one of America's leading engines of growth," said ABC Chief Economist Anirban Basu. "The broader U.S. economic recovery is now in its 74th month, but remains under-diversified, led primarily by a combination of consumer spending growth as well as residential and nonresidential construction recovery. Were the overall economy in better shape, the performance of nonresidential construction would not be as closely watched. The economic recovery remains fragile despite a solid GDP growth figure for the second quarter, and must at some point negotiate an interest-rate tightening cycle. Recent stock market volatility has served to remind all stakeholders how delicate the economic recovery continues to be."

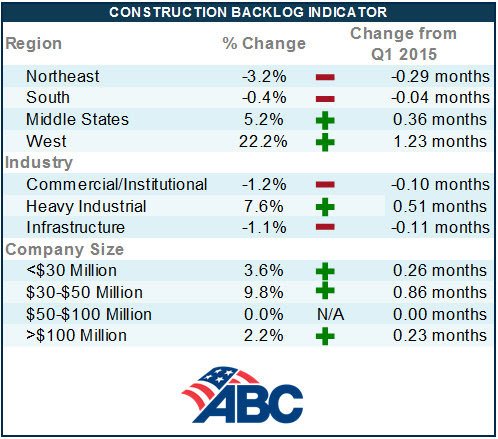

Regional Highlights

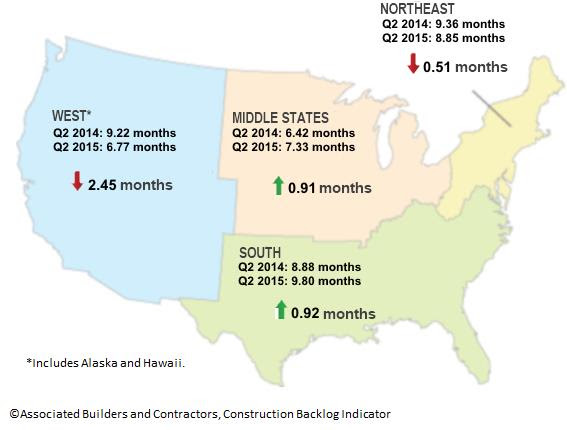

- The West experienced a significant expansion in backlog, rising 1.2 months following the resolution of the West Coast port slowdown, however backlog in the region remains nearly 2.5 months below its year-ago levels, the largest drop of any region.

- Backlog in the South has essentially returned to where it was two years ago, in part because of a slowdown in energy-related investment. The implication is that the average contractor remains busy, but boom-like conditions no longer prevail in energy-intensive communities.

- Despite this, backlog in the South continue to hold the longest average construction backlog.

- Backlog slipped for a second consecutive quarter in the Northeast, but remains above levels registered during the second half of 2013.

- See charts and graphs here.

Industry Highlights

- Backlog in the heavy industrial segment has never been higher during the length of the series, penetrating the seven-month mark for the first time. This represents an increase of more than two months in average backlog over the past two years. Average backlog was below five months during 2013's second half.

- Industrial backlog has continued to rise despite the strength of the U.S. dollar, which has contributed to limited export growth.

- Commercial/institutional backlog has remained above eight months on average for twelve consecutive quarters, a reflection of America's steady rate of employment expansion.

- Backlog for all industry segments is higher on a year-over-year basis with exception of the commercial/institutional segment. Commercial/institution construction segments have been among the most active from a construction spending perspective in recent years. Therefore, the small adjustment in average backlog is not particularly worrisome.

- See charts and graphs here.

Highlights by Company Size

- On a quarterly basis, backlog rose or remained flat across all firm sizes.

- Average construction backlog is higher or roughly the same as year-ago levels for firms of all size categories with the exception of a half-month drop in backlog among firms generating $100 million or more in annual revenues.

- The largest firms, however, continue to have the lengthiest average backlog at 10.7 months.

- See charts and graphs here.

Related Stories

Senior Living Design | Apr 24, 2024

Nation's largest Passive House senior living facility completed in Portland, Ore.

Construction of Parkview, a high-rise expansion of a Continuing Care Retirement Community (CCRC) in Portland, Ore., completed recently. The senior living facility is touted as the largest Passive House structure on the West Coast, and the largest Passive House senior living building in the country.

Hotel Facilities | Apr 24, 2024

The U.S. hotel construction market sees record highs in the first quarter of 2024

As seen in the Q1 2024 U.S. Hotel Construction Pipeline Trend Report from Lodging Econometrics (LE), at the end of the first quarter, there are 6,065 projects with 702,990 rooms in the pipeline. This new all-time high represents a 9% year-over-year (YOY) increase in projects and a 7% YOY increase in rooms compared to last year.

75 Top Building Products | Apr 22, 2024

Enter today! BD+C's 75 Top Building Products for 2024

BD+C editors are now accepting submissions for the annual 75 Top Building Products awards. The winners will be featured in the November/December 2024 issue of Building Design+Construction.

Resiliency | Apr 22, 2024

Controversy erupts in Florida over how homes are being rebuilt after Hurricane Ian

The Federal Emergency Management Agency recently sent a letter to officials in Lee County, Florida alleging that hundreds of homes were rebuilt in violation of the agency’s rules following Hurricane Ian. The letter provoked a sharp backlash as homeowners struggle to rebuild following the devastating 2022 storm that destroyed a large swath of the county.

Mass Timber | Apr 22, 2024

British Columbia changing building code to allow mass timber structures of up to 18 stories

The Canadian Province of British Columbia is updating its building code to expand the use of mass timber in building construction. The code will allow for encapsulated mass-timber construction (EMTC) buildings as tall as 18 stories for residential and office buildings, an increase from the previous 12-story limit.

Standards | Apr 22, 2024

Design guide offers details on rain loads and ponding on roofs

The American Institute of Steel Construction and the Steel Joist Institute recently released a comprehensive roof design guide addressing rain loads and ponding. Design Guide 40, Rain Loads and Ponding provides guidance for designing roof systems to avoid or resist water accumulation and any resulting instability.

Building Materials | Apr 22, 2024

Tacoma, Wash., investigating policy to reuse and recycle building materials

Tacoma, Wash., recently initiated a study to find ways to increase building material reuse through deconstruction and salvage. The city council unanimously voted to direct the city manager to investigate deconstruction options and estimate costs.

Student Housing | Apr 19, 2024

Cal State Long Beach student housing project will add 424 beds

A new $115 million project recently broke ground at California State University, Long Beach (CSULB) that will add housing for 424 students at below-market rates. The 108,000 sf La Playa Residence Hall, funded by the State of California’s Higher Education Student Housing Grant Program, will consist of three five-story structures connected by bridges.

Construction Costs | Apr 18, 2024

New download: BD+C's April 2024 Market Intelligence Report

Building Design+Construction's monthly Market Intelligence Report offers a snapshot of the health of the U.S. building construction industry, including the commercial, multifamily, institutional, and industrial building sectors. This report tracks the latest metrics related to construction spending, demand for design services, contractor backlogs, and material price trends.

Construction Costs | Apr 16, 2024

How the new prevailing wage calculation will impact construction labor costs

Looking ahead to 2024 and beyond, two pivotal changes in federal construction labor dynamics are likely to exacerbate increasing construction labor costs, according to Gordian's Samuel Giffin.